We wrote about the pitfalls associated with mainstream approaches to measuring quality, but this is not the only measure of company characteristics that we feel has shortcomings; we experience the same phenomenon with valuation.

Many believe that valuation can be described neatly by the well-established growth or value factors that rank stocks on a metric such as price-to-book (P/B) ratio.

But portfolios that profess similar philosophical beliefs can perform very differently. That raises an important question: Why is there such wide dispersion of performance for funds within a value or growth category?

As they did with quality, William Blair quantitative analysts began addressing the issue several years ago. They recognized that mainstream metrics for defining valuation have serious shortcomings that prevented their acceptance by our team of fundamental analysts and portfolio managers. Our quantitative analysts worked closely with them to identify a better combination of metrics that helps our investment teams identify stocks that better meet our criteria for measuring attractive valuation.

How are our metrics different? In our view, the main shortcoming of mainstream metrics is that they tend to be influenced by accounting distortions that can affect analyses of quality and valuation. The metrics we use to determine valuation instead emphasize cash flow analysis.

Why Does this Problem Arise?

We believe that these problems arise partly because mainstream metrics are so well accepted and used broadly to select stocks in popular style-based portfolios, such as index funds and smart beta strategies. They are commonly used as initial screening tools by active managers that profess a growth or value style of investing.

After underperforming traditional growth stocks for most of the past decade, however, questions have begun to surface as to whether value stocks are best defined by low P/B ratios. Many companies may have valuable intangible assets that are not captured by a traditional book value calculation, and therefore may fall into the growth category despite possessing compelling valuation characteristics when evaluated using cash-flow-driven metrics.

Demonstrating the Problem

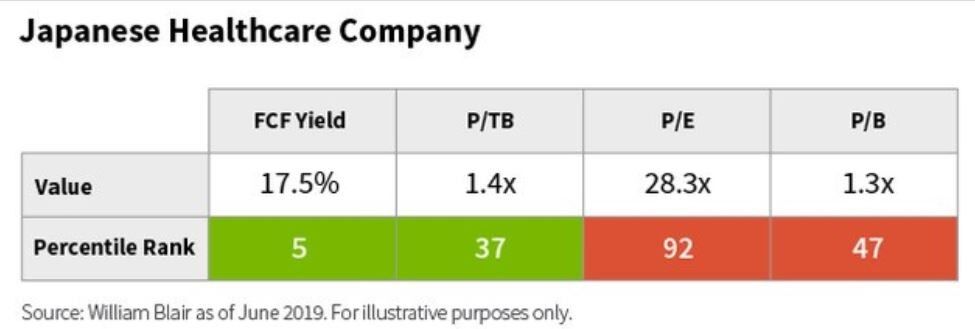

In the table below, we show metrics for a Japanese healthcare company whose stock looked unattractive using price-to-earnings (P/E) ratio and average using P/B ratio. But it has strong valuation attributes based on our own metrics.

The lesson: P/E and P/B ratios may conceal attractive valuations because they can be distorted by the presence of accounting measures such as goodwill and depreciation/amortization.

Metrics that emphasize cash flows and de-emphasize noncash measures paint a better picture of the stock's valuation because the stock's free cash flow (FCF) yield and price-to-tangible-book-value (P/TB) ratio rank attractively.

How Widespread Is This Phenomenon?

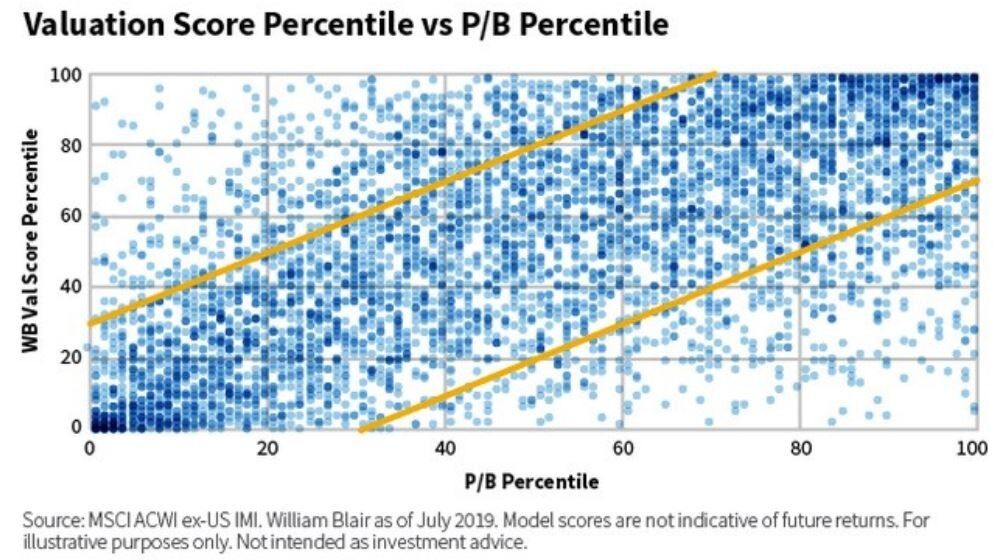

The graph below charts our proprietary approach to measuring valuation against a traditional metric: P/B ratio. The individual points represent individual stocks in the MSCI AC World ex U.S. IMI. We divided this chart into three regions:

- The area between the two blue lines represents stocks where there is relative alignment between our approach to measuring valuation and traditional metrics.

- The area above and left of the top blue line represents stocks that the market perceives as having unattractive valuation using a traditional approach but that our approach identifies as attractively valued.

- The area below and right of the bottom blue line represents stocks that the market perceives as attractively valued but our approach identifies as unattractively valued. We interpret these stocks as value-trap candidates or cheap for a reason.

While most stocks fall within the bands, there are hundreds of stocks where our approach and the traditional metric disagree.

Implications for Active Management

Valuation is an important input to our Systematic team's investment decision-making process, but we believe it needs to be integrated with a stock's fundamentals, the stock's market sentiment, and how combinations of stocks can be integrated into a well-diversified portfolio.

With that said, this analysis offers several important implications for our approach to asset management.

First, there are attractively valued stocks that are underappreciated in the market. These are stocks that might be candidates for portfolio inclusion after considering fundamentals and sentiment.

Second, there are stocks that the market perceives as attractively valued that we identify as weakly valued. Our approach seeks to avoid stocks like these in a wholesale fashion, and we believe this can help improve relative performance over the long term.

Furthermore, we believe the combination of favoring attractively valued stocks and simultaneously striving to avoid weakly valued stocks in a core portfolio helps foster a more consistent performance experience.

Peter Carl

Portfolio Manager

William Blair Investment Managment

Tipp: Dieser Beitrag ist auch im "Investment Insights"-Blog von William Blair verfügbar.

Weitere beliebte Meldungen: