Die Fondsmanager der besten Nordamerika Aktienfonds haben exklusiv fünf Fragen zur konjunkturellen Entwicklung in den USA, den Fundamentaldaten, Gewichtungen und Performances der Fonds beantwortet. Was sind potenzielle Risiken für US Aktien?

Funds

| 09.07.2012 15:30 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

Click on picture to enlarge!

e-fundresearch: What is your current outlook for the U.S. economy for the next 12 months?

Cormac Weldon

Cormac Weldon, Head of US Equities & Fund Manager, "Threadneedle (Lux)-American AU (ISIN: LU0061475181)" (04.07.2012): We remain below consensus in our earnings forecasts for the remainder of this year and 2013, based on the uncertainty around the eurozone crisis and the potential impact of the forthcoming presidential election and the ‘fiscal cliff’ on corporate activity.

Nevertheless, we do expect healthy earnings growth of c.5% and we also believe that recent macro data supports our view of a modest and sustainable economic recovery, helped by a greater contribution to economic activity from a levelling out of the housing and consumer sectors. For this reason, we have been favouring domestically-exposed companies, as opposed to companies exposed to global growth.

Against this background, valuations are cheap, even based on our below-consensus earnings forecasts. Valuations are further supported by strong cash flows and balance sheets and by an increased willingness to return capital to shareholders.

With further support coming from attractive valuations and a likely further appreciation in the dollar, we expect the US to be among the best-performing equity markets on a medium-term view.

Grant Bughman

Grant Bughman, Fund Manager, "UBS (Lux) Eq S - USA Growth (USD) P-acc (ISIN: LU0198837287)" (26.06.2012): As we've moved into the summer months the sustainability of the global recovery has been pitted against the demons of excessive debt burden. The US economy and equity markets started the year on a positive note as employment gains in excess of 200,000 jobs per month and the feel good tonic of Europe's Long Term Refinancing Operations fuelled an impressive rally. This optimism has been stymied of late as global economic data has slowed, LTRO's effects wore off, and the intractable relationships between European banks and sovereigns have become more worrisome.

These familiar plot twists have been repeated multiple times since the heights of the financial crisis over three years ago. Ultimately, it appears Europe will need to find some way to bolster economic activity in order help grow its way out of its large debt burdens while receiving support from the ECB and stronger European countries. We expect Europe’s road to get its banking and sovereign problems under control will be lengthy and one fraught with macro risks and vacillating headlines from positive to negative (and back again) along the way. In the US, the continued deleveraging in the private sector and uncertainty surrounding our own fiscal imbalances will continue to be a drag on economic activity. While the US is unlikely to decouple from problems beyond its borders, the relative health of the banking system, ongoing improvement in the housing sector, and the Federal Reserve’s willingness to provide additional stimulus if needed should help the domestic US economy to muddle through the current uncertainty until the end credits of this ongoing saga finally roll.

Jeffrey Bianchi

Jeffrey Bianchi, Fund Manager, "ING (L) Invest US Growth P Cap USD (ISIN: LU0272290692)" (03.07.2012): ING’s Fundamental Equity team does not make macroeconomic forecasts. However we do have a Multi-Asset Strategy and Solutions team (“MASS”) which does make economic forecasts. The following comments are from the economist on ING’s MASS team, NOT the portfolio manager of the fund. We believe that the U.S. economy has moved into a phase of self-sustaining, if modest, growth. We recently lowered our GDP forecasts to 2.2% for 2012 (from 2.5%) and to 3.1% in 2013 (from 3.2%). Central to our forecast is recovery in housing and growth in spending on consumer durables. Our forecast includes the impact of a mild recession in Europe in first half 2012, in line with European Central Bank projections. Inflation is not a risk between now and 2013, as the decline in energy prices and unit labor costs should keep inflationary pressures in check. The FOMC remains committed to maintaining the federal funds rate target near zero until late 2014, and we believe it is likely to undertake a new round of asset purchases should recent employment weakness continue. Serious risks to our forecast remain, notably a larger-than-anticipated “fiscal drag” in the U.S. in early 2013 as tax cuts expire and federal spending cuts take effect. And a financial accident stemming from the ongoing European debt crisis continues to be a possibility.

18.06.2026 10:00

30 Min.

Bernhard Tollay Geschäftsführer, Metis Invest GmbH

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: Which company specific fundamental factors are you focusing on currently?

Cormac Weldon

Cormac Weldon, Head of US Equities & Fund Manager, "Threadneedle (Lux)-American AU (ISIN: LU0061475181)" (04.07.2012): We are focused on companies with exposure to secular growth trends; those operating in industries with high barriers to entry or with a product advantage. These characteristics should help to deliver sustainable earnings growth even in a slow growth environment. We also continue to look for companies with strong balance sheets where management is managing capital proactively, for example buying back shares, raising dividends or undertaking sensible corporate activity. We look for companies that are able to add value for their customers, and where management has the expertise to oversee long-term growth. Naturally, we also determine whether the stocks offer good value and, in particular, whether they have the potential to appreciate in price. There are around 70 stocks held in the portfolio with the top 10 holdings representing about 30% of the fund’s holdings.

Because we are not tied to any one valuation methodology, screen, or factor, we can pick a diverse range of stocks for our portfolios, whether they are growth or value stocks, across the entire market capitalisation spectrum. This flexibility gives us the best chance to perform well in any market environment.

Grant Bughman

Grant Bughman, Fund Manager, "UBS (Lux) Eq S - USA Growth (USD) P-acc (ISIN: LU0198837287)" (26.06.2012): Our investment process is consistent and repeatable and focuses on identifying the best businesses models, then figuring out what to pay for them while diversifying the types of business we own amongst what we call Elite, Classic, and Cyclical growth. When thinking about the types of businesses we own, we look for companies that can take market share, having pricing power and high or improving return on invested capital. We then assess the sustainability of their business model by analyzing the competitive landscape, barriers to entry, or technological advantages which would enable them to continue their growth for a longer period than expected. Once this framework is used to identify the kinds of businesses we’d like to own we assess the valuation which focuses on a probability weighted discounted cash flow scenario analysis to determine base case as well as bull case and bear case price targets.

Jeffrey Bianchi

Jeffrey Bianchi, Fund Manager, "ING (L) Invest US Growth P Cap USD (ISIN: LU0272290692)" (03.07.2012): Our investment philosophy and process has remained unchanged since the inception of the current investment team (May 1, 2004). We integrate fundamental research and screening tools in order to focus our industry and company expertise into superior stock selection, which has been the primary source of excess returns.

The objective of our investment process is to identify stocks that appear attractive based on three principal fundamental drivers we believe characterize successful growth stocks: 1) Business Momentum (strong and improving growth) 2) Valuation (price appreciation potential) 3) Market Recognition (earnings revisions and relative price performance)

Our portfolios consist of stocks with strong fundamental growth characteristics, attractive valuations and potential for upside earnings surprises.

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: Which over- and underweight positions are currently implemented in your U.S. equity positions?

Cormac Weldon

Cormac Weldon, Head of US Equities & Fund Manager, "Threadneedle (Lux)-American AU (ISIN: LU0061475181)" (04.07.2012): Acknowledging the risk-averse market tone and the slowdown in global growth, the fund invests in companies with defensible business models able to grow even in a slow growth environment. In this context, the fund continues to be overweight in Apple. Within financials, we favour credit card companies and have a big position in Capital One. Conversely, the fund continues to be underweight in the utilities and consumer staples sectors, which have recently performed strongly due to risk aversion but which we believe are overvalued. In addition, we have an underweight position in companies exposed to emerging markets as their economic growth slows down.

Grant Bughman

Grant Bughman, Fund Manager, "UBS (Lux) Eq S - USA Growth (USD) P-acc (ISIN: LU0198837287)" (26.06.2012): From a sector standpoint the strategy remains overweight holdings in Consumer Discretionary and Health Care that we believe are well positioned both domestically and globally to take market share. Examples of top holdings include Dollar General, Amazon.com, Priceline.com in Consumer and Allergan, UnitedHealth Group, and Agilent Technologies in Health Care. We continue to seek out sustainable business models that are mispriced by the market, while attempting to the manage the correlation between our three types of growth companies. After the Russell index reconstitution in June the strategy is now slightly overweight the Energy sector as well but remains underweight cyclical companies as a whole, with an underweight remaining in the Financials, Industrials, and Materials sectors. With economic uncertainty remaining elevated, we continue to mitigate the strategy’s risk by reducing its sensitivity to macro-driven influences.

Jeffrey Bianchi

Jeffrey Bianchi, Fund Manager, "ING (L) Invest US Growth P Cap USD (ISIN: LU0272290692)" (03.07.2012): Our portfolio construction process follows a disciplined approach. We believe that controlling sector weights and individual position active weights through prudent position sizing are the critical means by which tracking error risk is managed. At times, the ING Large-Cap Growth strategy may favor a particular industry within a given sector; however, sector exposures typically do not exceed 300 basis points versus the benchmark. We maintain a fairly neutral sector positioning with active exposures broadly dispersed across many industries. Currently the portfolio is very modestly overweight the Information Technology sector and modestly underweight Materials. As always, we are focusing on companies with positive business momentum, appropriate valuations and market recognition that fundamental improvements are sustainable.

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: Where do you see potential risks for US equities?

Cormac Weldon

Cormac Weldon, Head of US Equities & Fund Manager, "Threadneedle (Lux)-American AU (ISIN: LU0061475181)" (04.07.2012): Lately, the ongoing sovereign debt crisis in the eurozone lent a risk-averse tone to markets, reinforced by evidence that economic growth had continued to decelerate in China. In addition, the uncertainty surrounding the political hiatus ahead of the US elections and the ‘fiscal cliff’ mean that companies are less willing to hire and expand until the situation is clearer, which in itself may cause a self-feeding slowdown in the economy in the second half of the year.

Grant Bughman

Grant Bughman, Fund Manager, "UBS (Lux) Eq S - USA Growth (USD) P-acc (ISIN: LU0198837287)" (26.06.2012): As described earlier, the risk to US equities remain the macro environment that both consumer and companies are faced with. The tremendous uncertainty surrounding European sovereigns and banks, political uncertainty and fiscal risks in the US, and slowing emerging markets all pose substantial challenges to US economic growth and as a result equity market valuations.

Jeffrey Bianchi

Jeffrey Bianchi, Fund Manager, "ING (L) Invest US Growth P Cap USD (ISIN: LU0272290692)" (03.07.2012): We believe we are in the midst of a modest global recovery fueled by slowly improving economic conditions in the United States and easing monetary policy globally. In the current slow-growth environment, we remain cautiously optimistic and are focused on what we believe to be high-quality companies with expanding market shares and above-average growth rates.

In our option, the key risk to U.S. equities in the near-term is an exogenous shock to the system. Should a macroeconomic event occur, it could have a contagion effect and impact foreign and domestic markets. Unfortunately, such events are difficult to forecast. A potential short-term negative would be escalation of the nuclear conflict in Iran or North Korea, or a spike in concern about the sovereign debt crisis in Europe. We also continue to monitor China’s economic activity, as it continues to show signs of deceleration (due in part to its European exposure as well as its past contractionary monetary policy).

Within the United States, we generally see modestly improving economic conditions. Monetary policy makers have assured the public that they are willing to provide additional economic stimulus if needed; the Fed’s commitment to accommodative monetary policy encourages individuals and corporations alike back into the risk pool. The housing market has shown signs of life recently, and this could be a key catalyst for the economy should the sector rebound in earnest. Corporate America is generating copious amounts of free cash flow as well as record-high incremental margins, an astonishing level for where we are in the economic cycle. Corporations are starting to give this excess cash back to us in earnest through large buyback programs and dividend increases, a bullish sign about their confidence; increased merger and acquisition activity would be the next step.

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: Please comment on the performance and risk parameters of your fund in the past year as well as over the past 3 and 5 years.

Cormac Weldon

Cormac Weldon, Head of US Equities & Fund Manager, "Threadneedle (Lux)-American AU (ISIN: LU0061475181)" (04.07.2012): The fund outperformed by 2.5% on a gross basis in 2011. The outperformance came primarily from stock selection decisions, while the fund’s sector positioning also added to returns. At the stock level, stock selections within the IT, financials and industrial sectors led to the largest gains, while positions in the healthcare and energy sectors detracted from returns. Highlights included positions in McDonald’s, IBM, Limited Brands, Ralph Lauren and Apple and avoiding Citigroup and Bank of America. Detractors included positions in Themor Fischer Scientific and in a number of oil servicing firms.

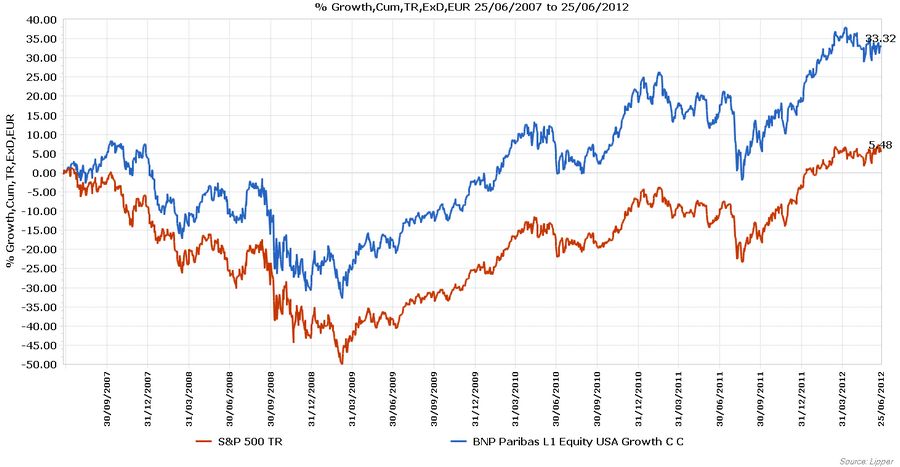

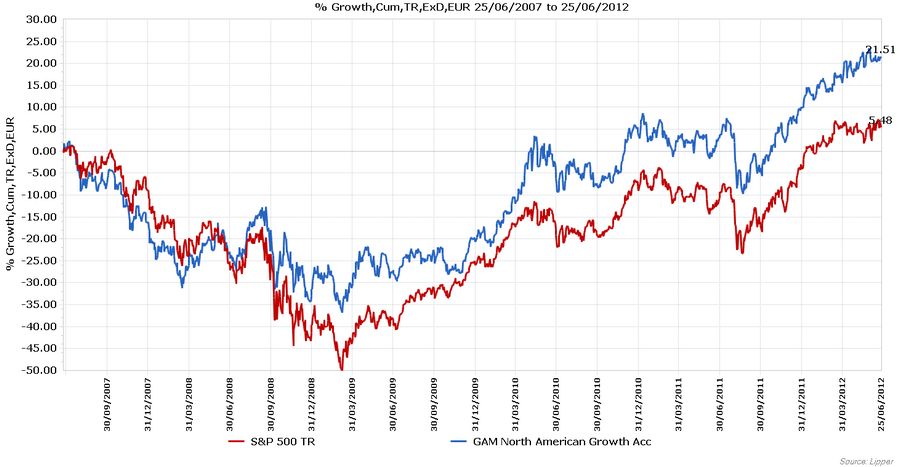

Over the past year, the fund has returned -0.7% net compared to -0.4% (gross) for the index and -3.6% (net) for the peer group, placing the fund in the top quartile of its category. Over the last 3 years, the fund has returned +45.5% net vs. +51.8% for the index (gross) and +39.6% (net) for the peer group. Over 5 years, the fund has returned +17% net vs. -4.5% for the index (gross) and -7.5% for the peer group (net). Data at 31 05 2011.

Risk is a key consideration when we build the portfolio and is a key part of our stock-level analysis as analysts explicitly assess downside risks. when investment opportunities are reviewed, we consider both the upside opportunity and the downside risk. Investment opportunities presenting proportionally good levels of upside with limited downside risk would result in a higher conviction than would be the case for an opportunity where the outcome is more binary. On the back of this, we run high-conviction portfolios which derive most of their risk from the positions that we have selected. Our in-house risk system and the risk report that our risk management team produces daily are used along the way to constantly monitor and review the fund’s positioning.

Grant Bughman

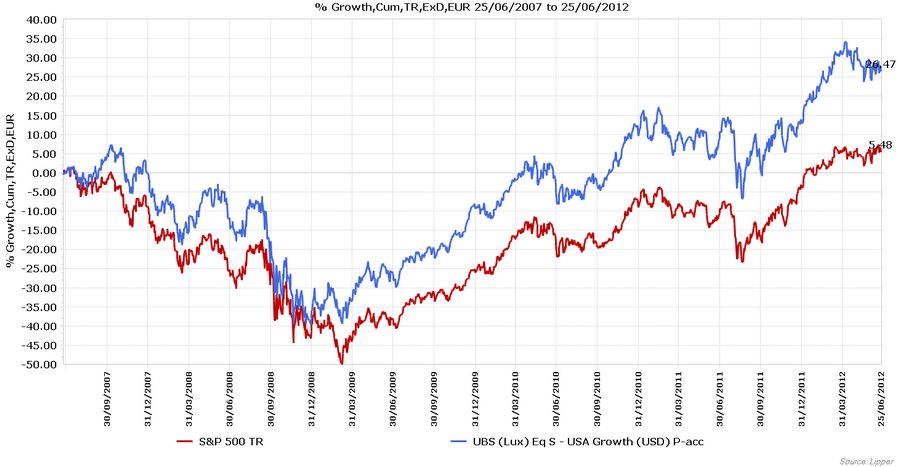

Grant Bughman, Fund Manager, "UBS (Lux) Eq S - USA Growth (USD) P-acc (ISIN: LU0198837287)" (26.06.2012): We seek exposure to a mix of business models in various stages of growth, which enables us to own a diverse range of companies and limit our downside risk. This has helped us outperform during the many recent periods of volatility in markets. The ability to identify disruptive entrants in the Elite growth space (mainly in Information Technology and Consumer Discretionary) has added alpha for our client. We also carefully manage our exposure to risk and focus on building portfolios that carry diversified cash flow streams which has led to a lower than normal allocation to Cyclical growth and solid business models generating strong free cash flows in Classic growth which have helped to dampen returns during the past volatility.

Jeffrey Bianchi

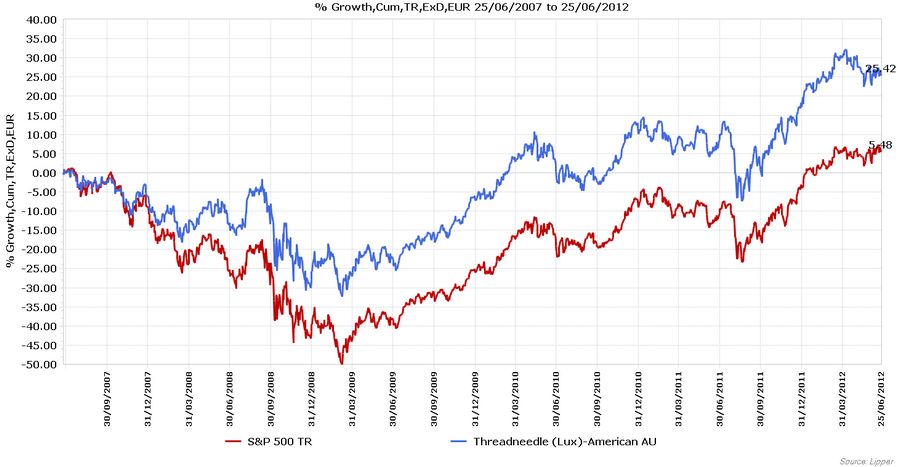

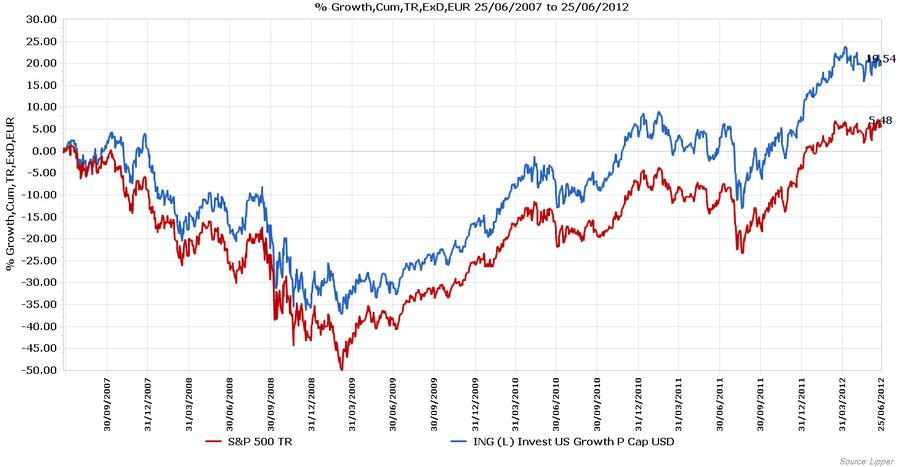

Jeffrey Bianchi, Fund Manager, "ING (L) Invest US Growth P Cap USD (ISIN: LU0272290692)" (03.07.2012): For the one-year period ended March 31, 2012, ING (L) Invest US Growth P-CAP USD (the “Fund”) returned 12.69% versus 11.02% for the benchmark Russell 1000 Growth Index on a gross-of-fees basis. Outperformance was driven primarily by strong stock selection, particularly in the consumer discretionary, consumer staples and industrials sectors. Gains were mitigated primarily by weak selection within information technology and health care.

Over the past three years ended March 31, 2012, the Fund underperformed the Russell 1000 Growth Index by 86 bps; however, the Fund outperformed the benchmark by 217bps over the five-year period. Performance over both periods was attributable to stock selection. Performance in calendar years 2007 and 2008 was exceptionally strong, with the Fund outperforming by 729 bps and 459 bps, respectively. In 2007, eight of the ten GIC sectors added value as a result of positive stock selection. The top contributors to performance were in health care, consumer discretionary and energy. In 2008, seven sectors added value from stock selection. Top contributors to performance were in health care, materials and energy. The key to our success during these volatile market conditions has been a consistent and disciplined approach to stock selection.

Over the past five years our minimal sector bets have resulted in a moderate tracking error (which we view as a key measure of risk). The strategy also had a top-decile information ratio as a result of good excess returns (vs. the Russell 1000 Growth benchmark) combined with a moderate level of risk.

Click on picture to enlarge!

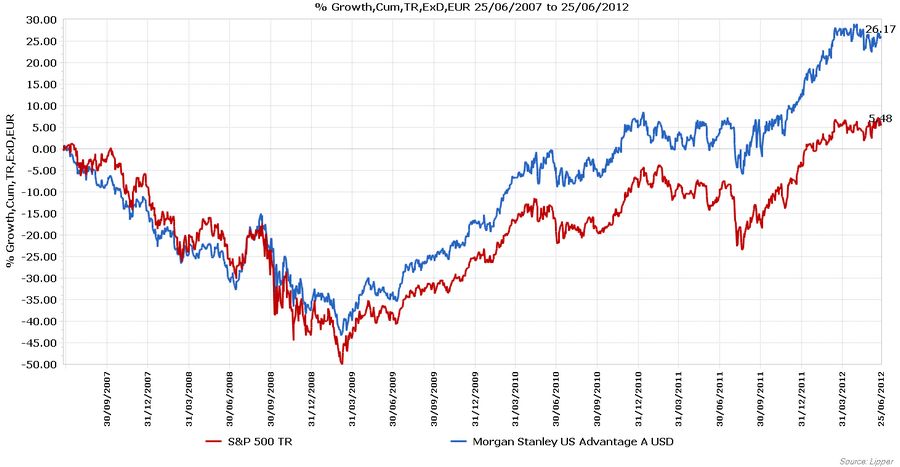

All Performance Data in Top-10 list are per 25.06.2012:

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.