Investment Universe, Process, Strategy and Benchmark – How does the Fund Manager invest? (ISIN: LU0256787531)

- Universe: European Small and Mid Caps, excluding the UK

- Objective: Outperformance of the FT Mid Cap Europe ex-UK TR

- Investment approach:

- Fundamental stock-picking, supported by numerous company meeting and strong proprietary screening model

- Firmly believe in companies with strong competitive position (product or market) and consistent growth - Key Portfolio characteristics:

- Long-only portfolio of 60 to 100 stocks

- Strong focus on liquidity: 94% of the fund could be liquidated in less than 5 days

- No position above 3% of the total assets nor more than 5% in the float of any stock

- Outperformance generation derives mostly from stock selection (80%), whilst industry selection and country selection each account for 10%

Investment Process

1/ Research & screening

Two sources of investment ideas:

- Screen the investment universe through quant screening

- Meet as many companies as we can regardless of ranking to remain opportunistic

2/ Analysis & valuation

The investment case has to go through:

- A fundamental analysis: valuation, balance sheet quality, growth, quality of management, competition structure, etc.

- A proprietary price target based on average of PE, EV / EBIT, and DCF

3/ Portfolio construction

Portfolio construction aims at:

- Selecting high conviction stocks

- Focus on liquid names

Risk management

Risk is controlled through 3 lines of defense:

- Instrument selection, sizing constraints

- Stop losses per individual name

- Stop loss at the portfolio level

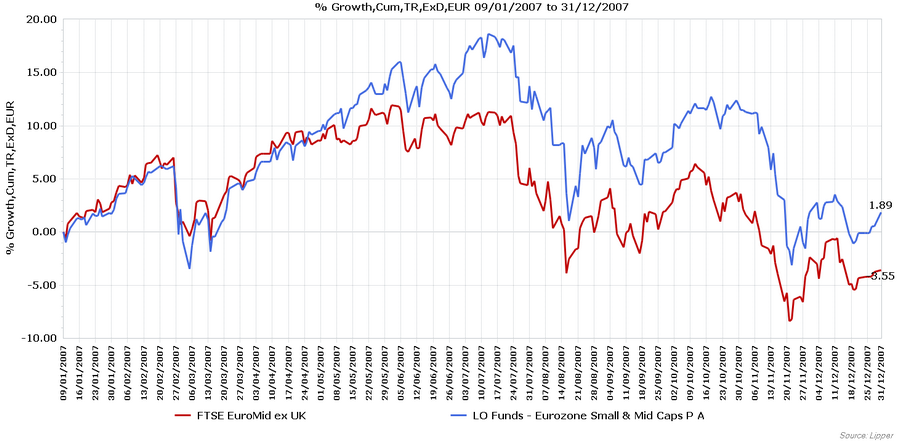

Performance Review 2007

Xavier Lagrandie and Michel Leblanc: "- Outstanding performance (around 9%): fund was positive while benchmark was negative => good sectors selection + stock picking in the fund

- strong positive contribution from overweight in Industrials and IT sectors

- exposure to cyclical stocks which outperformed the defensives ones especially in the first semester

- underperformed in consumer staples and healthcare."

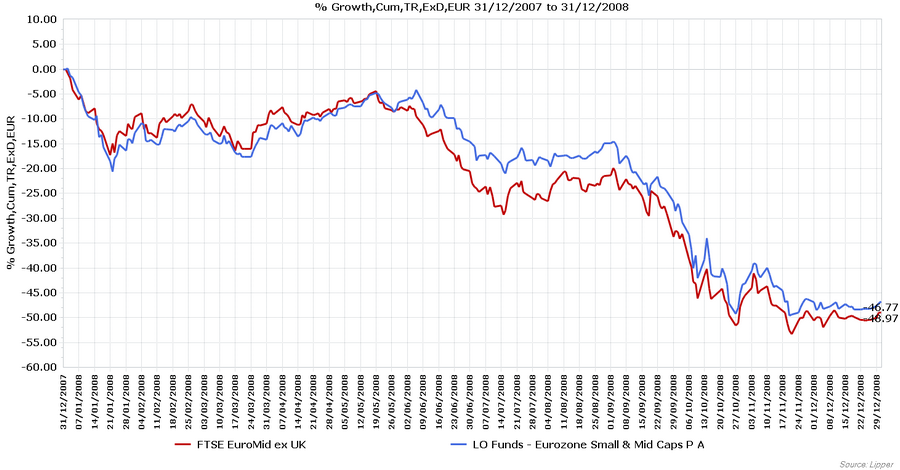

Performance Review 2008

Xavier Lagrandie and Michel Leblanc: "- Good stock picking for IT whereas stock selection for Materials and Consumer discretionary had a negative impact

- Overweight in Industrials vs. underweight in Financials sector paid off, respectively +2% and +1.5%

- France and Germany exposure was well rewarded while Switzerland contribution was significantly negative (currency effect + stock selection) around -2%."

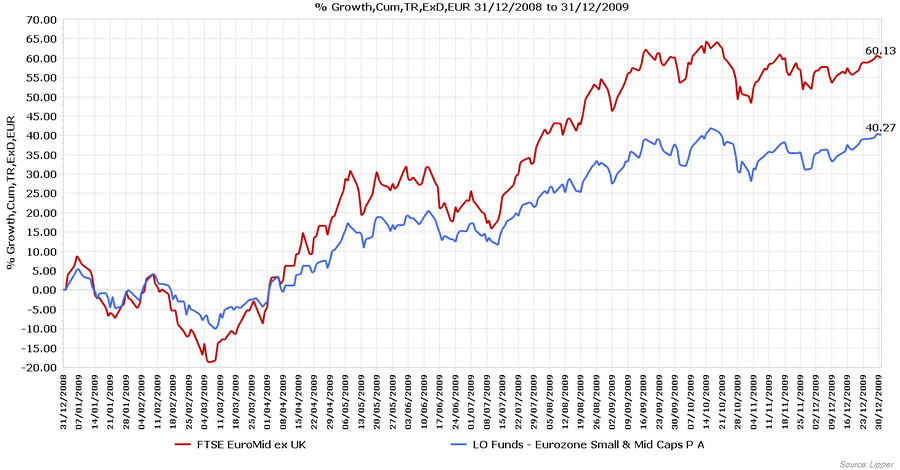

Performance Review 2009

Xavier Lagrandie and Michel Leblanc: "- Overweight in Industrials definitely paid off thanks to good stock picking / Same scenario for Materials and Energy sectors very good stock selection

- Strong negative impact with our overweight in IT combined with poor stock picking compared to the benchmark / same for consumer staples

- underweight in Italy and overweight in Switzerland vs. the benchmark had a positive impact while underweight in Sweden stocks was unfavourable." (ISIN: LU0256787531)

Performance Review 2010

Xavier Lagrandie and Michel Leblanc: "Fund outperformed +33%

- Top 3 sectors : Industrials, Consumer Discretionary and Materials highly outperformed

- Overweight in Industrials paid off

- Outstanding stock picking especially in Financials and Consumer Discretionary + underweight in financials paid off

- Negative currency effect due to underweight in Sweden."

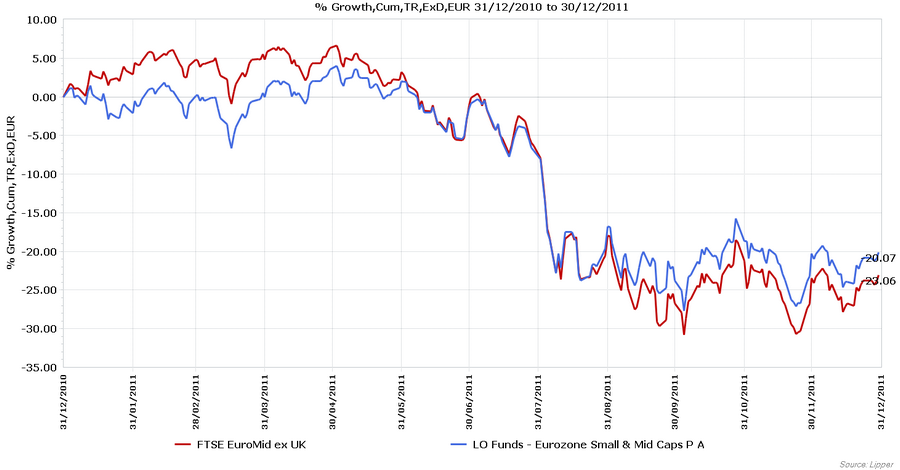

Performance Review 2011

Xavier Lagrandie and Michel Leblanc: "- Good stock selection in Materials sector which underperformed in the overall market

- poor stock picking in Industrials and Consumer staples sectors

- underweight Swedish match position was negative."

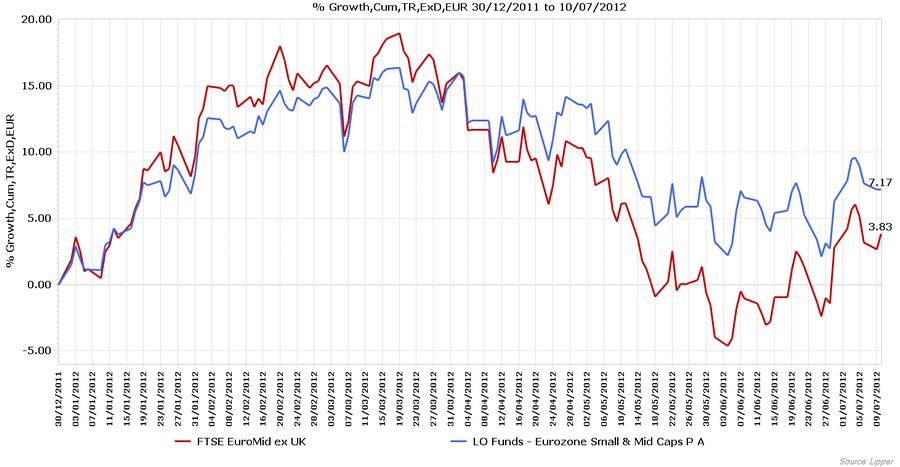

Performance 2012 - Year-to-Date

Xavier Lagrandie and Michel Leblanc: "- Strong underweight in financials + good stock selection pay off

- Good stock picking in industrial sector vs. poor stock selection in consumer staples and discretionary

- Underweight in Spain and overweight in Switzerland => positive contribution to the fund’s performance."

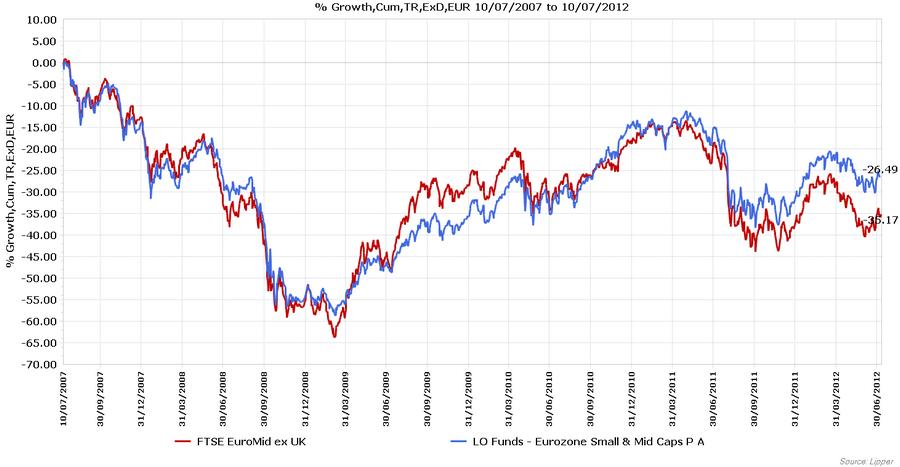

Performance since 2007

Xavier Lagrandie and Michel Leblanc: "Over the period since 2007, the relative performance of the fund is favourable and promising in a very volatile situation knowing that 2008 was a very difficult year for the market.

Neutral positioning vs. benchmark + cash slightly high in average => safe behaviour."

Weitere beliebte Meldungen:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}