Stuart M Stanley, CFA, High Yield Portfolio Manager, "Invesco Extra Income Bond T" (ISIN: AT0000673892) (15.08.2012): "We are expecting a slowing global economy over the next year, weighed down by a turgid and bifurcated European economy and slowing Chinese growth. Developing economies too could see lower growth as commodity prices continue to show some weakness. A slightly weaker macro picture itself, however, should not have a major impact on the more stable high yield companies which should continue to generate free cash flow to comfortably service their debts."

Folglich rechnen wir weiterhin mit sehr geringem Quartalswachstum deutlich unter Potential. Negative Quartale sind weiterhin nicht auszuschließen. Für das Gesamtjahr 2013 erwarten wir insgesamt geringfügig positives Wachstum."

|

e-fundresearch: "Which are the most important elements in your investment process?"

Stuart M Stanley, CFA, High Yield Portfolio Manager, "Invesco Extra Income Bond T" (ISIN: AT0000673892) (15.08.2012): "Our high yield investment process is mostly bottoms up, but is guided by our thoughts on the macro picture which includes our view of the economy and valuations. Our bottoms up work is done on a company-by-company basis as we search for value and strengthening creditworthiness to create returns. Our top down work helps us to tactically identify broader-based market opportunities and when risk-taking is most likely to be rewarded and when it is potentially most dangerous. We also tend to focus less on the largest cap bond structures as we have the flexibility and research capabilities to deal with medium and small cap structures, though we typically avoid illiquid names."

Darüber hinaus steuern wir auf Portfolio-Ebene die Sensitivität des Fonds gegenüber Veränderungen der Risikoprämien. Dies geschieht im Rahmen des Top-Down-Managements indem Investitionsgrad, Ratingallokation, und Portfolio Duration verändert werden."

|

e-fundresearch: "How do you assess the current development of the spreads vs. government bonds as well as the default rate?"

Stuart M Stanley, CFA, High Yield Portfolio Manager, "Invesco Extra Income Bond T" (ISIN: AT0000673892) (15.08.2012): "The global high yield spread according to Bank of America-Merrill Lynch indices is 620bp and the yield is 7.3%. The yield is not overly compelling on a historical basis but the spread is in line with long-term averages. Yields are held down by low government yields but we do not expect the low yield environment to change anytime soon. The high yield spread is pricing in benign outcomes to the US fiscal budget standoff and the European sovereign debt crisis but is pricing in a higher levels of defaults. Implied defaults in today’s spreads are greater than 6% while expectations are for much lower defaults – in the 3-4% area, which is below historical averages. We’d suggest that the strong demand for cash credit and high yield, supported by record high yield inflows in 2012, is keeping spreads slightly tighter than they might normally be."

Wir rechnen mit einem künftigen Rückgang der durchschnittlichen Kreditqualität. Dieser Trend ist bereits in der Ratingmigration zu beobachten. Auch künftig werden Rating-Herabstufungen voraussichtlich überwiegen, ihr Ausmaß wird aber u.a. davon abhängen wie gläubigerfreundlich künftige Managemententscheidungen ausfallen. Bei weiterhin stagnierendem Wirtschaftswachstum liegt der unmittelbare Managementfokus vermutlich weiterhin auf Cash Flow-Generierung und Bewahrung der Liquidität.

Steigenden Ausfallsrisken sind auch in aktuellen Marktniveaus reflektiert. Die impliziten Anstiege entsprechen nicht unseren Erwartungen. Folglich erachten wir Risikoprämien als adäquat. Insbesondere im Vergleich zu Staatsanleihen erscheinen spekulative Unternehmensanleihen attraktiv. Im niedrigen Zinsumfeld und aufgrund der Unsicherheiten im Zuge der Staatsschuldenkrise erfreut sich die Assetklasse zunehmender Beliebtheit. Die Möglichkeit einer breiten Diversifikation bei gleichzeitig höheren Renditen lockt stetig weitere Käuferschichten an. Ein Engagement in der Assetklasse eignet sich aufgrund der charakteristischen Volatilität des High Yield Markts aber nur für risikobewusste Investoren unter Berücksichtigung der ausgeprägten Mark-to-Market-Risiken mit entsprechend langer Haltedauer."

|

e-fundresearch: "Which over- and underweight positions are currently implemented in the High Yield portfolio?"

Stuart M Stanley, CFA, High Yield Portfolio Manager, "Invesco Extra Income Bond T" (ISIN: AT0000673892) (15.08.2012): "The portfolio is currently positioned to benefit from today’s market environment with sector overweight positions in financials, basic industries, transportation. Underweights include wirelines and consumer cyclical including European autos. Sector weights are generally the result of individual security selections and thus may differ from an overall sector view. For example, we like European cable names but find them very rich and are thus underweight. The portfolio is also overweight single B credits vs double Bs. This reflects again tightness in some double B names as a result of investment grade accounts buying them. And finally, irrespective of the particular sectoral weightings, our picks should all do reasonably well in a slowing economy."

Zwar ist die Sektorallokation Ergebnis der Einzeltitelselektion, dennoch lassen sich auch im Aggregat Positionierungen erkennen. Wenngleich die EBA-Vorgaben mehrheitlich erreicht wurden besteht im Bankensektor weiterhin Rekapitalisierungsbedarf. In Verbindung mit immer wieder aufkeimender Unsicherheiten hinsichlich eines „Bail-In“, sprich der Beteiligung aller Gläubiger im Falle einer Schuldenrestrukturierung sind wir bei Finanzwerten weiterhin selektiv und tendenziell untergewichtet.

Angesichts mangelnder Wachstumsimpulse zählen zyklische Branchen wie die Automobilindustrie und Chemiewerte zu den größten Untergewichten. Die Aussichten für Kabelnetzbetreiber schätzen wir hingegen weiterhin positiv ein. Unsere Einschätzung basiert auf den technologische Wettbewerbsvorteilen, der robusten Ertragslage, sowie den gesunden Liquiditätsprofilen."

|

e-fundresearch: "Please comment on the performance and risk parameters of your fund in the past year as well as over the past 3 and 5 years."

