Investment Universe, Process, Strategy and Benchmark – How does the Fund Manager invest?

East Capital’s investment philosophy is based on a long-term perspective, fundamental analysis and active stock-picking, combining growth with value. The East Capital (Lux) Eastern European Fund (ISIN: FR0000284689) invests in shares of companies in the whole of Eastern Europe, and seeks investments in a very wide spectrum of countries, sectors and companies without country or sector limits. Two thirds of the portfolio consists of large or medium sized companies.

In order to effectively combine stock ideas with top-down and country allocation considerations, the 19 countries in Eastern Europe we invest in are divided into 8 different regions for which we build separate model portfolios. The Eastern European fund is a selection of the best ideas from each model portfolio, consequently benefiting from a high diversification (as a comparison, the benchmark MSCI EM Europe Index Total Return only comprises 5 countries).

Performance Review 2007

Peter Elam Håkansson and Team: "The year 2007 may well go down in recent history as the year of the ”decoupling,” i.e. the previously unthinkable split of the American economy from the rest of the world. Previously, it was generally considered that the American economy generally determined developments in other countries. In 2007, this view was challenged, partly as a result of the American credit crisis and its side-effects. Whether or not this split is wishful thinking remains to be seen. In Latin America and the emerging markets of Asia, total exports to the US make up 40% and 20% respectively, whilst the corresponding figure in Eastern Europe is just 4%. Although growth in our region will tail off slightly, it is expected to remain healthy. We feel that countries with strong, balanced economies will do relatively well when the outlook for the world economy is uncertain. Russia is a good example of this, with an economy that is maybe stronger than ever, with good underlying growth as well as large budget and current account surpluses. Poland is a good example of a growth engine in Central Europe, whilst the developments in countries with greater economic imbalances, such as the Baltics, Bulgaria and Romania, are more dependent on changes in the uncertainties of the world market. Growth in Eastern Europe in 2008 will be slower than in 2007, which comes as no surprise bearing in mind that the growth over the last two years has been the strongest since 1989. Furthermore, some of the economies have exceeded their potential, which has led to economic overheating. The most important driver of growth in Eastern Europe has been, and will remain, domestic demand. There are however, considerable variations within the region and the markets are likely to remain volatile."

Performance Review 2008

Peter Elam Håkansson and Team: "The global credit crisis dominated our Eastern European markets for most of 2008 and the last five months of the year in particular. In the first part of the year, Russia outperformed most developed markets, mainly driven by the continuous increase in the oil price. But the appetite for Russian equities was reduced due to the falling oil price in July, political factors like the conflict in Georgia in early August, and a number of company specific situations. As the global credit crunch intensified in September, the Russian market took a big hit and forced selling by highly leveraged local investors exacerbated the downfall. Large injections of capital by the Russian central bank into the system did not succeed in stopping the dramatic fall. For Eastern European markets in general, the sell-off triggered by the increasing risk aversion by international investors have led to liquidity problems and sharply decreasing valuations. Several of these countries also have economic imbalances and the way these will be handled is very important going forward."

Performance Review 2009

Peter Elam Håkansson and Team: "2009 started with a lot of uncertainty after one of the most serious financial crises in modern history. The year did however end on a much more positive note. During 2009, most countries in Eastern Europe recorded almost unprecedented economic contractions and, at the same time, we saw very strong recoveries on the equity markets. Eastern Europe has been amongst the strongest-performing markets and some countries have even shown performance figures over or around 100%. Considering these incredible increases in share prices, it is easy to forget that there is still a long way to go until we are back at pre-crisis levels. For example, the Russian market (RTS), which gained an amazing 128% in USD terms during 2009, is still about 40% lower than the pre-crisis levels, and valuations remain attractive. During the year, we saw global investors coming back to emerging markets again, but the inflows to global emerging markets funds of about USD 80bn went mainly to Asia and Latin America. Although the inflows to Russia and Eastern Europe recovered at the end of 2009, they were still limited."

Performance Review 2010

Peter Elam Håkansson and Team: "In 2010, the Fund outperformed the benchmark by 8.2% in USD terms (+24.2% for the Fund against +16% for the MSCI EM Europe Total Return Index). Overall the Fund benefited from strong stock picking in Russia, most notably from exposure to off-benchmark names in the energy sector like Bashneft, Eurasia Drilling and TNK-BP. Performances of the other countries in the region were mixed. Our exposure to the off benchmark Baltic countries gave a positive allocation effect, as these countries started to recover from the crisis. Less liquid frontier markets however were still lagging behind in terms of performance due to limited investor risk appetite (with the notable exception of Georgia) and the Fund’s exposure to off-benchmark countries led to a combined negative attribution of around 2%.

Underweight in the energy sector gave overall a strong positive allocation effect, as well as an overweight in the consumer sector. The materials sector, where we were underweight, was the main performance detractor during the year."

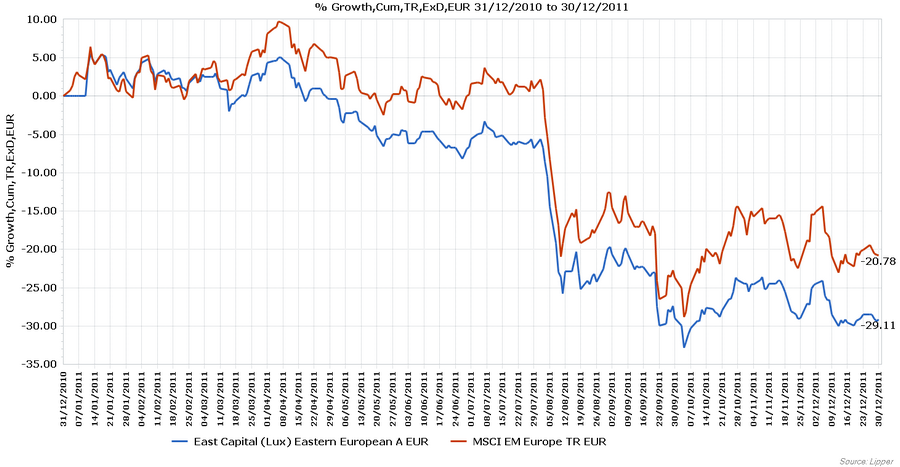

Performance Review 2011

Peter Elam Håkansson and Team: "In 2011, the Fund underperformed the benchmark by 7.3% (-30.8% for the Fund in USD against -23.5% for the MSCI EM Europe Index Total Return). Overall the Fund suffered from its relative overweight to mid-caps and frontier markets in the region, positions we kept and in selected cases even increased during the year as fundamentals for these companies overall did not change in a negative way (rather the opposite).

The benchmark has a significant bias towards the energy sector given the heavy weight of blue-chip names like Gazprom and Lukoil in the MSCI Russia Index and the heavy weight of Russia in the MSCI EM Europe Index (around 65%). As the Russian energy sector was among the most resilient sectors in 2011 in the region and the Fund was underweight this sector, this affected the relative performance negatively.

The financial sector was the biggest performance detractor during the year, on the back of increased global financial worries. Among underperformers in 2011 were the pan-Eastern European banks Erste Bank and Raiffeisen International, which we liked on both valuations and potential higher earnings upside as loan provision write-backs should increase.

Performances of the different countries in the region were mixed. Underweight in benchmark’s weakest country Turkey gave a positive allocation effect but as less liquid frontier markets were punished by decreased risk appetite in 2011, the Fund’s exposure to off-benchmark countries led to a combined negative attribution of around 2%. Still, the Fund’s largest non-index country holding, Fondul Proprietatea in Romania, outperformed the benchmark."

