Investment Universe, Process, Strategy and Benchmark – How does the Fund Manager invest? (ISIN: LU0158078906)

Timothy Teo: "Based on initial screening for liquidity with daily turnover >USD 500,000, a universe of about 70 stocks is carved out. Based on preliminary screening based on growth prospects, financial position, industry outlook and management, the list is filtered down to about 50 stocks. Further to that about 40 stocks would be actively researched by meeting management regularly and analyzing the industry which the company operates in.

Despite the recent market weakness, Thailand is one of the best performing markets in Asia. The economy is enjoying a nice rebound from the floods in 4Q11 which saw the country grew only 0.1% last year. Manufacturing activities staged a V-shaped recovery YTD. We expect to see more business activities boosted by the flood management projects starting later this year. The underlying economy remains healthy as seen by strong loans growth and robust capex spending supported by years of under-investment since the early 2000s. Low interest rates are also supportive of leveraged consumption and investment. While export is slower like the rest of the countries in the region, we think that Thailand will continue to register decent growth for the rest of the year given the low base from last year’s flood.

We continue to favour the bank and property sectors in the medium term given the strong health of the economy. With the recent market weakness, we have added some defensives in the telecom and healthcare sectors. However, we are seeing more value emerging in the cyclical sectors, many of these stocks look attractive now. We believe that these stocks should be seeing some valuation support at current levels. Thailand remains one of the cheapest markets in Asia after China and Korea on a PE basis.

Amundi views are subject to change.

The benchmark for the fund is the SET Index which includes all the stocks listed in the Stock Exchange of Thailand (499 stocks, as of 12 June 2012). But many of these stocks are not investible given its low liquidity as mentioned in the above section. "

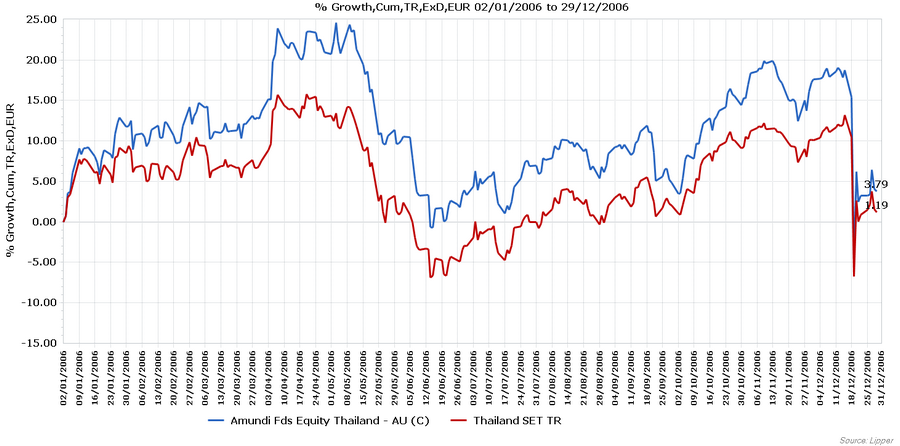

Performance Review 2006

Reginald Tan: "The fund outperformed the benchmark due to our sizable weighting in the financials. Our position in Bank of Ayudhya paid off as the stock outperformed the index by 30% after GE Capital announced its purchase of 25% in the bank in the 3rd quarter of 2006. Interest rate was hiked during the first half of 2006, and the banking and property sector rebounded in the second half of the year in expectation of a rate cut. Our holdings in various property stocks like LPN Development, Preuksa Real Estate and Rojana Industrial Park contributed positively as their sales continue to deliver during the year. Our underweight in the telecommunication sector worked out well as the stocks did not perform that year as reforms continued to be delayed.

On the negative side, the underweight position in the utilities sector resulted in underperformance due to positive expectations on the IPP bidding. Certain consumer stocks which we did not hold outperformed the index like Big C Supercenter and Siam Makro due to improving profit growth."

Performance Review 2007

Reginald Tan: "The fund outperformed the benchmark in 2007. The overweight in energy sector boded well as energy prices almost doubled through the course of 2007. However given the stock limit of maximum 10%, PTT the largest energy conglomerate stock in the index which did well during the year impacted performance in that sector. Our position in Aromatics Thailand (petrochemical) did well as the stock more than doubled in 2007 due to very strong product spreads. Our position in Bank of Ayudhya was noteworthy, which rerated after General Electric (GE) bought 29% of the bank in mid 2006. There were strong expectations of vast improvement in the operations of the bank coupled with acquisitions along the way.