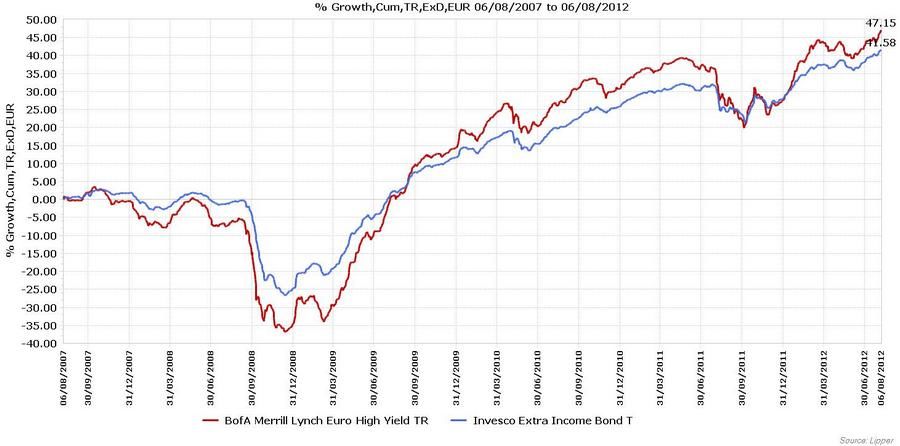

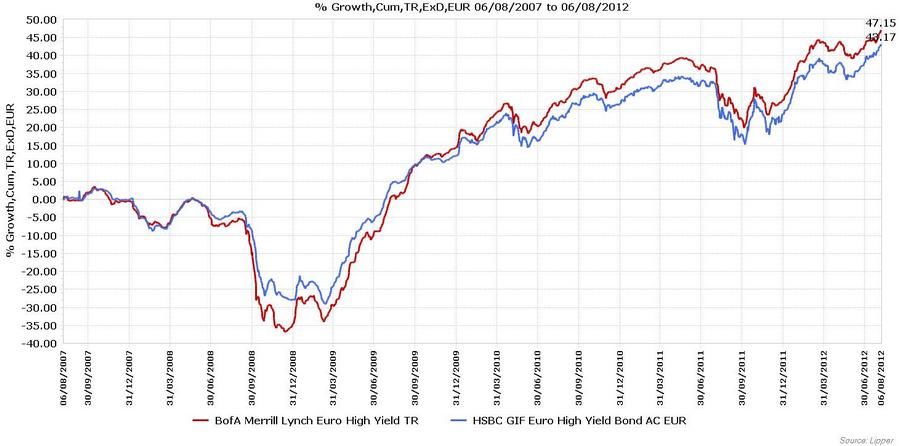

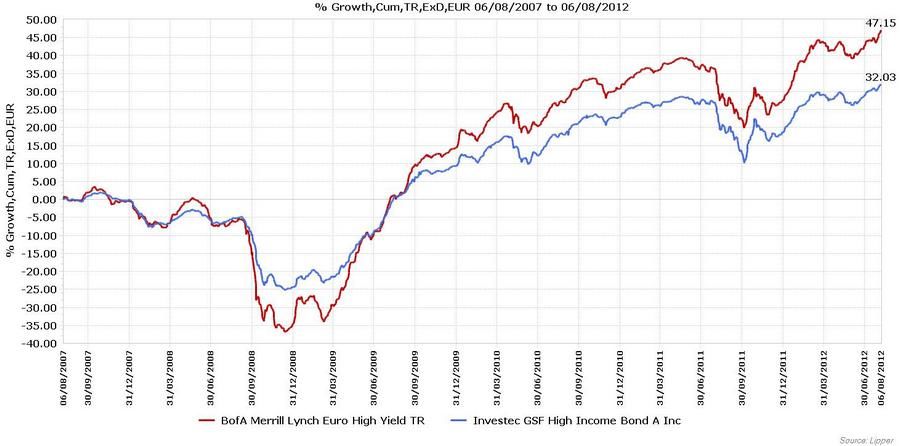

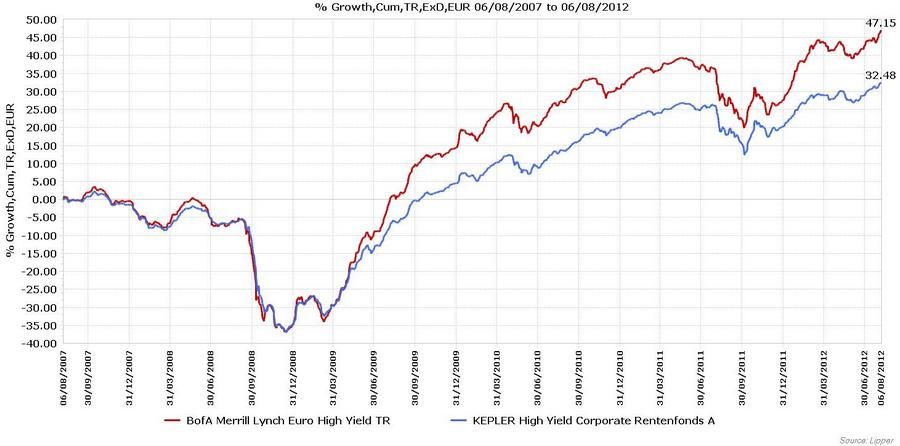

Stuart M Stanley, CFA, High Yield Portfolio Manager, "Invesco Extra Income Bond T" (ISIN: AT0000673892) (15.08.2012): "As of the end of July 2012, the fund’s annualized performance before fees over the past 1, 3, and 5 years was 7.16%, 12.39%, and 7.43%, respectively. Within its peer group as defined by Morningstar, the fund placed in the 1st, 2nd, and 1st quartile over the same periods. Volatility over those periods was 9.5%, 7.04%, and 12.34%, respectively. Due to the high diversification of the fund with 212 issues and 163 issuers and 55% invested in the US and the remainder in Europe, the fund generally exhibits lower volatility than its market and peers."

|

Fortsetzung der Artikelserie am 27. 8. 2012:

Lipper Global - Equity Europe

(für GRATIS newsletter anmelden)

