Die Fondsmanager der besten europäischen Schwellenländer Aktienfonds haben exklusiv fünf Fragen zur aktuellen Marktsituation, den Gewichtungen und Performances sowie den Risiken und Chancen beantwortet. Welche Elemente sind die wichtigsten im Investment-Prozess?

Funds

| 25.06.2012 04:30 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

Click on picture to enlarge!

e-fundresearch: "How do you assess the current market situation in the European Emerging Markets?"

Aziz Unan

Aziz Unan, Portfolio Manager, "Renaissance Ottoman EUR" (ISIN: IE00B0T0FN89) (21.06.2012): "Aus unserer Sicht bieten die europäische Schwellenländer hervorragende Anlagemöglichkeiten. Neben Afrika, sind diese Länder auch unser Hauptfokus. Sie haben Russland mit dem Thema Ressourcen, Polen als verlängerte Werkbank Westeuropas sowie die Türkei als dynamisches und wachstumsorientiertes Land mit dem Schwerpunkt Konsum."

Mikael Rosenbeck

Mikael Rosenbeck, Portfolio Manager, "Jyske Invest Turkish Equities" (ISIN: DK0060009835) (20.06.2012): "Despite on-going uncertainties over sovereign debt concerns in peripheral Europe, we expect Turkey to outperform its peers in the near future and will attract EM equity funds thanks to Turkey’s relatively stronger macro position which is highly benefiting from the current weakness in oil price. Furthermore the country has a very attractive demographic structure and a relative low penetration of consumer and mortgage loans which should support growth in the future."

Alexandra Richter

Alexandra Richter, Portfolio Manager, "Allianz Emerging Europe - A - EUR" (ISIN: LU0081500794) (19.06.2012): "We remain distinctly positive for the Eastern and Emerging European region in the medium to longterm. We expect most of the countries in Eastern and Emerging Europe to generate economic growth in the coming years, which is higher than that of Western Europe. The reason for this is that most countries in Eastern and Emerging Europe have less macroeconomic imbalances compared to the countries in Western and Southern Europe. Second, the long-term process of convergence is still far from complete. The GDP per capita is still well below the EU average. The market penetration with various products and services is still low, there remains a sometimes high catch up potential. Investments (outsourcing) into the region continue due to lower labor costs and lower tax burden. However, although the long-term convergence story for Eastern Europe remains intact, the shorter term outlook is affected by fiscal austerity in the Eurozone via direct trade links and capital flows as well as the deleveraging process of European banks.

11.06.2026 10:00

90 Min.

Raheel Altaf (Artemis), Emil Yanchev, Daniel Ganev (Karoll Capital Man...

There are close trade links between countries in Eastern Europe and the European Union. Whereas the trade links with the Eurozone are the highest for Czech Republic and Hungary. Bulgaria, Romania and Poland have a more moderate share. Russia and Turkey have the lowest. The exports to the Periphery are small, with the exception of Bulgaria. Besides the trade linkage, countries in Eastern Europe are also impacted by the financial sector linkage given that around 80% of the banks in Central Europe are owned by European banks which partially funded the growth in the region by external sources. As European banks are currently in the process to deleverage in order to strengthen their capital position, Eastern Europe is also exposed to the deleveraging process. While in many countries foreign ownership is very high, the dependence on external funding is quite different. Therefore markets which are characterized by high loan-to-deposit ratios such as Ukraine, Slovenia, Serbia, Hungary, Romania feel the impact from deleveraging more strongly than markets which are domestically funded such as Czech Republic, Slovakia, Turkey and Russia. Austerity measures and the deleveraging process have also resulted in lower capital inflows to Eastern European. Although the inflow from EU funds should support investments in general, many countries are facing much lower flows than before which hinders the growth of investments and therefore lowers the medium term growth potential of the countries. Due to the openness of their economy Czech Republic and Hungary will both be negatively affected by the weaker activity in the Eurozone. Whereas sound fundamentals including a moderate debt level and commitment to reforms underscore the defensive character of Czech Republic, the economic situation in Hungary is more fragile due to high public and private debt, exposure to FX loans, high external refinancing needs and ongoing deleveraging on the back of high foreign ownership in banking sector. The Polish economy is well diversified, less exposed to exports and its net external position versus foreign banks is relatively benign. Russia is also well positioned to cope with an economic slowdown in Europe - unless the oil price fall below 80$/barrel - as its direct trade exposure is limited, its fundamentals remain strong with the low public and private debt as well as comfortable reserve backdrop. Turkey is facing an economic slowdown which is deserved by the Central Bank in order to bring down the high current account deficit, which makes Turkey vulnerable to sudden stops of capital flows. The longterm the outlook for Turkey remains attractive on the back of its demographic trends, low debt level and low exposure to Europe."

Tom Wilson

Tom Wilson, Co-Portfolio Manager, “Schroder ISF Emerging Europe A Acc” (ISIN: LU0106817157) (20.06.2012): "Global equity markets sold off sharply during the period, driven chiefly by electoral uncertainty in Greece and fears that the country could exit the eurozone. On the political front, the EU summit in May produced no significant policy response to the crisis, while concerns over broader EU policy coordination weighed further on sentiment after Francois Hollande won the French presidential election on a pro-growth platform. In the US, data releases were mixed as April’s non-farm payrolls report was weaker than expected while the Conference Board’s index of leading economic indicators declined. However, there were signs of improvement in US housing markets as sales of new homes rose 10% year on year in April. On the policy front, there was no FOMC meeting in May but the minutes of April’s meeting suggested that the Fed is marginally more confident about the domestic macroeconomic outlook. However, eurozone concerns continued to dominate equity markets during the period, resulting in a sell-off in the MSCI World index. The MSCI Emerging Europe index underperformed the MSCI World and also underperformed the MSCI Emerging Markets index, reflecting relatively poor returns from the higher-beta Russian and Hungarian markets and weakness in a number of the local currencies.

Turkey outperformed its regional peers in May, although it marginally underperformed broader emerging markets. At the stock level, defensive names in areas such as food retail and beverages ranked among the best performers while transport and auto-related names benefited from the decline in Brent crude oil prices. However, the majority of the cyclical and higher-beta names performed poorly as risk appetite declined due to renewed uncertainty in the eurozone periphery. Turkish macro data releases at the start of May were largely encouraging as the HSBC manufacturing PMI accelerated to 52.3 in April from 49.6 in March while industrial production climbed 2.5% year on year in March on a workday-adjusted basis, up from 1.6% the previous month. Current account data also provided some support for sentiment as the deficit eased to $6.1 billion in March – the sixth straight month that the deficit has narrowed. Lagging indicators were resilient as unemployment fell to 10.4% in February 2012, down from 11.5% in the same month of last year. Other consumer-related releases were less upbeat however as consumer confidence eased to 91 in April from 94 in March. On the inflation front, the statistics office reported CPI inflation of 11.1% year on year for April – a three-and-a-half-year high. However, the series has since moderated significantly (to 8.3% year on year in May). On the policy front, the central bank left overnight and benchmark repo rates on hold in May, as expected, while reiterating its determination to meet the 2012 year-end inflation target of 6.5%.

The Czech Republic outperformed its Emerging European peers in May, benefiting from the relatively defensive composition of the local index and the market’s high divided yield. However, macro data releases continued to reflect the negative impact of the ongoing eurozone crisis: the HSBC Manufacturing PMI declined to 49.7 in April and has since eased further to 47.6 in May. Moreover, GDP data showed that the recession unexpectedly deepened as the economy contracted by 1% quarter on quarter in Q1 on a seasonally-adjusted basis; VAT changes are likely to have shifted some consumption into Q4 2011 and poor weather is unlikely to have helped investment, but nonetheless the figures were poor and well below consensus expectations. Industrial production data was also downbeat as the series declined 0.7% year on year in March. Consumer-related data releases continued to reflect a weak consumer environment as retail sales declined 0.3% year on year in March and have since weakened further to -4.1% year on year in April. On the inflation front, CPI rose 3.5% year on year in April, down from 3.8% the previous month and slightly below expectations, but above the central bank’s target. Turning to policy, the central bank held interest rates at 0.75%, in line with expectations. Two of the board members voted for a cut while one voted for an increase.

Poland marginally outperformed its regional peers but underperformed wider emerging markets. At the stock level, defensive names in areas such as telecommunications and utilities outperformed while many of the commodity and financial-related names registered poor returns. On the data front, the HSBC manufacturing PMI declined to 49.2 in April, more than forecast, from 50.1 in March. However, industrial production data continued to highlight the relative resilience of the Polish economy in a CE3 context as the series rose 2.9% year on year in April, slightly ahead of expectations. There were however some signs of the labour market softening slightly, with real wages down 0.6% year on year in April. Inflation data was disappointing as headline CPI rose 4% year on year in April, ahead of expectations. On the policy front, the central bank unexpectedly raised interest rates by 25bps in early May to 4.75% and has since left rates on hold in early June. According to the central bank, May’s hike was made in response to ‘persistently’ high inflation and solid Q1 2012 growth data. The central bank maintained its hawkish stance in early June and does not expect inflation to meet the 2.5% midpoint until early 2014.

Russia underperformed its regional peers and also underperformed its EM peers, reflecting the decline in crude oil prices, the market’s relatively high beta and weakness in the rouble. In contrast to most of the Emerging European markets however, data releases were largely upbeat: inflation eased to 3.6% year on year in April (albeit flattered by the delay in the annual utility tariff hike from 1 January to 1 July), GDP expanded a better-than-expected 4.9% year on year in Q1, and retail sales and real wage growth were robust (up 6.4% and 10.4% year on year respectively in April). Labour markets also remained in good health as the unemployment rate for April was 5.8%, close to a pre-crisis low. On the downside, capital outflows continued, with the central bank data implying a net outflow of $7 billion for April. The net private capital outflow for January-April period was $42 billion, reflecting domestic political unrest and volatility in the rouble. Turning to policy, the central bank decided to keep all monetary policy instruments unchanged (that is, it kept refinancing rate at 8.0%, the overnight deposit at 4.0%, the overnight fixed-rate repo at 6.25% and the overnight auction-based repo rate at 5.25%), as largely expected. However, the accompanying comments were of more interest to many market participants: aside from dismissing weak industrial production and investment readings in March as temporary, the central bank also stated unequivocally that it expects inflation to be within the target range by the end of 2012.

Hungary underperformed the regional index and also underperformed wider emerging markets, reflecting the relatively high beta of the market and weakness in the forint. Data releases continued to highlight the highly open nature of the Hungarian economy, with the manufacturing PMI declining to 46.9 in April from 57.7 in March. However, the PMI has since rebounded to 52.2 in May. Industrial production data has also been volatile, rising 0.6% year on year in March but more recently declining 3.1% year on year in April on a workday-adjusted basis. Inflation data releases during the month were disappointing as headline CPI accelerated to 5.7% year on year in April, ahead of expectations, driven by fuel prices and excise hikes. Business and consumer confidence measures remained downbeat, reflecting ongoing deleveraging. The broader growth environment remained weak, with GDP falling 0.7% year on year in Q1 2012 (-0.1% expected). Turning to policy, the central bank held interest rates at 7%, in line with expectations. In other developments, the government said that it expected to start talks with the IMF ‘soon’; however, at the end May, the ECB said that Hungary’s proposed revisions to the central bank law are insufficient to restore the central bank’s independence (the central bank law is also a key focus for the IMF). At the time of writing, it appears that formal IMF negotiations could start in mid-June, which could allow Hungary to sign a standby agreement in September."

Marcin Fiejka

Marcin Fiejka, Fondsmanager, "Pioneer Funds Em Europe and Med Eq E No Dis EUR" (ISIN: LU0085425469) (20.06.2012): "At the moment Emerging European markets are hostage to the Euro zone crisis and concerns about slowing growth in Europe and elsewhere. The economic situation in places like Russia and Turkey remains good. Turkish economy continues to grow strongly and benefits from falling oil prices. Russian market suffered from falling commodity process and lack of visible reform agenda from the new government. However, trading at PE of less than 5 Russian market is very cheap on historical basis and could show strong recovery on the news of global stimulus programs and expectations of global recovery."

Philip Screve

Philip Screve, Senior Asset Manager, "Dexia Equities B Emerging Europe C Cap" (ISIN: BE0945516574) (15.06.2012): "Emerging markets in general and emerging Europe in particular are still very much in “risk-off” mode. Weaker global growth, lower commodity prices and doubts about the future of the Eurozone have driven down stock prices and currencies, as investors prefer to hide in safe havens such as the US dollar. Emerging Europe has already seen a good part of deleveraging in recent years as Western European banks decrease or limit their exposure to the region. Further Eurozone instability may threaten or delay part of the EU funds targeting infrastructure or agricultural projects. Necessary reform is becoming more difficult to implement as Central European governments fear for loss of popularity with their electorate. The Russian market is less sensitive to the Eurozone problems, but suffers from lower oil prices and fears for rising discontent in the streets. The Turkish market also remains in wait and see mode as the country is dependent on foreign capital inflows to finance its current account deficit."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Which are the most important elements in your investment process?"

Aziz Unan

Aziz Unan, Portfolio Manager, "Renaissance Ottoman EUR" (ISIN: IE00B0T0FN89) (21.06.2012): "Wir sind Value Investoren. Neben einer makroökonomischen Analyse bildet bei uns das Thema Bottom-up Research den Schwerpunkt. So identifizieren wir Unternehmen, die auf mittlerer Sicht ein hohes Wertsteigerungspotential aufweisen."

Mikael Rosenbeck

Mikael Rosenbeck, Portfolio Manager, "Jyske Invest Turkish Equities" (ISIN: DK0060009835) (20.06.2012): "We believe that financial markets are efficient in the long run and that valuation is the key to successful stock-picking. In our mind however, short-term financial markets are not efficient due to human behavior. Academic research shows that the existence of behavioral errors can lead to temporary deviation between market value and fair value. This creates opportunities for the long-term investor.

We implement our philosophy by defining and searching for preferred characteristics – grouped into Valuation, Momentum and Strength. We favour attractively-priced high-quality companies with strong earnings momentum. Our investment process is bottom-up focused and centered around identifying, verifying, validating and analyzing companies with the mentioned characteristics. Macro and sector tilts are not an active part of our investment process.

We are active managers. We believe that combining quantitative screening, fundamental analysis and risk assessment with teamwork and disciplined decision making will lead to generating consistent risk adjusted outperformance in our funds. A combination of fundamental valuation and behavioral finance is hence key to our success."