A handful of mid-caps stocks across various sector hurt the fund performance due to the volatile market movement that affected stock prices, this includes Krungthai card, Phatra Securities, Regional Container Lines."

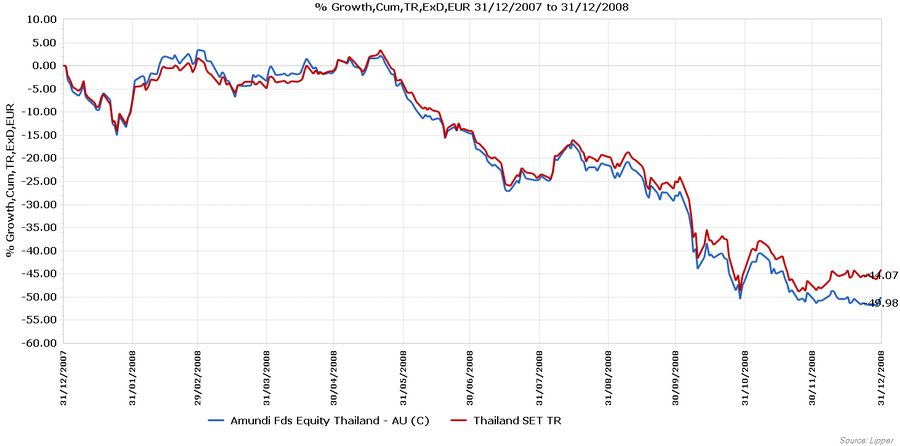

Performance Review 2008

Reginald Tan: "2008 was a very challenging year for the fund. The Lehman Brothers collapse in September 15 2008 triggered a global financial crisis. Politically, Thailand was facing mounting protest from the People Alliance for Democracy (PAD). The fund underperformed the benchmark by 2.89%. A broad based correction in many sectors hit especially hard in the mid-cap stocks segment where liquidity became an issue in a rapid falling market. In terms of sectors we were hurt being overweight property, consumer staples, healthcare and tourist sector. We were helped by our underweight position in Energy, overweight position in banks, telecommunication and utilities as the fund turned defensive around the 3Q-4Q in the year."

Performance Review 2009

Timothy Teo (since May 2009): "The fund outperformed benchmark strongly by 6.10% in 2009. The market rebounded sharply from March. Major changes in the portfolio were made during the market rebound. In general, the fund rotated out of the more defensive stocks like telecommunication, media and utilities into other more cyclical stocks like property stocks, shipping stocks and automaker stocks. Another theme we focussed since early 2009 was the tourism theme which was represented by Airport of Thailand. Then, tourist arrivals were in the midst of bottoming out. We added to an insurance stock, Bangkok Life Assurance on the day of IPO in September and have been adding to its position since then. The stock has been up 90% since IPO. On the negative side, we were hurt by our underweight in Krung Thai Bank that rebounded sharply from very depressed levels and our overweight in CP All that underperformed in a sharp rally in the market. In the early part of the year, we were overweight telecommunication which were also a drag on performance, since 2Q, the position was moved into an underweight."

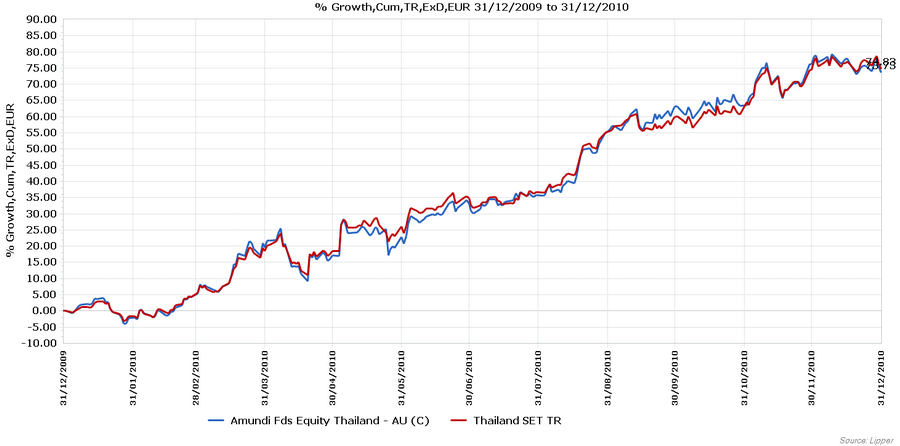

Performance Review 2010

Timothy Teo: "The fund outperformed the benchmark strongly by 8.17% in 2010. Despite seeing one of the worst violence in the last two decades which saw the death of more than 90 people, Thailand turned out to be the best performing market. Our sizable position in the banking sector contributed to the outperformance. Positions like Tisco Financial and Krung Thai Bank were strong winners for the fund. Our overweight in CP All, the 7-11 convenience stores franchiser in Thailand paid off handsomely as the stock more than doubled for the full year. Our stock selection in the energy sector worked well, stocks like PTTEP and Thai Oil were good performers in the sector. On the contrary, our bets in the property sector did not work out well due to the cooling measures to manage supply of condominiums in Bangkok."

Performance Review 2011

Timothy Teo: "In 2011, Amundi Thailand fund outperformed its stated benchmark. Noteworthy contributors were the fund’s holdings in Bangkok Dusit Medical Services which the fund had considerable exposure to. The stock was up 76% in 2011. Another stock that did well was Bangkok Life Assurance that had 50% appreciation in share price. Our overweight in Banks and Properties stocks added strong outperformance to the fund. These sectors registered very strong profits growth all the way till the floods in 3Q11. The healthcare sector outperformed last year following robust earnings growth and valuation accretive acquisition made by Bangkok Dusit Medical. The fund’s exposure in Berli Jucker paid off as the stock was rerated after being discovered by the market that it was a cheap consumer company with Asean focus. Our underweight in the telco sector detracted value against the benchmark, however, it was well offset by the strong stock selection and sector allocation above mentioned."

Performance 2012 - Year-to-Date

Timothy Teo: "YTD the fund was trailing the benchmark. Our early bet on external cyclical did not pay off this year. Exposures in these sectors had been a drag on performance. However we think it is largely been priced into the share prices. The fund was also hurt by stock selection in the financial sector as some stocks underperformed the sector due to various stock specific concerns, some unwarranted while others overdone. Our underweight in telco sector hurt as well. We have since been adding to that sector gradually on weakness in price as the operating environment remains very healthy in our view."

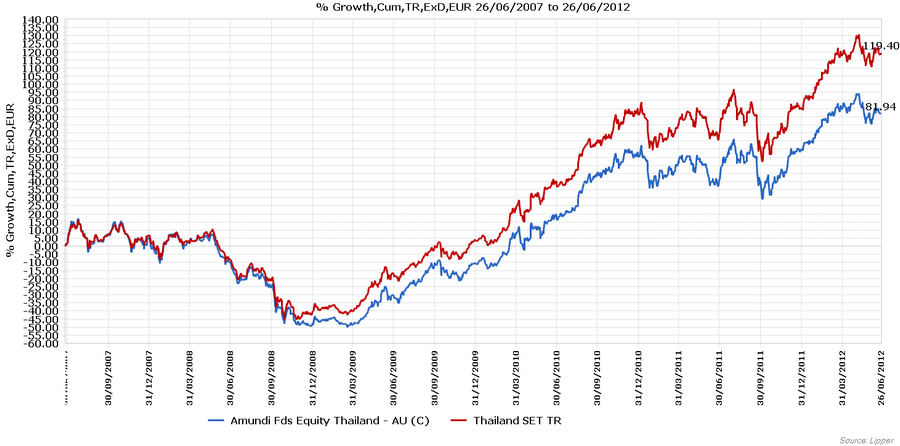

Performance since 2007

Timothy Teo: "The fund outperformed the benchmark based on getting different themes right through the course of the years. On aggregated basis, sectors that did well across the time period were big exposure to banks, properties and energy. The low exposure in telcos benefitted the fund. Our low exposure in the food sector hurt the fund. Political concerns presented the opportunities to buy stocks over the longer term. The performance in 2012 YTD was explained in the previous section."

Weitere beliebte Meldungen:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}