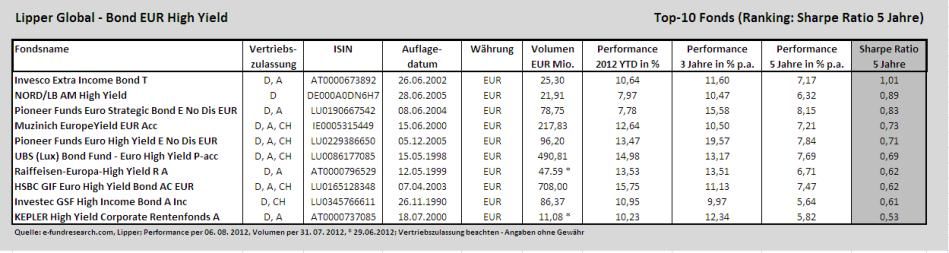

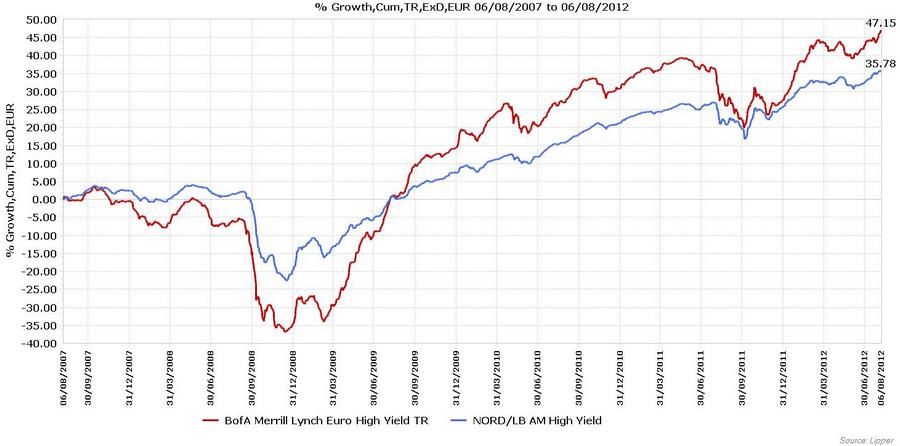

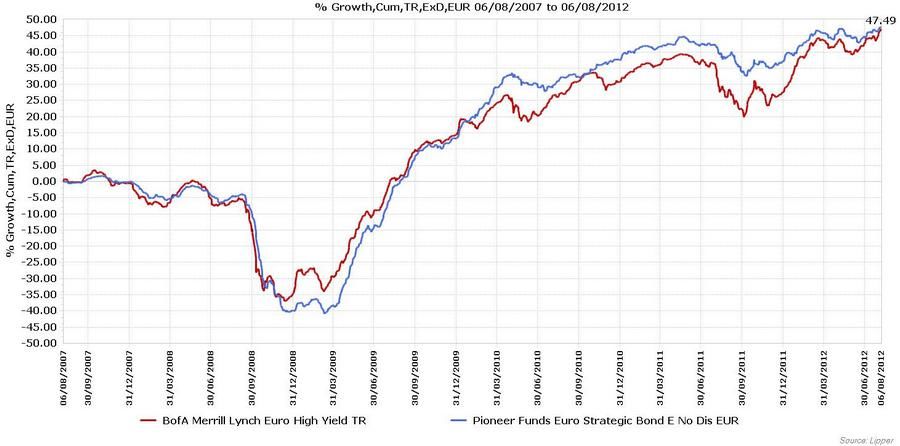

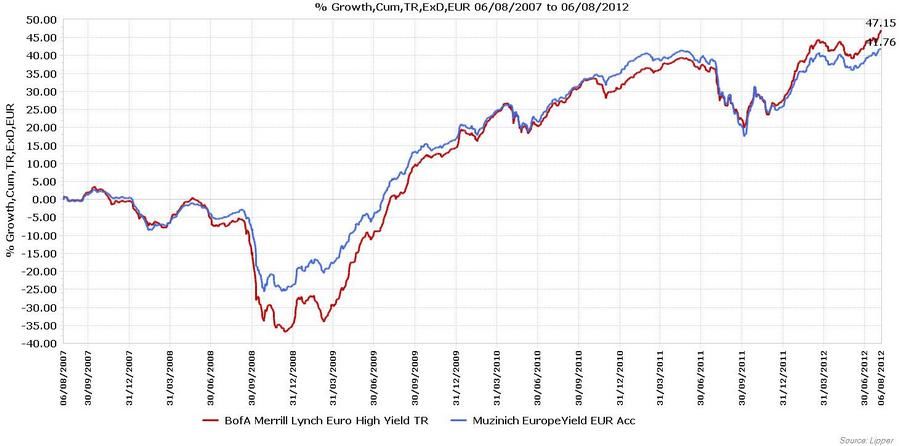

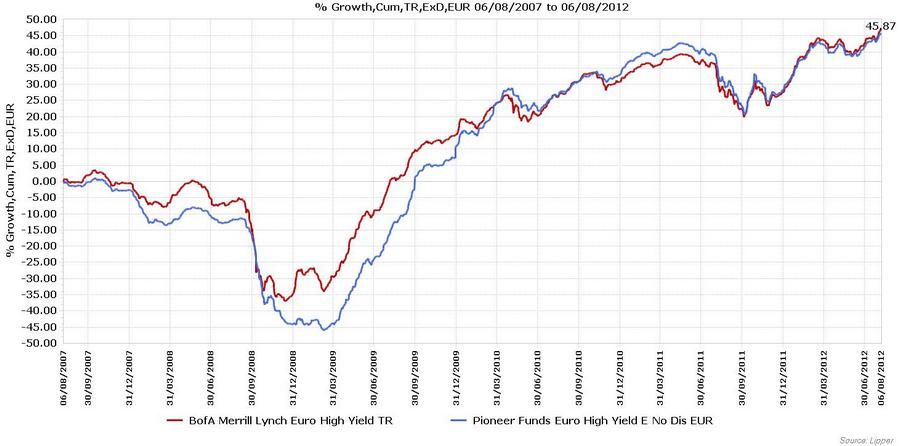

