[utiIntlLogo]

Content Advertorial

In 2003, the UTI Asset Management Company (UTI AMC) was carved out of the erstwhile UTI and the ownership of the firm was split equally between the four largest State-owned financial institutions: Life Insurance Corporation, State Bank of India, Bank of Baroda and Punjab National Bank. In 2010, the global money manager, T Rowe Price International Ltd, acquired a 26% stake in UTI, diluting the existing four shareholders equally.

UTI AMC presently manages an AUM of 55.16 Billion spread across Public and Private markets in India, as a predominantly Long Only active manager. We do not manage any other country’s assets and strategically have positioned ourselves as an India Specialist firm. Domestically, we run in excess of 200 mutual funds for over 10 million investors. Offshore, we have investment structures in Ireland (UCITS), Mauritius, Cayman Islands, Singapore and Dubai (DIFC). Our global clients include Sovereign Wealth Funds, Pension Funds, Insurance Companies, Asset Managers, Banks and Family Offices.

Given that India is still an Emerging Country, it does not yet form part of most global equity & bond indices (except Global Emerging Markets). Consequently, allocations to India are still considered within the ambit of GEM portfolios. Thus, as a single country EM manager, we are seen as a boutique house. The global landscape for accessing India is peppered with funds managed by most large well-known international fund houses. It is a very competitive space and we play in that zone as a leading domestic Indian manager with local presence and expertise. We believe that the local understanding of a complex market like India gives us a distinctive edge in making investment decisions. Emerging markets in general and India in particular are by definition inefficient markets. Our ability to consistently beat the MSCI India Index in both Up & Down markets is a direct consequence of not just a robust investment & risk management process but a refined understanding of the local investment dynamic.

We were the first to launch an Offshore Indian Equity fund in 1986, pre-dating the establishment of SEBI, India’s capital markets regulator. In the UCITS space, we were the first to launch an Indian fixed Income fund in 2012 and most recently the first to launch a multi asset class India Balanced Fund in 2018.

Essentially UTI has played a pioneering role in development and proliferation of Indian capital markets. In the list of Top 10 Indian asset managers, UTI is the only one that is not a part of a Bank or a Conglomerate, thus eschewing most conflicts of interest that others face.

India – mystical, paradoxical and booming

India has a long unbroken history of evolution, rich and complex, since the days of the Indus Valley civilization. Its contribution to the world of science, mathematics, astronomy, philosophy and medicine is well recognized. In the early 1800s, before the British plundered the country, India represented 25% of global GDP. The India of today is staging an animated comeback with a pro-growth policy agenda and it is on track to become the 2nd largest economy of the world behind China, by 2050. The fact that this booming growth is not fuelled by debt makes India stand out amongst its Emerging market peers.

Economic Growth

At a GDP growth rate of 7.5%, India is the fastest growing large economy of the world today. While it is the 6th largest in nominal terms, on a Purchasing power basis (PPP) it became the 3rd largest in 2016. The growth comes predominantly from Services (51%) while Manufacturing delivers 33% and Agriculture represents 16%. Although agriculture is the smallest segment, it has a direct impact on 60% of the population – the residents of rural and semi-rural India. The bulk of the reform process of the Modi Government is focused on this segment of society.

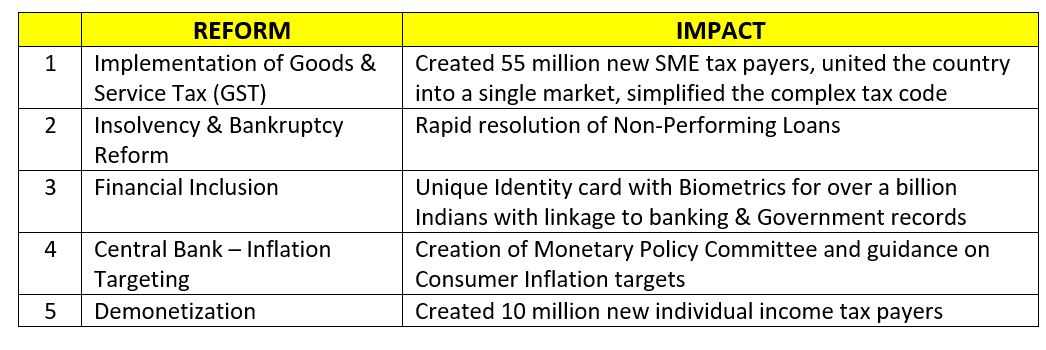

Reforms

Investment Climate & Markets

The market capitalization of Indian equity markets at USD 2.3 Trillion, has kept a healthy pace with the size of the nominal GDP, maintaining a ratio of 95% on average over the past decade. As the country has further opened up to foreign investment an increasing number of companies have listed to seek equity capital. The credit upgrade by Moodys to Baa2 in 2017 and the jump to 100th place in Ease of Doing Business Index has given India greater prominence on the global investment landscape. In the Foreign Direct Investment (FDI) league tables, India is now in the Top 10 countries since 2016 and continues to attract large inflows.

2018 is turning out to be a watershed year for Indian equities. After the global financial crisis, this is the first time that:

- Earning Growth has risen to high single digits.

- Corporate credit is expanding

- Domestic retail investors are investing in domestic equities

- Capacity Utilization is reaching optimal levels

- Pension Fund reforms are creating institutional demand of equities

Despite the upswing in Indian equities this year, the Price Earning multiple at 21 remains at the upper end of the Fair Value band for one year forward earnings. The resurgence in earning growth after a gap of 5 years heralds the beginning of a secular trend that is likely to last 4-5 years.

Our strategies

Our varied investment schemes are designed to suit every need.

Indian Equity: The investment objective is to achieve medium to long-term growth of net assets through investment primarily in growth oriented Indian stocks listed in Mumbai Stock Exchange and National Stock Exchange.

Indian Fixed Income: The investment strategy is to generate total returns with moderate levels of credit risk by investing in a portfolio of fixed income securities issued by the Central Government of India, State Governments of India, Indian Public Sector Undertakings, companies of Indian origin or deriving a significant portion of their business in India.

India Balanced Strategy: To allow investors participation into India’s economy and growth story through risk-adjusted Indian equity exposure, using an active asset allocation strategy, while providing downside protection through income from Indian debt.

For more information please contact us at [email protected] or visit our website.

Weitere beliebte Meldungen:

{kind=link}

{kind=link}