e-fundresearch.com: European investors are being offered hundreds of different US equity strategies and managers: How do Janus Capital Group’s US equity strategies differentiate themselves in this highly competitive market environment and what characteristics make the Janus equity investing approach unique?

Nick Thompson: The depth of our research and the expertise of our analysts are what really set Janus apart. There are other bottom-up fundamental research firms out there, but few bring the industry-level expertise of our long-tenured analysts. We have more than 30 analysts at Janus, with an average of 15 years of financial industry experience. Our team of health care analysts serves as an example of the level of expertise our analysts bring to their respective industries. Most of our analysts on the team come from scientific backgrounds. We have an analyst with a degree in biochemistry, another analyst with a PhD in immunology and another has a degree in chemistry. This helps our analysts understand more than an individual business, but the science behind much of the innovation taking place within the sector.

I would also argue that the level of research is deeper at Janus. One of our key slogans is that “talking to management is not research.” We continually go the distance to get beyond management teams at a given company. We have a team of research associates who conduct our own proprietary surveys to get a better gauge on consumer habits, or other changing trends within industries. This type of extra research is critical to our insights.

e-fundresearch.com: A growing number of allocators are using passive ETFs for their US equity exposure: How does Janus Capital Group address this issue and by what means does Janus ensure truly active management within its product range?

Nick Thompson: We believe that over time active fundamentally driven stock picking will drive returns in excess of our benchmark and our peers. Our research starts with a list of global companies rather than a specific benchmark. In the US, the years since the end of the credit crisis in 2009 have been dominated by macro-events, multiple expansion, and generally upward trending markets. This environment has created a backdrop where most US benchmarks rank at the top of their peer groups, making a passive strategy look attractive on a relative basis. We believe this dynamic will reverse as company fundamentals begin to drive stock prices again. We look forward to a return to the era of the active manager.

e-fundresearch.com: Looking at current valuation levels and a 6y+ stock market rally: Why should (European) investors still put an increased focus on long-only US equity?

Nick Thompson: One could argue that equities are still not overvalued, even after the six year market rally. This is especially true after the recent selloff. Today’s multiples look reasonable against the backdrop of low rates and low inflation. In periods of sub 2% inflation, P/Es have been just above 19x. Equities also look attractive relative to other asset classes.

e-fundresearch.com: How optimistic is your view into the future and what obstacles and challenges should investors in US equity strategies be prepared to overcome going forward?

Nick Thompson: As we mention above, equities are not overvalued in light of low rates and low inflation. However, we have come out of a period of rapid multiple expansion, and with multiples in line with historical averages, earnings growth is going to be the primary driver of returns going forward. With a stronger dollar and weaker global economy, and companies in the U.S. already taking a number of steps to cut costs and expand operating margins, further earnings growth will be harder to come by. Harder, but not impossible. The challenge will be finding those companies that are poised to grow earnings. We think it’s a challenge where active management, and deep knowledge of specific companies and industries can help.

e-fundresearch.com: Thank You!

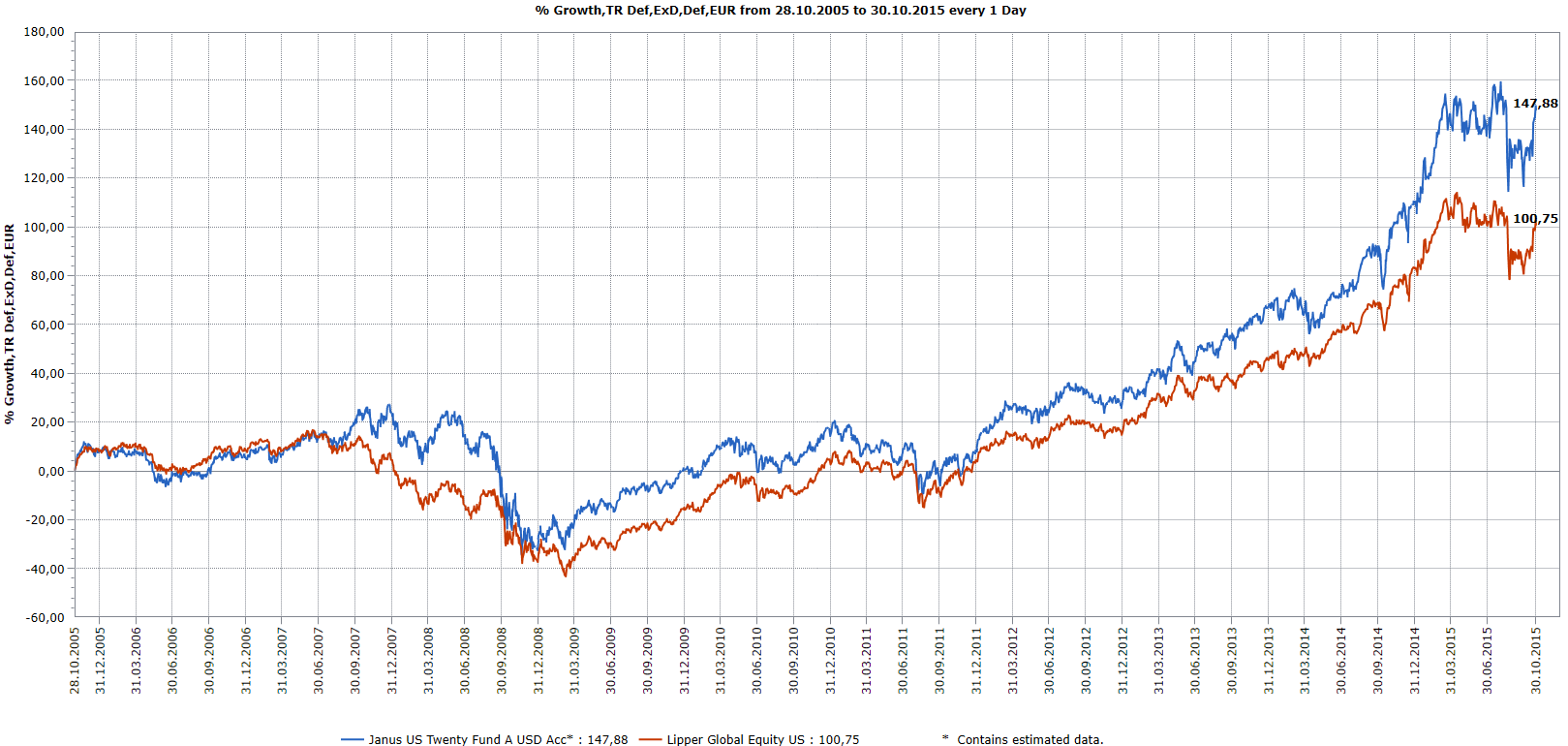

10-Y Chart: Janus US Twenty Fund A USD Acc vs. Peer-Group Average

Weitere beliebte Meldungen:

{kind=link}