Jagd nach Rendite: Wie positionieren sich globale Fixed-Income Manager vor dem Hintergrund eines sich weiter verbreitenden Negativ-Zinsumfelds sowie stärker divergierender Zentralbankpolitiken? Interview Nr. 4 mit Ariel Bezalel, Jupiter Dynamic Bond SICAV.

Managers

| 10.03.2015 12:00 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

e-fundresearch.com: What are your personal lessons learned from 2014 market developments?

Ariel Bezalel: Amid a challenging year for the flexible bond sector overall, the Jupiter Dynamic Bond SICAV returned 6.31% in 2014. For much of the year duration was at the shorter end of the scale and on the back of rising deflationary fears we aggressively increased duration in late Q3. This helped to boost performance in the final quarter.

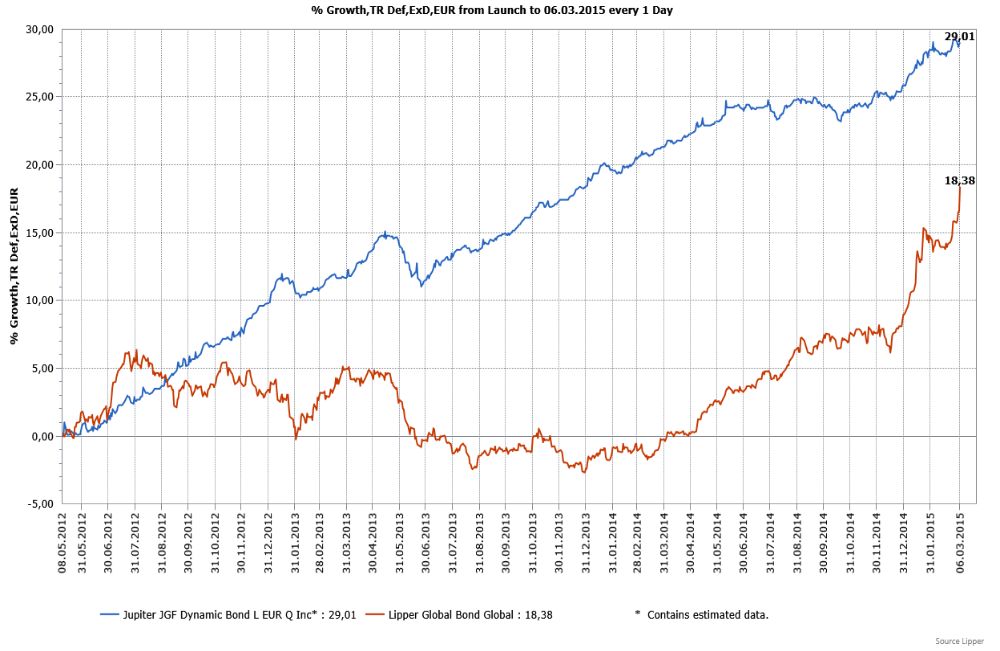

Chart: Jupiter Dynamic Bond SICAV seit Auflage

Zum Vergrößern bitte auf den Chart klicken!

We came into the year expecting relatively modest gains, with coupon payments making up a larger chunk of investment returns. The Fed had started tapering and the US economy was showing increased signs of a self-sustained recovery. We were also concerned that the market was underestimating the pace of recovery in the US economy and therefore the potential pace at which the Federal Reserve might normalize policy. As a result, duration was kept at a low level of 2 years through hedges in 5-year US Treasury bonds and we have adopted strategies aimed at defending the fund against rising US rates (e.g. via yield to call and floating rate notes). Our view proved to be too bullish. The US suffered from a weather-related slowdown in Q1, while a combination of geopolitical and deflationary risks elsewhere in the world meant further Fed tightening might be delayed – a perfect storm in terms of our positioning. We closed out our US Treasury bond short in September and the position proved to be the largest negative contributor to performance during the year.

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.