Alexandra Richter

Alexandra Richter, Portfolio Manager, "Allianz Emerging Europe - A - EUR" (ISIN: LU0081500794) (19.06.2012): "Stock selection is the main part of our investment process and is expected to be the dominant driver of returns for the strategy. However, because country specific trends such as political risk, regulation and macroeconomic environment can also impact stock returns, our process uses both bottom-up and topdown inputs. For stock selection, the direct contact with companies is important. We therefore regularly visit companies in the region. When analyzing a company, the development of its market, the market position and the competitive environment, the financial strength of the company and - very important - the quality of the management are elements of our investment process. We avoid companies with untrustworthiness management, over-stressed balance sheet or questionable business models."

Tom Wilson

Tom Wilson, Co-Portfolio Manager, “Schroder ISF Emerging Europe A Acc” (ISIN: LU0106817157) (20.06.2012): "The fund manager seeks undervalued stocks in countries in Emerging Europe based on a combination of a top-down and bottom-up-approach. About 80% of the value is added is expected to come from stock selection and 20% from country decisions. Our risk controls include alpha adjusted tracking error and stop loss rules with the aim to outperform the MSCI Emerging Europe 10/40 Index by 3.5% per annum. Our portfolio usually holds between 30-50 stocks. Schroders has a large and experience emerging market equity team which is responsible for a range of EM strategies. The Emerging European product is just one of these. There are 38 investment professionals in the team with an average of 12 years’ experience. The fund managers are centralised in London, but the analysts are locally based, although the analysts for the Emerging European product are also London based."

Marcin Fiejka

Marcin Fiejka, Fondsmanager, "Pioneer Funds Em Europe and Med Eq E No Dis EUR" (ISIN: LU0085425469) (20.06.2012): "Regular company visits and talks with our analysts and colleagues in regional offices are key elements."

Philip Screve

Philip Screve, Senior Asset Manager, "Dexia Equities B Emerging Europe C Cap" (ISIN: BE0945516574) (15.06.2012): "The investment process combines a quantitative/qualitative stock screening with a thematic overlay. The quantitative stock selection process gives special attention to a company’s profitability level and evolution as well as dividend levels, both compared to valuation. Attention is also given to more qualitative aspects such as the company’s management and the corporate governance. Selected companies are then matched with a number of longer or shorter term trends or themes driving the markets or the economy."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Which countries and sectors are currently over- and underweighted?"

Aziz Unan

Aziz Unan, Portfolio Manager, "Renaissance Ottoman EUR" (ISIN: IE00B0T0FN89) (21.06.2012): "Neben Emerging Europe liegt unser Hauptfokus momentan auf den Wachstumsmärkten in Afrika. Diese sind aus unserer Sicht im wesentlichen Märkte in Sub-Sahara Afrika, also beispielsweise in Nigeria und Kenia. Nigeria allein hat eine Bevölkerung von 170 Mio. Neben dem Thema Öl, gibt es hier interessante Investitionsmöglichkeiten in den Bereichen Konsum und Infrastruktur."

Mikael Rosenbeck

Mikael Rosenbeck, Portfolio Manager, "Jyske Invest Turkish Equities" (ISIN: DK0060009835) (20.06.2012): "Our aim is to be fairly sector neutral. Instead we are focusing on picking the best companies within each sector using our investment process – looking for companies that are cheap, with positive momentum and with strong earnings.

Overweight: Turkiye Halk Bankasi exposure toward the attractive Retail and SME segment and is the most profitable turkisk bank – with ROE above 20% generated from high NIM and a low cost-income ratio. Furthermore the banks is well capitalized and has a loan to deposit ratio at 82%.

Kozal Altin Isletmeleri is a low cost gold producer with high growth potential. Kozal is currently producing from 2 hubs and plans to increase with 3 more within the next 3 years. Valuation wise the company is attractive."

Alexandra Richter

Alexandra Richter, Portfolio Manager, "Allianz Emerging Europe - A - EUR" (ISIN: LU0081500794) (19.06.2012): "Our active country positions are not very pronounced currently. Following the current market view as outlined above, we tend to underweight certain Central European countries, most notably Hungary. Besides selective exposure to Oil & Gas companies we favor companies exposed to the domestic demand theme such as financials, consumer and telecom stocks. Overall, we prefer more quality companies with sustainable growth, a healthy balance sheet and good dividend yield."

Tom Wilson

Tom Wilson, Co-Portfolio Manager, “Schroder ISF Emerging Europe A Acc” (ISIN: LU0106817157) (20.06.2012): "In terms of country positioning, we remain overweight Russia (although we reduced the magnitude of the overweight in early June) and neutrally positioned in Turkey and Hungary. We are underweight Poland and the Czech Republic. We retain our off-benchmark exposure to Kazakhstan, Egypt and Georgia for stock-specific reasons."

Marcin Fiejka

Marcin Fiejka, Fondsmanager, "Pioneer Funds Em Europe and Med Eq E No Dis EUR" (ISIN: LU0085425469) (20.06.2012): "We are overweight Russia and underweight Hungary and Poland."

Philip Screve

Philip Screve, Senior Asset Manager, "Dexia Equities B Emerging Europe C Cap" (ISIN: BE0945516574) (15.06.2012): "The main country bet in the fund is Russia. The country continues to offer the best and most profitable growth opportunities compared to very low valuation levels. Sector wise the fund’s bets concentrate on consumer related areas (consumer staples, consumer discretionary & IT)."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Where do you see opportunities and where do you see risks and which impact will the European sovereign debt crisis have in the long term?"

Aziz Unan

Aziz Unan, Portfolio Manager, "Renaissance Ottoman EUR" (ISIN: IE00B0T0FN89) (21.06.2012): "Die europäische Staatsschuldenkrise, wie im Übrigen auch das gleiche Thema in den USA, wird uns noch lange beschäftigen. Gerade deshalb bieten die Länder in Osteuropa sowie in Afrika so interessante Investitionsmöglichkeiten. Die Staatsverschuldung in diesen Ländern ist deutlich niedriger."

Mikael Rosenbeck

Mikael Rosenbeck, Portfolio Manager, "Jyske Invest Turkish Equities" (ISIN: DK0060009835) (20.06.2012): "Opportunities for Turkey: Declining oil prices and its positive impact on two main vulnerabilities (i.e. inflation and current account) are the main opportunities from the macro perspective. Investors will enjoy positive real returns for bond yields as inflation will gradually decline through the end of the year. There is also a wide expectation of a possible outlook revision by rating agencies. We believe that current valuations are at tempting levels for Turkish equities. Accordingly, reduced risk appetite due to negative news flow from the Euro Zone and USA, plus elevated equity risk premium brought the ISE’s forward looking P/E to 8.9x levels, implying a 15% discount to its 5-year average. Banks’ current trading level of 1.0x P/BV is not demanding and could be a good opportunity to take positions.

Risks for Turkey: Funding is still the main risk from the macro perspective, especially in case of further squeeze in Eurozone banking system. If one country would exit the European Union or a collapse of a major European country this would most likely have a negative effect on the exchange rate. There are also political risks which are not priced in, like a possible war with Syria.

Long term impact on Turkey: Long term impact of the crisis would be less trade relations with the EU, as a result of ongoing export market diversification. Lower growth would inevitably have adverse effects on the Turkish economy."

Tom Wilson

Tom Wilson, Co-Portfolio Manager, “Schroder ISF Emerging Europe A Acc” (ISIN: LU0106817157) (20.06.2012): "We see significant opportunity in Russia, although we reduced the magnitude of the overweight in early June. Market sentiment remains sensitive to any downward pressure on oil prices and broader global growth concerns; at the time of writing, we estimate that the market is pricing in Brent at $85/bbl. Lower crude prices will dampen economic activity and the economy already faces headwinds from high real interest rates and political uncertainty, which continues to impact the investment environment. On the plus side, leverage is low while the consumer is in good health, boosted by low unemployment, high real wages and fiscal spend over the elections. On a bottom-up basis, the Russian market is very cheaply valued versus both its regional and broader EM peers. However, sentiment towards the gas sector (a dominant share of the benchmark) has deteriorated following the government’s decision to increase extraction taxes. On the political front, reform remains the wild card: the government remains well aware of the need to address concerns regarding corruption, the rule of law and fair representation. Some of the recent rhetoric has been positive in this sense, but implementation is what matters, and the regime has attracted international criticism after significantly raising fines for those taking part in political protests.

In our opinion Eurozone concerns will continue to dominate global equity market returns for the foreseeable future. Measures taken so far appear more focused on treating the symptoms rather than the cause of the problem. The high levels of debt that have been built up across the developed world and the deleveraging that is likely to follow as a consequence is expected to be a multi-year event. Clearly the problems in the Eurozone are particularly acute and countries in the emerging European area are likely to be affected more than most of the other emerging markets. Within the region the CE3 is expected to be the most vulnerable, particularly as the share of their trade with the Eurozone countries is relatively high. However, we are currently either neutral or underweight these counties. As noted earlier, we see better opportunities in markets that are less vulnerable and particularly cheap, such as Russia."

Marcin Fiejka

Marcin Fiejka, Fondsmanager, "Pioneer Funds Em Europe and Med Eq E No Dis EUR" (ISIN: LU0085425469) (20.06.2012): "Most Emerging Europe countries do not have excessive debt levels and are free in their monetary policy. Thus they have the fiscal and monetary means of dealing with economic headwinds and their growth rates are not constrained by debt payments. However, Euro zone is a major trading partner for most Emerging Europe countries and hence they are not isolated from the crisis. In the long run, the crisis might force governments to resolve some of the institutional and structural problems in Euro zone. The crisis will delay Euro zone entry for new EU member countries and create better understanding of how to integrate poorer economies so that they do not go through the boom and bust cycles of southern Europe."

Philip Screve

Philip Screve, Senior Asset Manager, "Dexia Equities B Emerging Europe C Cap" (ISIN: BE0945516574) (15.06.2012): "We continue to see most opportunities in the Russian market, on growth, company profitability and valuation grounds. Obviously risks abound, and investors remain sceptical for now. The Russian budget remains dependent on the oil price. The central bank’s decision to let the rouble depreciate will help lower the budgetary impact, but does not render Russia immune from the oil price evolution or global growth. Capital flight and corruption remain an issue and need to be tackled. In the meantime, areas likely to do best in investment terms are the beneficiaries of the increased consumer and government spending. A boost to valuations may come later in the year as local equity market trading reforms are gradually introduced, making the Russian market more accessible to (foreign) investors, and turning Moscow into a true financial centre. Planned privatisations, new listings and the scope for a substantial increase in participation of (Russian) institutional investors are all indicative of the market´s rerating potential. Consumer and government spending are likely to remain the backbone of Russian growth for some time to come. Russian household consumption will continue to grow as disposable incomes rise and the number of people able to afford more expensive items rises.

The domestic consumer also offers some investment opportunities in Central Europe and Turkey. Risks here are more connected to Eurozone instability/slowdown and its spill over effects: - weaker growth puts pressure on the currency and also makes reforms more difficult in Poland; - weaker growth is also likely to weigh on Czech growth, given the country’s openness; - EU/IMF and Hungarian government remain at odds as foreign demand for government bonds dries up and the HUF remains under pressure; - lower capital inflows risk a faster slowdown and weaker TRY in Turkey as the country continues to run a current account deficit.

The longer term consequences of the European sovereign debt crisis will likely lead to more orthodox budgetary and monetary policies. Germany is set to gradually take up a bigger role in European decision making as the only major player left able to bailout the rest, on its own terms. We see this leadership role as the inevitable corollary for the bailout of the weaker and less competitive Eurozone periphery. The necessary budgetary and deleveraging efforts will likely cap growth for many years to come, especially in those peripheral countries adapting to the ‘new normal’. The re-emergence of Germany as European powerhouse will further shift the economic centre of the EU to the North and the East, with Central Europe benefitting longer term from its geographic proximity and economic integration with Germany."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Did your fund outperform or underperform vs. benchmark over the past 5 years and which part could be linked to securities selection (Performance Attribution)?"

Aziz Unan

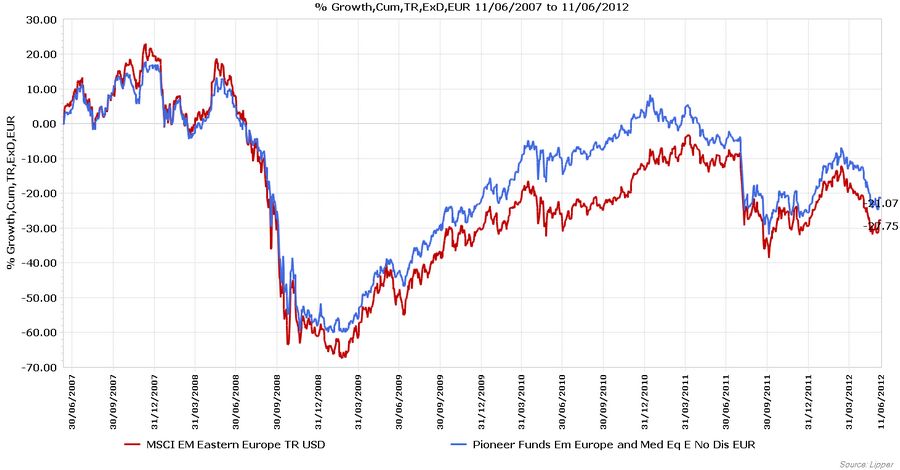

Aziz Unan, Portfolio Manager, "Renaissance Ottoman EUR" (ISIN: IE00B0T0FN89) (21.06.2012): "Unsere Fonds haben generell sehr gut performed. Der Ottoman Fund, ein Türkei-zentrierter Fonds, der ungefähr zu 70% in der Türkei investiert ist, wurde beispielsweise von Feri als bester Osteuropa Fonds im 1. Quartal 2012 dargestellt. EURO hat ihn zu einem der besten Osteuropafonds über einen Zeitraum von 5 Jahren gewählt. Die Titelauswahl spielt dabei eine wesentliche Rolle."

Mikael Rosenbeck

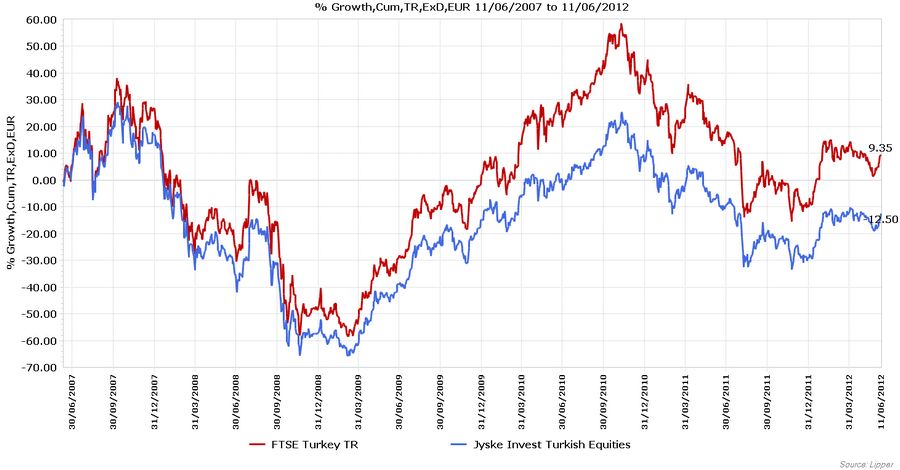

Mikael Rosenbeck, Portfolio Manager, "Jyske Invest Turkish Equities" (ISIN: DK0060009835) (20.06.2012): "We changed benchmark end May 2011 from MSCI Turkey 10/40 to MSCI Turkey 10/40 IMI. The reason behind the change was that MSCI wanted to disclose the MSCI Turkey 10/40 Index due to not enough group entity to enable the calculation. The fund underperformed the MSCI Turkey 10/40 by 9,02% from June 2007 – February 2011. The fund underperformed the MSCI Turkey 10/40 IMI by 0,52% from March2011 – May 2012. The relative risk of the portfolio is low due to a fairly sector neutral approach – which is combined with a beta around 1. Main relative risks is our exposure to companies with cheap valuation and earnings momentum."

Alexandra Richter

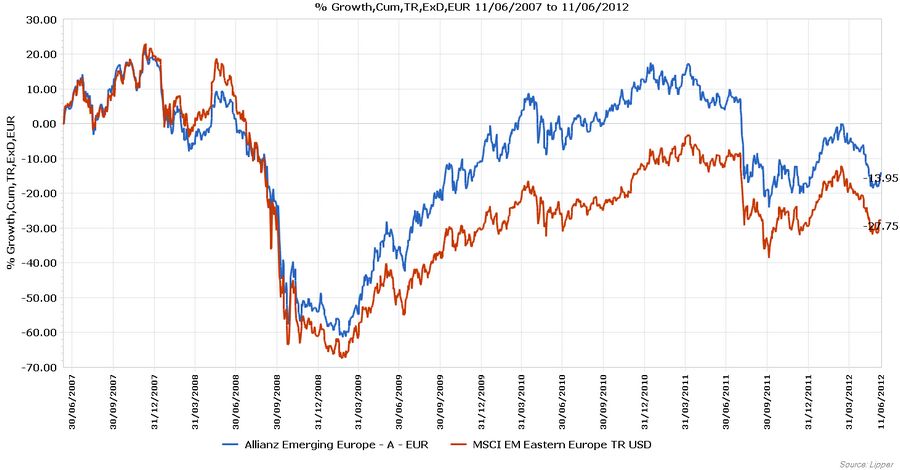

Alexandra Richter, Portfolio Manager, "Allianz Emerging Europe - A - EUR" (ISIN: LU0081500794) (19.06.2012): "The outperformance of the fund is driven by stock selection, which is the main part of our investment process. As in all emerging markets, in Eastern and Emerging Europe active portfolio management offers additional opportunities to add value."

Tom Wilson

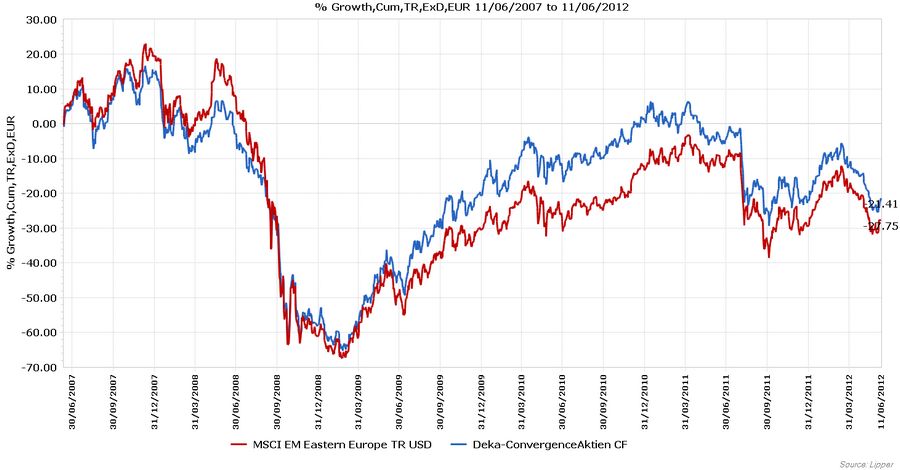

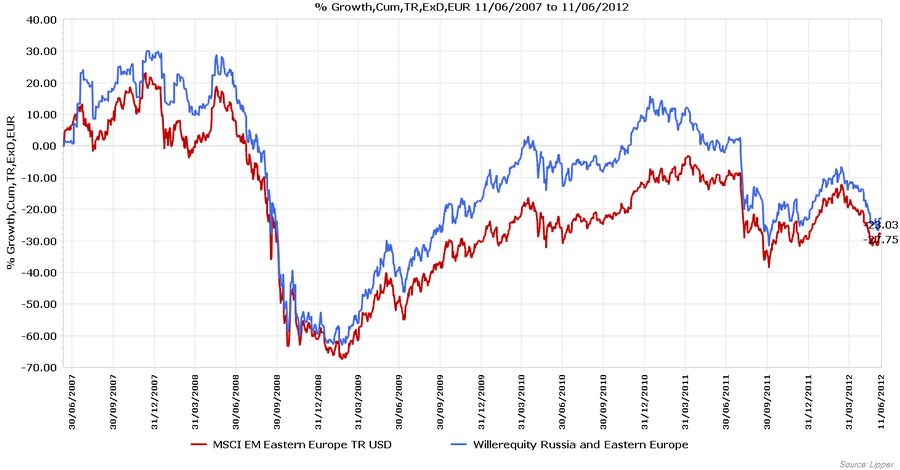

Tom Wilson, Co-Portfolio Manager, “Schroder ISF Emerging Europe A Acc” (ISIN: LU0106817157) (20.06.2012): "The fund outperformed its benchmark over 5 years as at 31 May 2012 returning -17.4% versus -24.5% (MSCI Emerging Markets Europe 10/40 Net (TR))."

Philip Screve

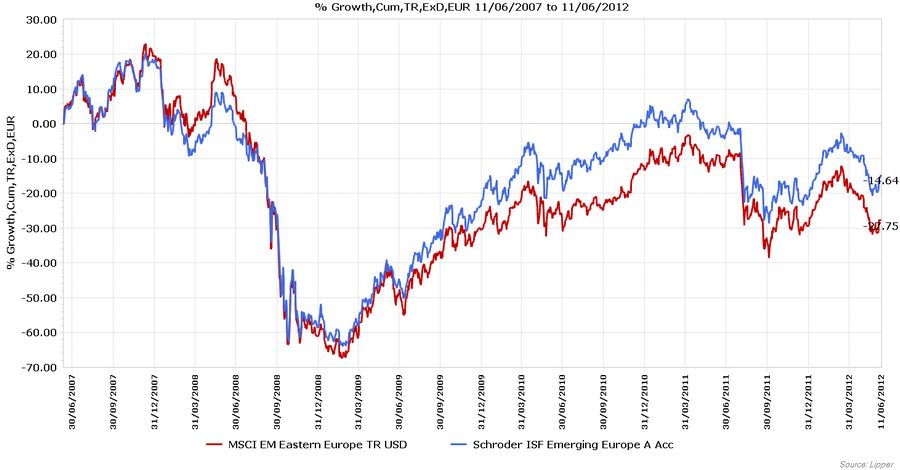

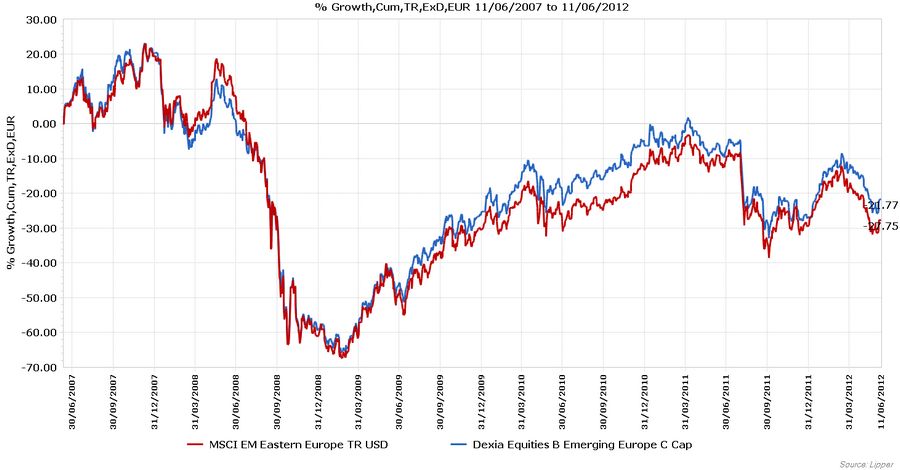

Philip Screve, Senior Asset Manager, "Dexia Equities B Emerging Europe C Cap" (ISIN: BE0945516574) (15.06.2012): "The fund has outperformed the benchmark most of the time over the past 5 years, one exception being the 2008 financial crisis where a lack of liquidity in the markets and extreme volatility led to some temporary underperformance. Stocks selection contributes the biggest part of the fund’s outperformance, with country and sector bets partially a function of the availability or not of attractive investment opportunities at any given time."

Click on picture to enlarge!

Click on picture to enlarge!

Alle Performance Daten der Top-10 Auswertung per 11.06.2012:

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.