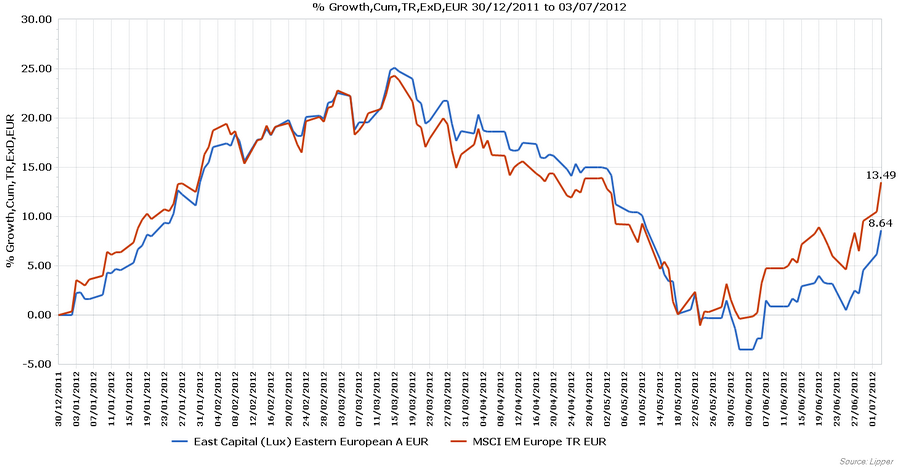

Performance 2012 - Year-to-Date

Peter Elam Håkansson and Team: "As per end of May 2012, the Fund underperformed the benchmark by 1.2% (-5.9% in USD for the Fund against -4.7% for the benchmark). While most equity markets in the region including off-index markets started the year strongly on the back of returning risk appetite, markets took a breather in March and April and then headed South in May, primarily driven by factors outside of the region such as resurfacing of problems in the Eurozone and increased concerns for a slowdown in the US and Chinese economies.

The most dominant attribution effect for the performance year to date was the negative attribution from the Fund’s underweight in best performing index market, Turkey, and the Fund’s overweight in the worst performing sector in the index, Russian utilities. Despite a large current account deficit and an unorthodox monetary policy, Turkey has, somewhat to our surprise, outperformed so far this year in the region. In the utilities sector in the fiscally much stronger Russia, a sector we liked based on the on-going reforms aiming at increased tariffs, the development took a U-turn when rumours surfaced that some of the state-controlled utilities companies could in fact be partly re-nationalized and the reform process could be halted, at least for some time. The Fund’s holdings in MRSK Holding and Federal Grid Company were among the worst performers for the period. As we speak, the development in the Russian utilities sector is difficult to predict short term, but given the sharp sell-off (some names were down around 50% in a month), we see little point in selling these names.

The Fund got positive attribution from several of its beaten down Russian mid-cap names, such as M.Video, LSR, FESCO and Sollers, and we expect this trend to follow as the companies are showing good results and valuations are low. Also, the Fund’s position in Fondul Proprietatea in Romania continued to create positive attribution."

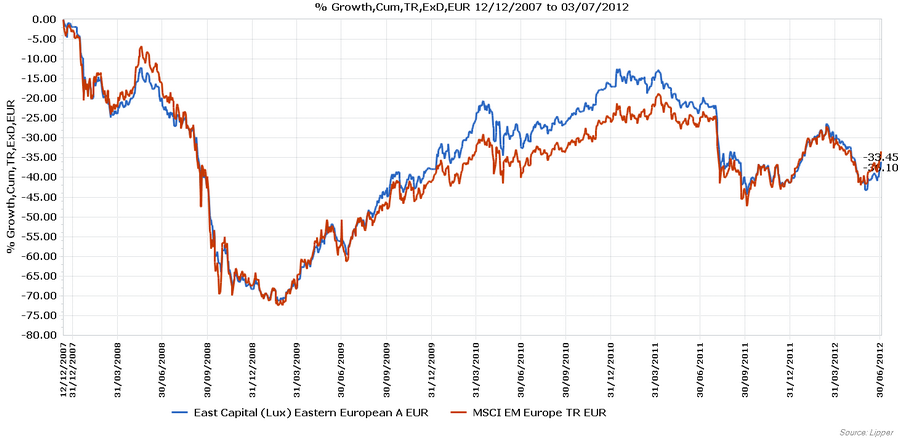

Performance since 2007

Peter Elam Håkansson and Team: "Despite exposure to non-benchmark countries and a larger focus on mid-caps than the index, the Fund outperformed the benchmark with 3.3% (in USD) between 2007-12-12 and 2012-05-31, a very difficult period for active managers encompassing both the Lehman crisis in 2008 and the following European debt crisis."

Weitere beliebte Meldungen:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}