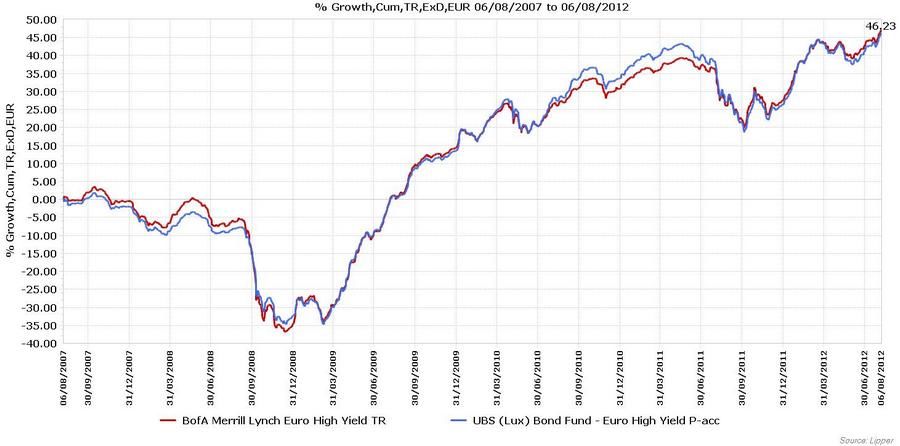

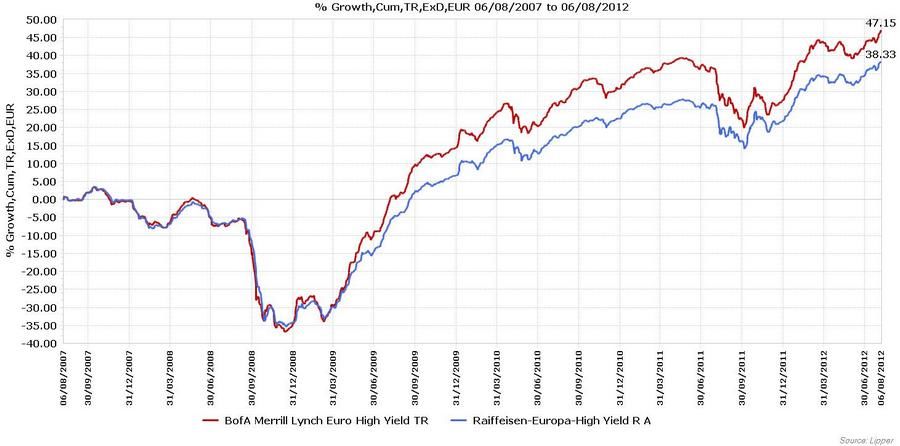

Alle Performance Daten der Top-10 Auswertung per 06.08.2012:

Weitere beliebte Meldungen: