The 60% plus surge in China’s A-share market since late 2014 has raised concerns about a bubble building, especially since the ascent came on the back of an explosion in margin trading and a soaring interest in index futures. The bubble bursting is indeed a risk: borrowing from a broker to buy stocks can accelerate the speed of price ascent, but it can also exacerbate the force of the downswing should anything trigger a price drop.

However, there is no evidence of China’s margin debt growing to a dangerous level that could trigger a market crash. There is also no conviction that China’s stock market has developed into an unsustainable bubble. Academic research has shown that an asset bubble could last for any length of time, ranging from weeks to years. A recent macroeconomic policy shift by Beijing to contain the downside risk of growth could support the market boom for a while longer.

Experience in other stock markets shows that an increase in margin trading is not a reliable leading indicator for stock market crashes. For example, although the explosion in margin trading led to sharp market corrections in the US in 2000 and 2007, there were many other occasions in the past 20 years when a sharp rise in margin trading did not lead to a crash. We do not know, ex ante, whether the level of margin debt has reached a critical level that would lead to a market crash, or whether it is just a market phenomenon along the way to a higher market peak.

In China, more relevant to assessing the chances a market crash due to too much froth is a jump in overall stock market leverage. This often accumulates in invisible ways. Margin debt is just one of them. For example, in the 2005-2007 stock-market boom, leverage built up significantly on the balance sheets of Chinese companies, especially unlisted state-owned enterprises, which collateralised hard assets to borrow from banks and used the proceeds for stock punting. This time around, many players are borrowing through the shadow banking market.

As much as we want to, we just do not know exactly how and where speculative leverage is building and when the red line will be crossed until after the event (market crash). However, putting the recent A-share market boom into perspectives can help to assess the sustainability of the bull-run.

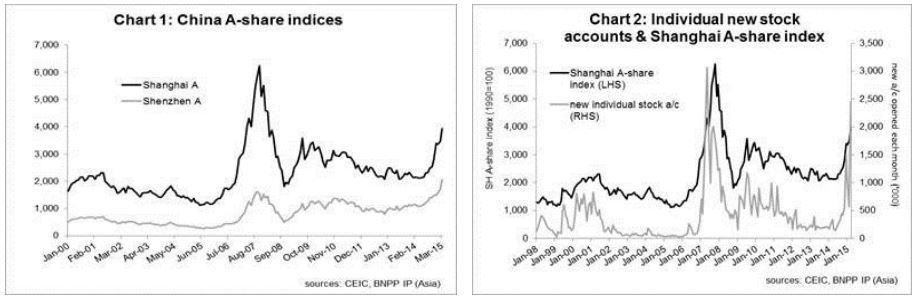

Firstly, both the Shanghai A-share index and the number of new investor accounts opened have only reached levels that are about half their 2007 peak (Chart 1 and 2). The latter not only has a close correlation with the Ashare movement, it also shows that only about half of the potential investible funds have entered the stock market, compared to the last bull cycle (Chart 2).

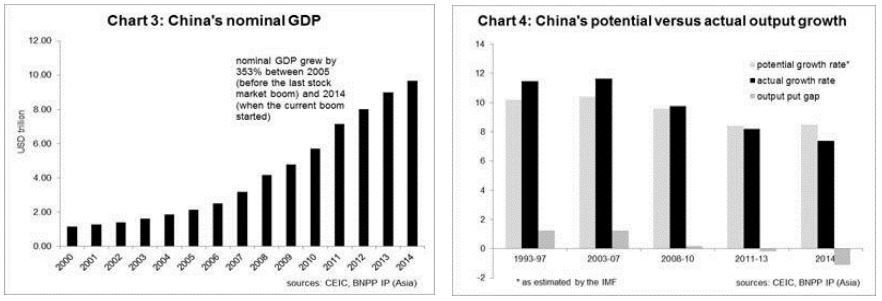

The key fundamental issue affecting the outlook for Chinese stocks rests in the deflationary risk in the system. China’s PPI has been in deflationary territory for more than three years. Nominal GDP contracted in the first quarter of this year with the GDP deflator turning negative for the first time since the US subprime crisis. In fact, China has seen a negative output gap since 2011 (Chart 4).

Arguably, Beijing was slow in realising this, as it focused on deleveraging the economy in 2014. The interest rate cuts since November last year show that it has finally recognised this risk and shifted its policy focus from cutting debt to protecting growth while cutting debt, and from containing inflation to fighting deflation. While the rise in margin trading is a legitimate concern, the change in Beijing’s policy focus is more important in shaping the outlook for stocks. Weak growth and deflation risk will put pressure on Beijing to adopt a policy-easing bias to reduce systemic risk. Stock valuation may be a secondary concern for Beijing at this stage, as it sees a strong stock market as a facilitator for capital market reform by reducing the reliance of corporate funding on banks. This benign policy backdrop plus rising momentum can propel Chinese stocks further through price-multiple expansion.

Chi Lo

Senior Economist, Greater China, BNPP IP