Die Fondsmanager der besten globalen Immobilien Aktienfonds haben exklusiv fünf Fragen zur globalen Konjunktur, den wichtigsten Elementen im Investmentprozess und den Gewichtungen bzw. Performances beantwortet. Was sind die bedeutendsten Risiken bei globalen Immobilienaktien?

Funds

| 16.07.2012 02:00 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

Click on picture to enlarge!

e-fundresearch: "What is your expectation concerning the global economy and its impact on global real estate markets?"

Guy Mountain

Guy Mountain, Real Estate Investment Manager, "Sarasin Sustainable Equity Real Estate Global B" (ISIN: LU0288928376) (10.07.2012): "Our base macro scenario is for an extended period of deleveraging that limits the pace of economic recovery for years to come. Simultaneous deleveraging of the private and public sector in Europe will lead to a sharp recession this year and only a very anemic recovery in the next. Although the US is more advanced in its process of deleveraging, a fiscal contraction looks likely in 2013 – the only question is whether it will be aggressive through political stalemate or modest through bipartisan agreement. On balance, we expect a low quality, low velocity global economic recovery to be the backdrop for the next few years. We expect policy rates to stay low till well into 2015, additional quantitative easing from most central banks and double-dip concerns to continue to prevail.

In this low interest rate environment, the listed real estate sector is well positioned, whether it be from continued quantitative easing pushing up the demand (and therefore prices) for real assets, or purely investors taking comfort in the sector’s secure and visible cash flows and dividends (we have already seen significant outperformance versus global equities this year). The uncertainty also keeps a lid on additional supply, as banks continue to reduce their exposure to real estate in their lending books. However, financing for the listed sector is still healthy, and at attractive levels either through the secured/unsecured debt markets or equity issuance. We also continue to see significant direct market deals by yield hungry institutions needing to match liabilities etc., keeping pricing for prime assets firm."

Marco van Bussel

Marco van Bussel, Portfolio Manager, "First State Global Property Securities A GBP Acc" (ISIN: GB00B1F76L55) (11.07.2012): "The global economy is slowing down rapidly and will take some time to pick up. We are seeing some downside risks in regions such as the Eurozone and China. This all has an impact on the real estate markets such as on the demand side for offices and shopping centres where business outlook confidence is deteriorating. As such you see demand for offices declining across the board but there are some markets which in general will do better like New York and London, although there is also a downward trend in these cities. Likewise in the retail sector sales are not as good as expected as consumer confidence is declining. The upper-end shopping centres are doing relatively well especially in the US as their shoppers have been more resilient on the whole. On the investment side you see the same trend as due to economic uncertainty investment volumes are decreasing, especially in the EMEA and Asian region."

Stephan Bruenner, Fondsmanager, "CS PortfolioReal A" (ISIN: DE0009751453) (06.07.2012): "Gegenwärtig wird die Stimmung an den Immobilienmärkten wohl weniger über das zyklische Auf und Ab im Laufe der normalen konjunktureller Schwankungen bestimmt, als vielmehr durch die Sorge um strukturelle und tiefgreifende Änderungen in der Marktdynamik dominiert. In diesem Kontext bleiben vergleichsweise sicher und liquide Immobilienmärkte bzw. -segmente weiter stark nachgefragt, wobei sich die Erwartung mittelfristig Zuwächse im Mietpreisniveau vielfach auf einen möglichen Trendbruch in den bislang problematischen Märkten stützt."

Mark Thorpe-Apps

Mark Thorpe-Apps, Fondsmanager, "UBS (CH) Inst Fd 2-Gl Real Estate Securities I-X" (ISIN: CH0022986407) (10.07.2012): "The new "normal" is low economic growth. Demographic trends, namely; lower birth rates and the aging of the population in OECD countries will cap trend economic growth. Trend GDP growth of 2% should be considered healthy. Bond rates have rallied to record lows in most developed countries. This augers well for most real estate markets and yield spreads are supportive of valuation. Supply is also contained in most markets. Overall, economic conditions are supportive of real estate investment."

Steve Burton

Steve Burton, Senior Global Portfolio Manager, "ING (L) Invest Global Real Estate P Cap EUR" (ISIN: LU0250172185) (11.07.2012): "The case for property companies remains strong in a world of sluggish economic growth. Listed property companies have many investment attributes that we believe are favorable in an uncertain “not too hot, not too cold” economic environment. This should provide support for the asset class, particularly among investors seeking a high component of current income in the total return proposition. These attributes include: (1) compelling relative yield in a low yield world with a generally positive near-term growth outlook; (2) historically stable cash flows generated from generally improving property fundamentals; and (3) attractive real estate valuations."

Webinar-Replay

60 Min.

Nicolas Schmidlin (ProfitlichSchmidlin AG) & Martin Roßner (ThirdYear...

e-fundresearch: "Which are the most important elements in your investment process?"

Guy Mountain

Guy Mountain, Real Estate Investment Manager, "Sarasin Sustainable Equity Real Estate Global B" (ISIN: LU0288928376) (10.07.2012): "For this fund the sustainable screening process done by Bank Sarasin’s Sustainable team (one of Europe’s largest sustainable investment units) is a key element of the investment process. Having screened our universe of listed real estate stocks using the Sarasin Sustainability-Matrix, we are left with 94 names from which to compose the portfolio. Asset allocation is determined from a top down approach guided by our investment policy committee, headed by our CIO and Macro Team, coupled with direct real estate research from our consultant Jones Lang Lasalle. We then use a bottom up approach for stock selection from the sustainable universe."

Marco van Bussel

Marco van Bussel, Portfolio Manager, "First State Global Property Securities A GBP Acc" (ISIN: GB00B1F76L55) (11.07.2012): "Real estate market fundamentals are highly dependent on local economic conditions, so our team incorporates asset-specific and region-specific micro and macroeconomic forecasts in its security valuation models. We invest a large proportion of our time meeting the management of property companies and inspecting their assets to assist in formulating a bottom-up assessment, of investments and markets. As part of this assessment we consider potential holdings based on value, asset quality, management quality, financial leverage and Environmental, Social and Governance (ESG) considerations."

Stephan Bruenner, Fondsmanager, "CS PortfolioReal A" (ISIN: DE0009751453) (06.07.2012): "Als bedeutsame Elemente in unserem Investitionsprozess haben sich einerseits die Portfolioallokation entlang geographischer Parameter und andererseits die Steuerung des Portfolios entlang typischer Risikoparameter der von uns investierten Investmentvehikel bewährt."

Mark Thorpe-Apps

Mark Thorpe-Apps, Fondsmanager, "UBS (CH) Inst Fd 2-Gl Real Estate Securities I-X" (ISIN: CH0022986407) (10.07.2012): "We apply disciplined valuation and scoring methodology throughout the whole investment process on macro factors, company fundamentals and valuations. We draw upon market consensus and in-house proprietary research to assign each stock a score that can be ranked within the subsector, country and region. The methodology reacts to price movements as well as changes to earnings and growth forecasts."

Steve Burton

Steve Burton, Senior Global Portfolio Manager, "ING (L) Invest Global Real Estate P Cap EUR" (ISIN: LU0250172185) (11.07.2012): "CBRE Clarion uses a multi-step investment process for constructing portfolios that combines top-down, research driven portfolio design with bottom-up securities selection based on intensive fundamental company analysis. CBRE Clarion has portfolio managers and analyst teams located in each of the world’s major regions, which allows the team to have a local presence in key property markets and have access to the resources and research of the global CBRE real estate platform. CBRE Clarion uses a proprietary system called Relative Value Analysis (“RVA”) that has been developed by the analysts over CBRE Clarion’s 25+ year history to provide a framework for security selection. The RVA system incorporates quantitative and qualitative factors that assist the analysts in evaluating performance characteristics of individual securities independently and relative to each other. Finally, CBRE Clarion’s portfolio construction and risk mitigation guidelines are employed to arrive at a well-diversified portfolio of global real estate securities."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Which over- and underweight positions are currently implemented in your global real estate funds?"

Guy Mountain

Guy Mountain, Real Estate Investment Manager, "Sarasin Sustainable Equity Real Estate Global B" (ISIN: LU0288928376) (10.07.2012): "At present, we are underweight Hong Kong and Singapore as we see the most rental pressure there and are wary of their exposure to China. In our conventional funds we focus on the landlord names and avoid the higher beta residential developers, and we try to replicate this in the sustainable funds, although we have a smaller sustainable universe in Asia. Japan is a region we have been positive on this year and it has been a strong performer - we are overweight the region in our conventional funds, while in the sustainable funds we are actually underweight due to the only sustainable stocks in the region being four high beta developers. However, though we are underweight on an asset allocation basis, we are overweight from a beta standpoint due to the lack of low beta JREITs. We have taken some money off the table in Japan on recent strength, as we are wary of the global economic and political situation, but we do believe that there are signs that Tokyo office vacancy and rental levels are showing signs of bottoming. As the strong supply pipeline tails off at the end of the year, the developer names that currently sit at significant discounts to their net asset values will benefit. We also favour Australia, finding the combination of relatively high dividend yields and scheduled annual rental uplifts particularly attractive at the prime end of the retail sector. Our last call is an underweight to Europe as the euro zone issues play out, and we have avoided significant exposure to the troubled southern European countries."

Marco van Bussel

Stephan Bruenner, Fondsmanager, "CS PortfolioReal A" (ISIN: DE0009751453) (06.07.2012): "Geographisch sind wir gegenüber unserer langfristigen Ausrichtung stärker in Asien und leicht in Nordamerika übergewichtet. Darüber hinaus streben wir eine weitere Diversifikation des Portfolios im Segment der offenen Immobilienfonds an und möchten gleichzeitig die Produktvielfalt unter den von uns investierten Produkten aus dem unteren Risiko-Rendite-Spektrum weiter ausbauen."

Mark Thorpe-Apps

Mark Thorpe-Apps, Fondsmanager, "UBS (CH) Inst Fd 2-Gl Real Estate Securities I-X" (ISIN: CH0022986407) (10.07.2012): "We have recently moved to market weight in most regions/countries. Valuations are fair given country specific conditions. Around the edges, we have started to U/W Australia and increase exposure to Canada."

Steve Burton

Steve Burton, Senior Global Portfolio Manager, "ING (L) Invest Global Real Estate P Cap EUR" (ISIN: LU0250172185) (11.07.2012): "During the quarter, we adjusted the strategy’s focus on the back of softening economic news and weaker growth, including a decrease in portfolio exposure to the more economically sensitive geographies, property types and business strategies. We continue to favor property companies in the U.S. and have a cautionary bias to those in Europe. We have reduced exposure to development companies in Asia and are now more cautiously positioned in this geographic region. By property sector, in the U.S., we are positive on the retail mall and apartment sectors and remain cautious on suburban office, health care, and shopping center sectors. In Europe, we favor office companies that focus on London’s West End submarket, and prefer dominant retail mall companies with exposure to the European Continent. In the Asia-Pacific region, we remain cautious on selected sub-sectors including Hong Kong and Singapore residential, given deteriorating housing affordability and increased government policy risk. We are also less favorable on Japanese REITs due to an expected overhang from pending equity issuance. Globally, we are generally positive on the retail property sector due to the stability of cash flows and their reasonable valuations, primarily high-quality malls."

Click on picture to enlarge!

Click on picture to enlarge!

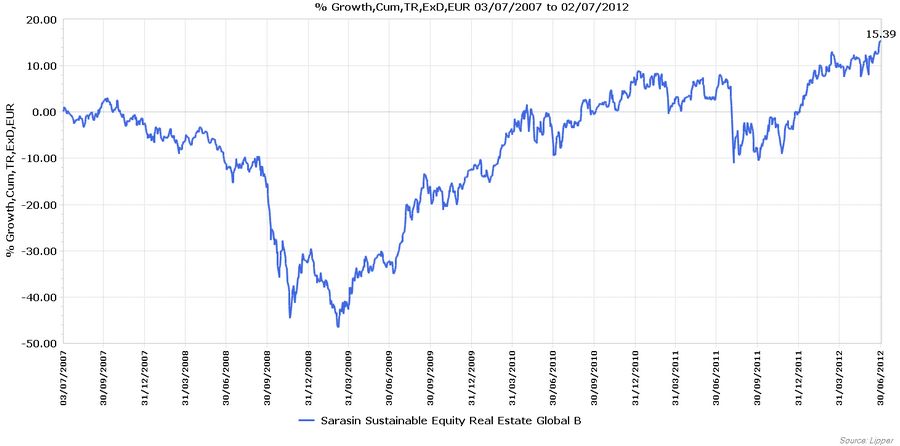

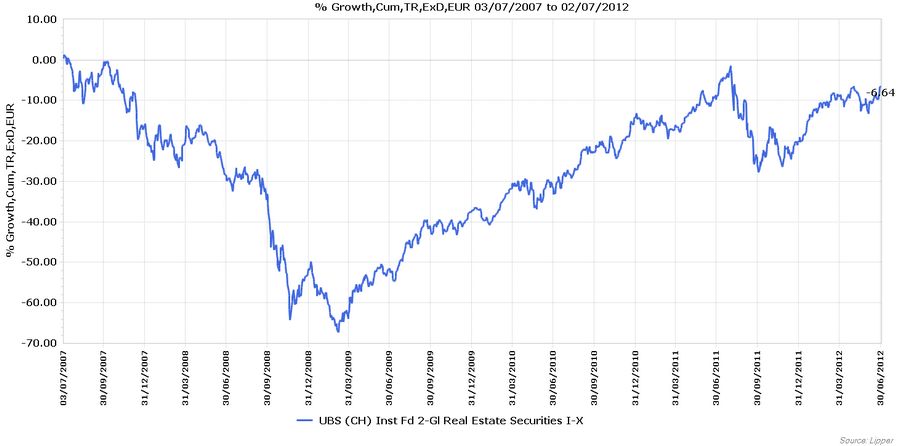

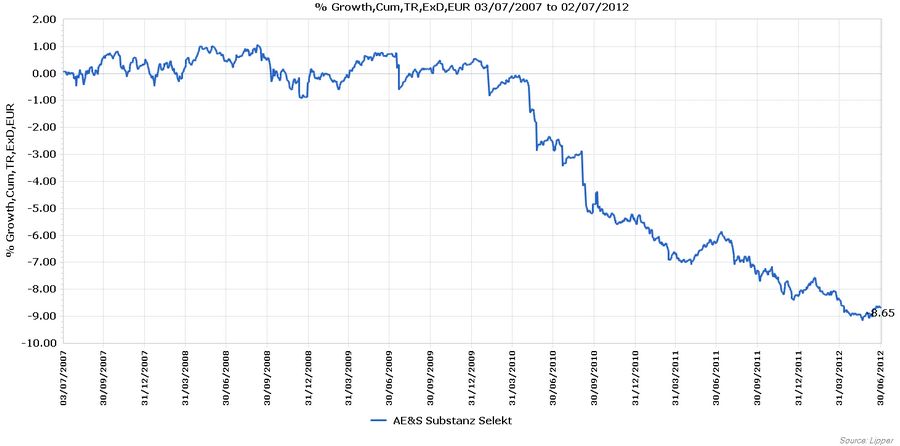

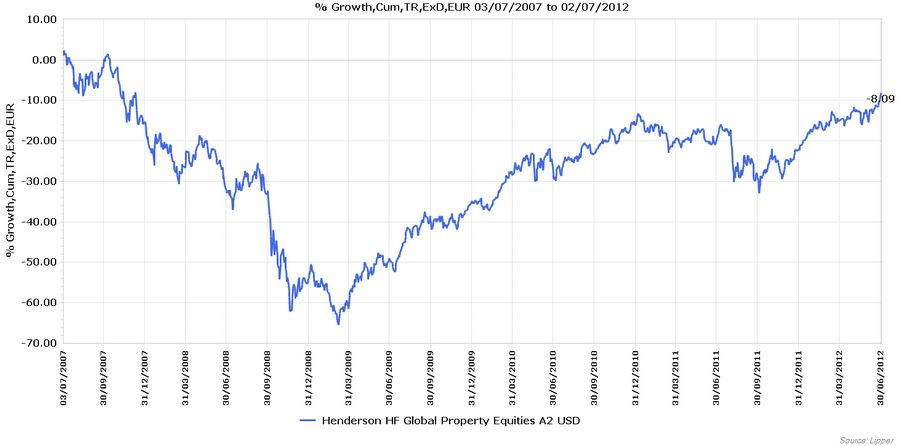

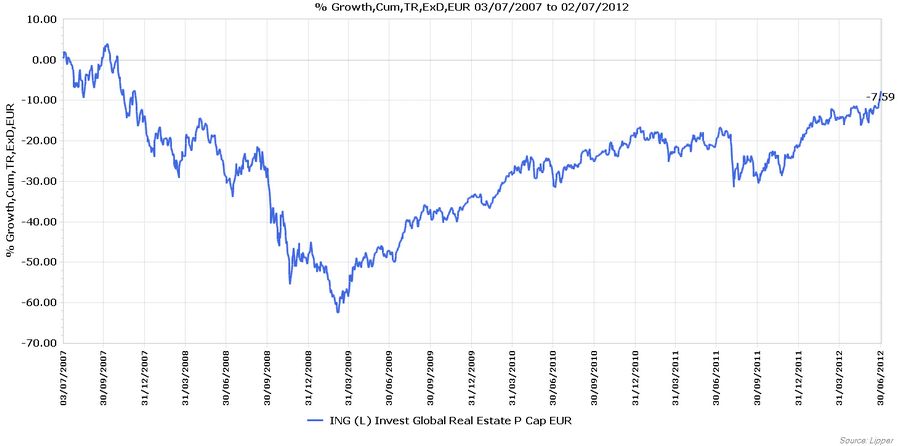

e-fundresearch: "Please comment on the performance and risk parameters of your fund in the current year as well as over the past 3 and 5 years."

Guy Mountain

Guy Mountain, Real Estate Investment Manager, "Sarasin Sustainable Equity Real Estate Global B" (ISIN: LU0288928376) (10.07.2012): "The fund switched to a sustainable fund in July 2009. In 2009 and 2010, the constraints of the sustainable filter did not help performance. Real estate companies with sustainable characteristics are usually those with good management teams, better assets, and stronger balance sheets – not characteristics helping performance when financing costs aided weaker, illiquid real estate companies. The reverse was true in 2011, and so far in 2012, as the key has been to invest in companies with the best quality and best located assets, good management teams, clearly attainable strategies and solid balance sheets. However, a lack of sustainable stocks in a number of regions and sectors has been frustrating. In 2011, the sad events of 11th March in Japan created the largest detractor from performance. At the start of the year there were only three high beta Japanese developers screening as sustainable that we were overweight (although underweight the region). This stock selection created significant alpha up until the earthquake when their higher beta nature caused them to sell off substantially more than the market. Sustainable exposure in Singapore has also been testing at times due to three out of the four sustainable names having exposure to the residential market (which suffered from continued policy intervention), although this year they have been the stronger performers.

At the outset of the fund in 2009 we only had approximately 60 names that screened as sustainable. We now have over 90 names in our investable universe, so the constraints created by the sustainable filter are continuing to decrease. We believe that sustainable legislation for real estate is still in its infancy, and with real estate responsible for approximately 40% of all CO2 emissions, and the fact that the additional cost to develop a building to a reasonable level of sustainability are minimal, it will continue to increase in importance as governments around the world look to reduce carbon footprints. We are already seeing some evidence that sustainable buildings are being rented and selling for more. In fact, we can envisage a time when all buildings - new or old - will have to meet some level of sustainability and therefore those companies ahead of the curve will be the winners.

The fund has an upper range tracking error used for risk monitoring of 8%. This is monitored on a monthly basis and is currently 4.2. Historically this has been as high as 6.5 in 2009.

The fund has also tended to have a higher volatility than its benchmark; currently at 23.8 against its benchmark of 22.8, but has never taken significant risk in excess of the index.

Sarasin targets liquidity below 10 days in its stock selection; currently the fund can sell 93% of the portfolio in 1 day assuming 20% of daily volumes can be traded.

S&P reviews portfolio risk and strategy implementation on a monthly basis against house policy and other managers for consistency of approach."

Marco van Bussel

Marco van Bussel, Portfolio Manager, "First State Global Property Securities A GBP Acc" (ISIN: GB00B1F76L55) (11.07.2012): "The First State Global Property Securities Fund is invested in a broad portfolio of global property securities. It is diversified across the residential, office, retail, industrial and hotel sectors. Based on performance to 30 June 2012 the First State Global Property Securities Fund has produced first quartile returns over 1, 3 and 5 years, outperforming its peer group over the same timeframes."

Stephan Bruenner, Fondsmanager, "CS PortfolioReal A" (ISIN: DE0009751453) (06.07.2012): "Die Performance der letzten 3 bzw. 5 Jahre umfasst eine außergewöhnliche Marktphase. Zunächst wurde unser Portfolio mit Kursverlusten im Bereich der Immobilienaktien, dann mit Konsolidierung im Segment der offenen Immobilienfonds konfrontiert. Dennoch gelang es mit Blick auf die langfristig orientierten Anleger im Fonds eine insgesamt über die Zeit zufriedenstellende Performance zu erzielen."

Mark Thorpe-Apps

Mark Thorpe-Apps, Fondsmanager, "UBS (CH) Inst Fd 2-Gl Real Estate Securities I-X" (ISIN: CH0022986407) (10.07.2012): "The portfolio generally holds around 80 securities from a benchmark in excess of 300 holdings. Over the past 5 years, the tracking error has ranged between 2% to 4%. The beta relative to the benchmark is 1.01 over the longer term. Our risk factors are mainly in the stock specific risk, while the risks related to size and country are minimum."

Steve Burton

Steve Burton, Senior Global Portfolio Manager, "ING (L) Invest Global Real Estate P Cap EUR" (ISIN: LU0250172185) (11.07.2012): "The major risks for the global real estate securities market are the same risks facing most asset classes, including the uncertainty in the global macro-economic picture. The thesis for a continued gradual global economic recovery is being tested by a number of familiar risks. First among these risks is the euro-zone debt crisis, which has become a more tenuous situation as a result of an increased probability that Greece may leave the euro zone, with associated implications for the broader financial system. Second is the risk of a stalling economic recovery in the U.S., which has suffered through two consecutive disappointing employment reports and a number of other disappointing economic releases. Third is the risk of an economic slowdown in China which may be materially weaker than consensus growth expectations. The Chinese government’s ability to manage this slowdown, particularly in light of negative economic developments in Europe and the U.S., remains somewhat unknown despite the many monetary and fiscal levers available to the Chinese central government."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "What are the major risks for global real estate equities?"

Guy Mountain

Guy Mountain, Real Estate Investment Manager, "Sarasin Sustainable Equity Real Estate Global B" (ISIN: LU0288928376) (10.07.2012): "The risks come from the two possible extremes: a sudden deterioration in the economic recovery and a seizing up of the lending market, or, conversely, a stronger than expected recovery creating a rotation from yielding assets into general equities."

Marco van Bussel

Marco van Bussel, Portfolio Manager, "First State Global Property Securities A GBP Acc" (ISIN: GB00B1F76L55) (11.07.2012): "The major risks at the moment are still a deepening crisis within the Euro area which would have a knock-on effect to other regions and also a more severe slowdown in China which would have major consequences globally."

Stephan Bruenner, Fondsmanager, "CS PortfolioReal A" (ISIN: DE0009751453) (06.07.2012): "Bedeutsame Risiken für globale Immobilienaktien könnten sich aus heutiger Sicht aus möglichen Veränderungen in der Zinslandschaft, dem regulatorischen Umfeld oder/und durch externe Schocks entfalten."

Mark Thorpe-Apps

Mark Thorpe-Apps, Fondsmanager, "UBS (CH) Inst Fd 2-Gl Real Estate Securities I-X" (ISIN: CH0022986407) (10.07.2012): "As real estate is a capital intensive sector, interest rate movement remains the major risk for our segment. Therefore, we actively monitor the spread between the dividend yield/cash flow yield vs the short term interest rate/5-year interest rate among the countries, and actively allocate accordingly in order to arbitrage the spread opportunities."

Steve Burton

Steve Burton, Senior Global Portfolio Manager, "ING (L) Invest Global Real Estate P Cap EUR" (ISIN: LU0250172185) (11.07.2012): "We believe total returns for property stocks will continue to be anchored by an average dividend yield which remains in the 3-4% range and earnings growth that we project both this year and next to be solidly in the mid single-digits. With real estate valuations trading below private market values, we continue to support the expectation that the sector can conservatively return a high single-digit total return over the course of the coming year."

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.