The January 2019 collapse of a Brazilian mine tailings dam—which released 11.7 million cubic meters of toxic mud, killed at least 150 people, and led to a corruption probe—underscores the critical but underappreciated value of environmental, social, and governance (ESG) considerations in emerging markets. In this four-part series, I examine the growing materiality of ESG factors to emerging market investing, exploring both risks and opportunities.

ESG: More Important in Emerging Markets?

The majority of ESG-aware asset managers surveyed by Citi Research in October 2018 expressed the view that ESG factors are more important in emerging markets than developed markets, particularly from a corporate governance risk perspective. (“Sustainability in CEEMEA,” Citi Research, as of 10/29/18.)

Generally, weaker corporate governance practices in emerging markets relative to developed markets have played a role in shaping this opinion. More seasoned, quality-focused investors have long appreciated the need to be sharp on governance considerations when investing in frontier countries such as Kenya and Argentina, as well as the more mainstream countries such as China, India, and Brazil.

Generally, weaker corporate governance practices in emerging markets relative to developed markets have played a role in shaping this opinion. More seasoned, quality-focused investors have long appreciated the need to be sharp on governance considerations when investing in frontier countries such as Kenya and Argentina, as well as the more mainstream countries such as China, India, and Brazil.

Emerging markets have more state-owned enterprises, necessitating a higher level of scrutiny of governance practices by prospective investors. While varying across different countries, there is generally a greater prevalence of family founders with majority stakes within emerging markets. Lower rates of board director independence and weaker corporate transparency are other realities contributing to the elevated governance risk profile.

Beyond these more obvious considerations related to governance and business culture, we've seen a variety of environmental and social issues become increasingly relevant to investors. From an environmental perspective, combating air, soil, and water pollution is becoming a more significant focus of government policy in China and India. And from a social perspective, investors are increasingly scrutinizing how companies are managing broader stakeholder relationships that can materially impact financial performance.

Back to the Brazilian Dam Disaster

The latter point takes us back to the Brazilian dam disaster.

The resource-intensive energy and materials sectors continue to play an important role in the socioeconomic welfare of many emerging and frontier economies, with concomitant ESG risk factors that can have severe consequences beyond share price performance.

For example, mining companies that operate in environmentally sensitive areas where indigenous populations live have to be thoughtful about how they develop resources. They must also ensure the safety of their employees through ongoing capital investments and training.

Brazil's Vale SA, which owns the dam that collapsed in Brumadinho, knows that all too well. The company has since announced that it will close all 10 of its dams in the country with a similar design.

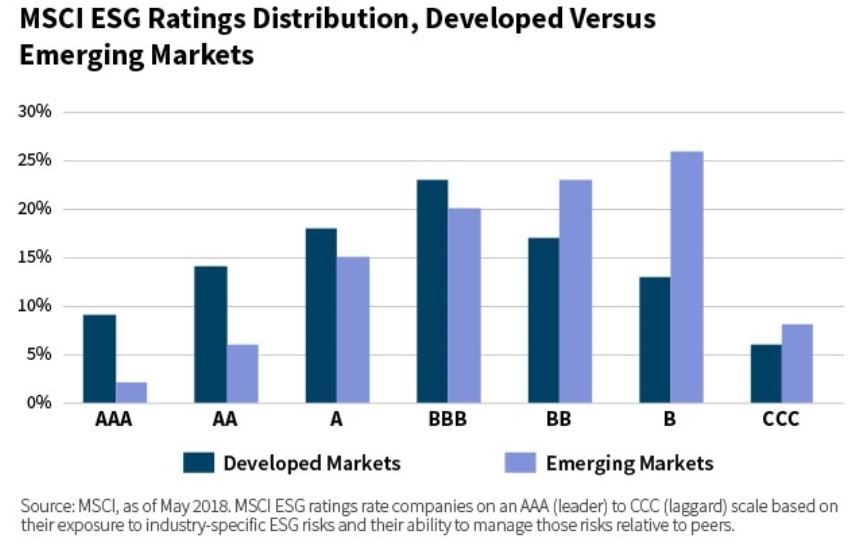

Ratings Reflect Greater Risks, but also Opportunities

These risks can be seen in the ESG ratings distributions of emerging versus developed markets. Conventional ratings distributions, such as the one shown below from MSCI, reflect a negative skew in emerging markets relative to developed markets. (Applying MSCI's ratings methodology, CCC is the lowest ESG rating assigned to companies on an industry-relative basis and AAA is the best.)

This negative skew in ESG ratings reflects some of the risks I discussed above, with a consistent overhang being weaker governance structures for companies across different sectors within emerging markets. Companies lacking a majority independent board, for example, are systematically penalized. The existence of a combined chairman and CEO or dual share classes with unequal voting rights are also detrimental to the rating.

Over time, we expect ESG ratings for emerging market companies to broadly improve as more capital flows into ESG-focused equity and fixed-income strategies, and as more asset managers integrate ESG considerations in traditional strategies.

Growth of ESG Assets in Emerging Markets

We've already seen tremendous growth in ESG-focused emerging markets fund assets, from less than $1 billion in 2008 to $20 billion in 2018, as measured by EPFR and Citi Research. Emerging market ESG funds now account for nearly 10% of global emerging markets funds, up from just 2% a decade ago, as illustrated below.

Asia ex-Japan represents a significant percentage of ESG-focused assets in emerging markets based on data collected by the Global Sustainable Investment Alliance (GSIA), with the largest markets for sustainable investing being Malaysia (30% of total professionally managed assets), Hong Kong (26%), South Korea (14%), and China (14%). (GSIA as of 2016)

Malaysia's prominence may come as a surprise considering the high-profile scandal involving its state-owned investment fund, 1MDB. Similarly, China's inclusion on the list of prominent ESG markets contradicts the conventional perception of weaker governance given the role of state-owned enterprises (SOEs) and environmental mismanagement (ambient air pollution kills hundreds of thousands of citizens every year, according to the Chinese Ministry of Health).

But, perhaps surprisingly, according to a recent biannual review of corporate governance practices in Asia by research firm CLSA, Malaysia was the “biggest mover in 2018,” climbing to 4th place in Asia's corporate governance market ranking.

And China was the fastest-growing market for sustainable investing from 2014 to 2016, according to the GSIA. Sustainable assets there were up 105%, followed closely by India (up 104%).

Much of that growth was driven by investment opportunities arising from public policy initiatives to clean up the environment, including China's efforts to improve air quality by working to transition away from coal toward natural gas and renewables. That's a compelling story that I'll explore further in my upcoming post in this series.

Blake Pontius, CFAPortfolio SpecialistWilliam Blair Investment Management

Tipp: Dieser Beitrag ist auch im "Investment Insights"-Blog von William Blair verfügbar.

Weitere beliebte Meldungen: