Die Fondsmanager der besten Pharma- und Healthcare-Aktienfonds haben exklusiv fünf Fragen zu den fundamentalen Faktoren, ihrem generellen Marktausblick sowie zu Gewichtungen und Performances beantwortet. Welche Elemente sind die wichtigsten in ihrem Investmentprozess?

Funds

| 30.07.2012 02:00 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

Click on picture to enlarge!

e-fundresearch: "Which fundamental factors are currently the most important ones when you assess pharma and healthcare stocks?"

Harald Kober

Harald Kober, Fondsmanager, "ESPA STOCK PHARMA EUR A" (ISIN: AT0000746771) (25.07.2012): "Der gesamte Pharma-Sektor zeichnet sich durch eine gute Dividendenrendite aus. Aktuell liegt die Dividendenrendite bei knapp 4% Die Dividenden werden durch solide Unternehmensbilanzen untermauert, d.h. es sind „gesunde“ Ausschüttungen. Es besteht daher momentan auch keine Gefahr, dass die Dividenden gekürzt werden. Die Gewinnentwicklung für den Sektor ist positiv. Wir rechnen für die nächsten Jahre mit einem Gewinn-Wachstum im mittleren einstelligem Bereich, gepaart mit steigenden Ausschüttungen. Der Pharmasektor ist die einzige Branche, die Gewinnwachstum und nachhaltig hohe Dividendenrendite vereint."

Paulina Niewiadomska

Paulina Niewiadomska & Michael Sjöström, Fund Manager Team, "Pictet-Generics-P USD" (ISIN: LU0188501257) (23.07.2012): "Key criteria include age and composition of product portfolio / pipeline / exposure to emerging markets / reimbursement issues and pricing power as well as management quality."

16.09.2025 11:00

45 Min.

Adrian Daniel, Frank Schwarz und Jan-Christoph Herbst

Erin Xie

Youri Amerijckx

Youri Amerijckx, Fund Manager, "KBC Equity Pharma Growth Cap" (ISIN: BE0177733293) (25.07.2012): "Valuation vs Potential (Valuation: 12mfwPE, 12m FW PE to Long Term Growth, 12FW EV/EBITDA etcetera, Potential: Long Term Growth, based on existing and future pipeline etc) Assessment of competitive landscape, impact of (bio)generics etcetera..."

Gemma Game

Gemma Game, Fund Manager, "AXA Framlington Health R Inc" (ISIN: GB0005753719) & "AXA WF Framlington Health A USD" (ISIN: LU0266013472) (23.07.2012): "This can be split into top down, thematic factors and bottom up, company specific factors. Top down factors include the political, regulatory and macroeconomic environments. The political environment is important in assessing the evolution of healthcare reform in the US and the pricing environment for Europe and Emerging Markets. The regulatory environment is important in assessing the lenience of the regulatory authorities in approving new biopharmaceuticals and medical devices. The macroeconomic environment is important in assessing the attractiveness of the Healthcare sector relative to other sectors in the broader markets. Bottom up factors that are important in assessing healthcare and pharma stocks include the competitive position of key products in their therapeutic area, growth of the patient population that these products treat, the patent expiry dates for these assets and the pipeline of new products that can replace the existing revenue base post patent expiry."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "What is your general outlook for pharma and healthcare stocks over the coming 12-18 months? Where do you see opportunities and where are the risks?"

Harald Kober

Harald Kober, Fondsmanager, "ESPA STOCK PHARMA EUR A" (ISIN: AT0000746771) (25.07.2012): "Der Pharmasektor zeigt sich in guter Verfassung angesichts der sehr volatilen Aktienmärkte und den zuletzt eingetrübten Konjunkturdaten. Als defensiver Sektor ist der Pharmasektor nicht so sehr vom allgemeinen Wirtschaftswachstum abhängig. Medikamente werden immer benötigt, ihr Bedarf steigt ständig. Die Bewertung von Pharma-Aktien ist auf dem aktuellem Niveau angemessen und noch nicht überzogen. Hinzu kommen noch die M&A Aktivitäten im Sektor. Pharmaunternehmen sind auf der Suche nach neuen Wirkstoffen und Medikamenten, um ihre wegen Patentabläufen reduzierte Pipeline aufzufüllen. Die Risiken liegen in einem Anspringen des Wirtschaftswachstums und damit verbunden mit einer Sektor-Rotation, d.h. dass Investoren ihr Interesse an defensiven Sektoren verlieren und sich eher den zyklischen Sektoren (zB Technologie, Konsum) zuwenden."

Michael Sjöström

Paulina Niewiadomska & Michael Sjöström, Fund Manager Team, "Pictet-Generics-P USD" (ISIN: LU0188501257) (23.07.2012): "We continue to see opportunities among innovation driven companies, in particular in medtech and biotech, as well as in companies benefiting from increasing purchasing power in emerging markets. The latter include generic drug makets, hospital supply companies and hospital management companies. The main headwind remains a difficult pricing environment with mounting pricing pressure and reimbursment limitations, in particular in developed economies."

Erin Xie

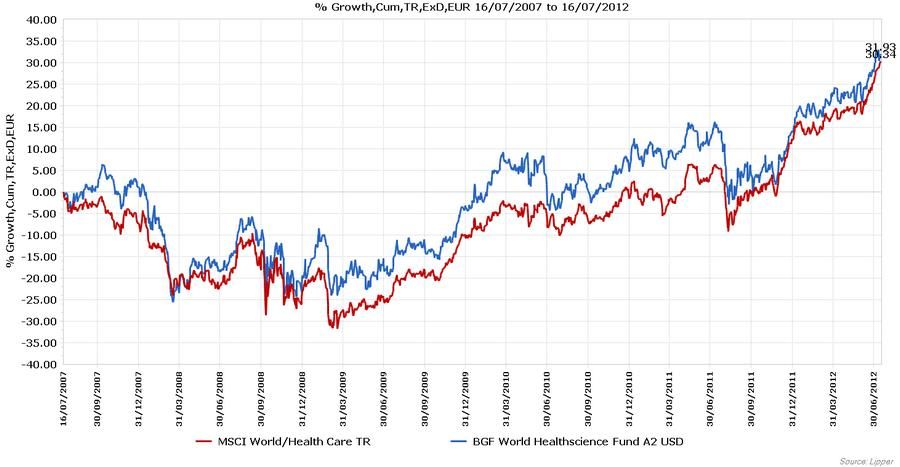

Erin Xie, Fund Manager, "BGF World Healthscience Fund A2 USD" (LU0122379950) (30.07.2012): "Overall, we believe healthcare valuations are attractive, however, policy headwinds remain. Fortunately, one policy event, the Supreme Court review of the Patient Protection & Affordable Act (PPACA) has been resolved with the Supreme Court upholding the Healthcare Reform law in the US. Since the individual mandate was not overturned, the 30mm people that are uninsured will be required to acquire health insurance, although approximately half will be eligible for Medicaid and individual states can still determine whether they can expand their Medicaid plans. Overall, the entire healthcare ecosystem will benefit since 30mm people will now be part of the healthcare system and one would expect to see an increase in physician visits, procedures, drug prescriptions, etc. starting in 2014.

While the implementation of Healthcare Reform is a positive for most healthcare companies as the uninsured population receive insurance coverage, we think the upside of the healthcare stocks may not fully materialize in the short term, as investors wait for the U.S. Presidential election outcome this Fall and the pending fiscal cliff to be resolved by Congress later this year. Meanwhile, as global economy slows down, healthcare stocks offer good defensive characteristics and could continue to outperform if macro economy continue to struggle."

Youri Amerijckx

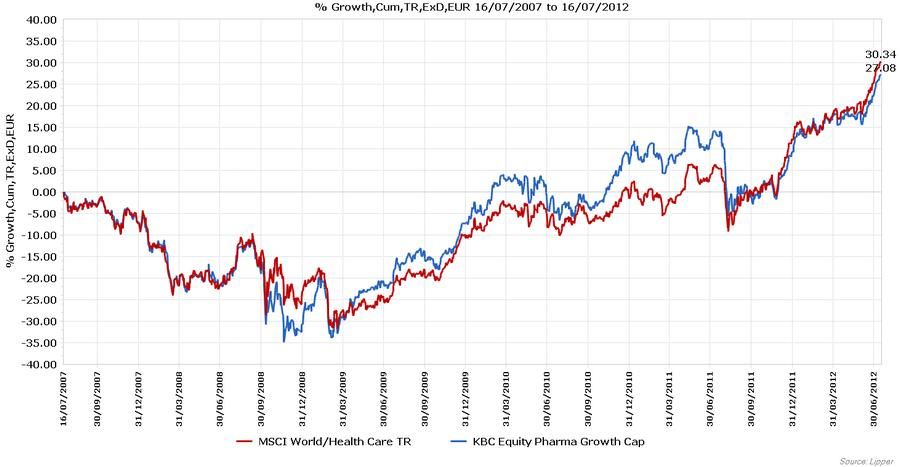

Youri Amerijckx, Fund Manager, "KBC Equity Pharma Growth Cap" (ISIN: BE0177733293) (25.07.2012): "Positive: vs the market. Euro potentially breaking up, healthcare is a more or less safe haven. A wave of new products upcoming at Big Pharma and Biotech. A lot of M&A. US hospitals enjoying effects of Obamacare. Watch out for Election rethorics in the US. Equipment negative: lack of innovation, pricing pressure, high depency on discretionary spending in some cases. Pockets of value to be found in the sector, though."

Gemma Game

Gemma Game, Fund Manager, "AXA Framlington Health R Inc" (ISIN: GB0005753719) & "AXA WF Framlington Health A USD" (ISIN: LU0266013472) (23.07.2012): "I expect the outlook for the healthcare stocks to be very dynamic over the next 12-18 months. The healthcare sector is a diverse group of more than 20 industries, from the high beta biotechnology industry through to the lower beta industries such as the drug wholesalers. Some industries such as pharmacy benefit managers are experiencing secular growth, and others areas such as the medical technology and biotechnology industries are exhibiting rapid growth of new product launches. The fundamentals for the pharma stocks are likely to be more pedestrian as the industry is currently in a multi year period of low sales and earnings growth as it moves through the patent cliff, where lots of products are losing patent protection and the sales are reapidly declining as a result of this. The opportunities at the moment are in companies that can deliver truly innovative, novel products (devices, or drugs) as well as companies that improve the efficiency of the healthcare system or lower costs of providing healthcare, such as the Healthcare IT and Managed Care industries respectively. The risks to the sector are that political (uncertainty around the impact of the US Presidential election in November), regulatory (uncertainty over the approval of new products and devices) and clinical (whether the clinical trials that companies run on their products and devices are successful or not)."

Click on picture to enlarge!

Click on picture to enlarge!

Harald Kober

Paulina Niewiadomska

Paulina Niewiadomska & Michael Sjöström, Fund Manager Team, "Pictet-Generics-P USD" (ISIN: LU0188501257) (23.07.2012): "The fund adopts a meticulous and well-disciplined bottom-up driven approach, comprising the following five steps: Idea generation, Analysis of Fundamentals, Valuation, Recommendation and Implementation. The Pictet-Generics fund adopts a growth-biased, non-benchmark approach. The fund has an Advisory Board which is composed of reputed experts from the industry, research or with a regulatory background. The Advisory Board members support the investment management team in identifying future trends, that offer above-average growth potential.

Michael Sjöström

The investment universe includes manufacturers and distributors of cheaper, bioequivalent copies of branded drugs (generics) and of improved versions of branded drugs (specialty pharmaceuticals).The fund focuses on companies exposed to countries with emerging pharmaceutical markets or with low generic use, as well as on niche players and specialty formulators located mainly in North America, Europe and Asia."

Erin Xie

Erin Xie, Fund Manager, "BGF World Healthscience Fund A2 USD" (LU0122379950) (30.07.2012): "Our investment team conducts bottom-up fundamental research to better understand the businesses, product potential and fair valuations of investment candidates. As each potential investment candidate is identified, the research analyst pursues intensive fundamental analysis. This analysis includes a review of business economics and industry fundamentals, an examination of the company's competitive position within its industry, independent field checks of each company’s products to monitor market demand change, and sophisticated financial analytics. Company visits and industry conferences play an integral role in assessing a company’s potential for inclusion in the portfolio. The research process is highly collaborative, with portfolio managers and analysts, combing their blend of scientific and financial acumen to work in partnership to conduct analysis and generate new investment ideas."

Youri Amerijckx

Youri Amerijckx, Fund Manager, "KBC Equity Pharma Growth Cap" (ISIN: BE0177733293) (25.07.2012): "Assesment of pipeline and potential, competitive strengths, management quality, dividends, share buy back policy, capital structure, liquidity, cash position, pricing strength."

Gemma Game

Gemma Game, Fund Manager, "AXA Framlington Health R Inc" (ISIN: GB0005753719) & "AXA WF Framlington Health A USD" (ISIN: LU0266013472) (23.07.2012): "The most important elements in the investment process are threefold: 1) bottom up, stock picking: investment ideas can come from company meetings with management or medical meetings where clinical trial data is presented 2) thematic overlay: drawing from the common political, regulatory and clinical newsflow we ccan identify certain themes that can be applied to the portfolio. For example, the themes running through the fund today are investing in cost savings/ efficiency and investing in innovation. 3) sell discipline: constantly re-evaluating whether the original investment thesis is intact and whether valuation remains attractive."

Click on picture to enlarge!

Click on picture to enlarge!

Harald Kober

Paulina Niewiadomska

Paulina Niewiadomska & Michael Sjöström, Fund Manager Team, "Pictet-Generics-P USD" (ISIN: LU0188501257) (23.07.2012): "The fund's investment process is purely bottom-up driven. As such the portfolio is not benchmark constrained and has not any over- and underweight positions. Therefore, our top 10 holdings represent our biggest convictions."

Erin Xie

Erin Xie, Fund Manager, "BGF World Healthscience Fund A2 USD" (LU0122379950) (30.07.2012): "As of June 30, 2012, the largest sub-sector overweight for the portfolio was biotechnology with approximately 28% of the Fund allocated to this sub-sector. The impetus for this overweight was the identification of multiple biotechnology companies showing promising innovative technologies that meet an unmet medical need or are an enhancement to a current product or procedure. Conversely, our largest underweight, relative to the MSCI World Healthcare Index, is pharmaceuticals. It is important to note that the Fund will typically be underweight this sub-sector relative to the large benchmark allocation (approx. 64% as of 6/30/2012)."

Youri Amerijckx

Youri Amerijckx, Fund Manager, "KBC Equity Pharma Growth Cap" (ISIN: BE0177733293) (25.07.2012): "Regional neutral (US, P-EUR, ROW); Overweight big biotech; overweight emerging biotech; neutral big pharma; overweight specialty pharma (resulting in neutral for combined big and specialty) strong underweight equipment; neutral HC services."

Gemma Game

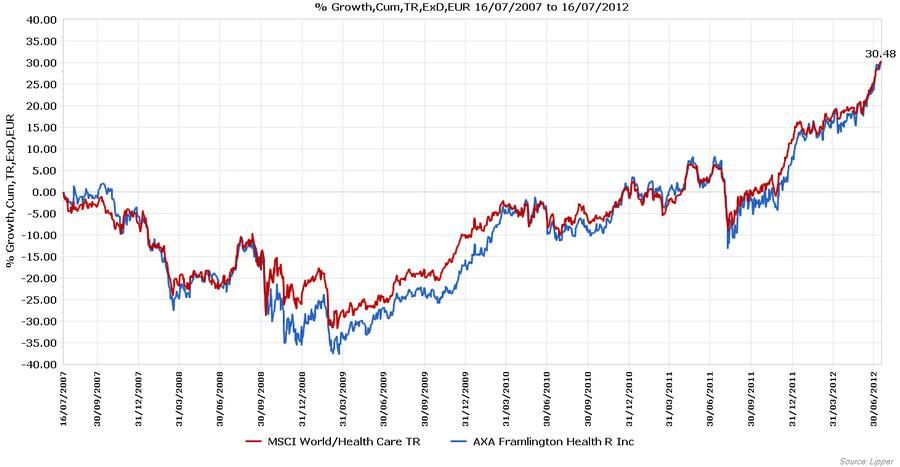

Gemma Game, Fund Manager, "AXA Framlington Health R Inc" (ISIN: GB0005753719) & "AXA WF Framlington Health A USD" (ISIN: LU0266013472) (23.07.2012): "We are underweight the pharma sector and overweight healthcare services, medical technology and biotechnology."

Click on picture to enlarge!

Click on picture to enlarge!

Harald Kober

Michael Sjöström

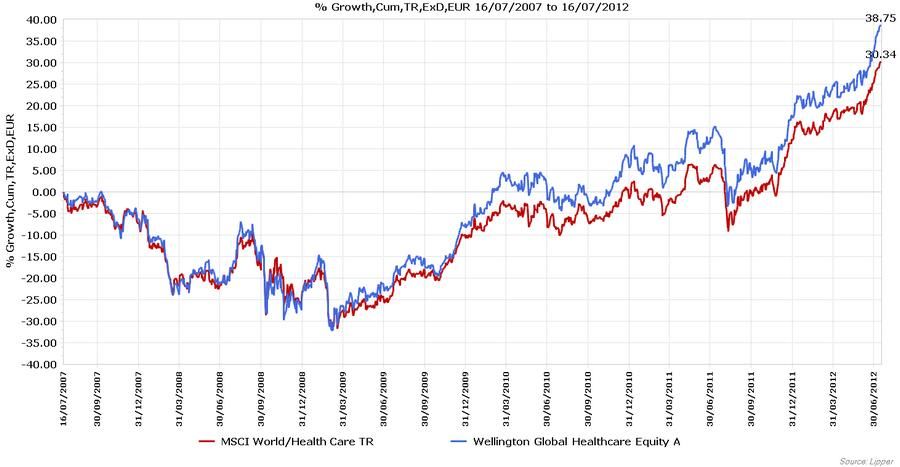

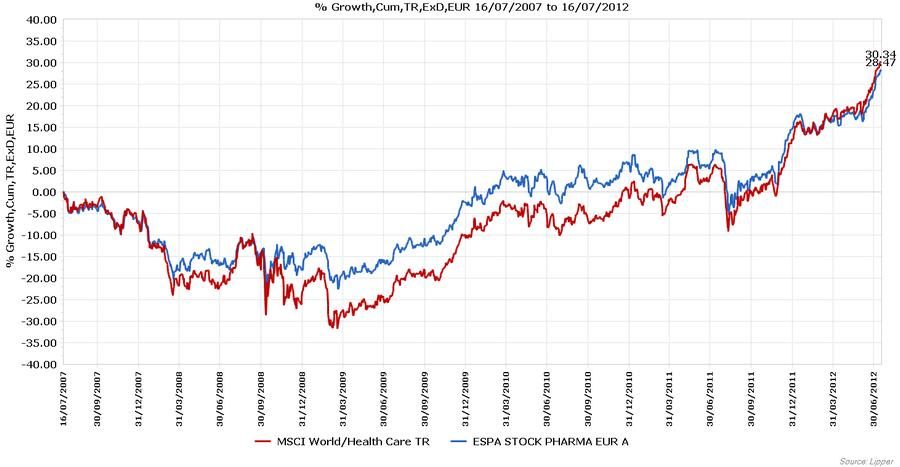

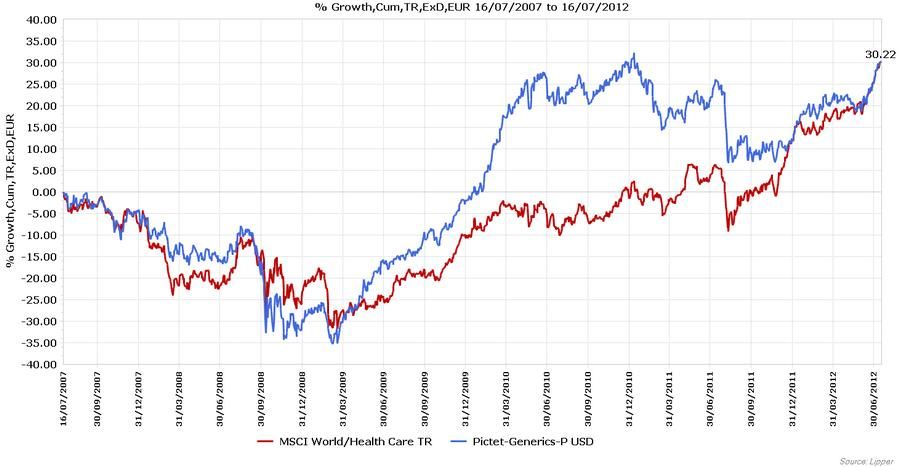

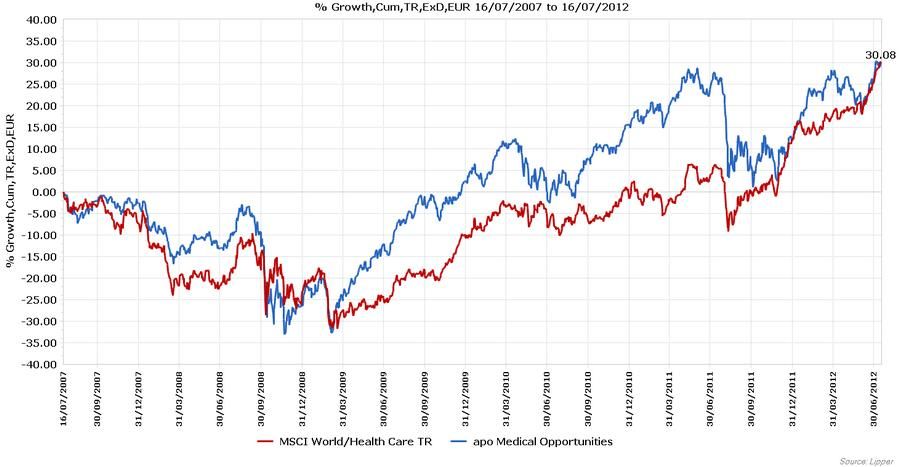

Paulina Niewiadomska & Michael Sjöström, Fund Manager Team, "Pictet-Generics-P USD" (ISIN: LU0188501257) (23.07.2012): "The Pictet Generics Fund outperformed the MSCI World Pharma Index over the last five years. Since there is no overlap between the fund and the index, a performance attribution cannot be calculated. However, given the process is strongly bottom-up oriented, stock selection is the key performance determinant."

Erin Xie

Youri Amerijckx

Gemma Game

Gemma Game, Fund Manager, "AXA Framlington Health R Inc" (ISIN: GB0005753719) & "AXA WF Framlington Health A USD" (ISIN: LU0266013472) (23.07.2012): "The fund has performed in line with the benchmark over the past 5 years, returning 3.21% on an annualized basis, compared to the benchmark MSCI World Healthcare Index TR of 3.33% on an annualized basis."

Click on picture to enlarge!

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.