When thinking about technology, asset managers and asset owners have similar concerns and opportunities—both when investing in it and applying it. We must understand that technology is less about technology stocks and more about the way disruption affects corporate performance. And we must address the implications of technology for our businesses. In this two-part series about the power of technological change, I address these topics.

The Technology of Everything

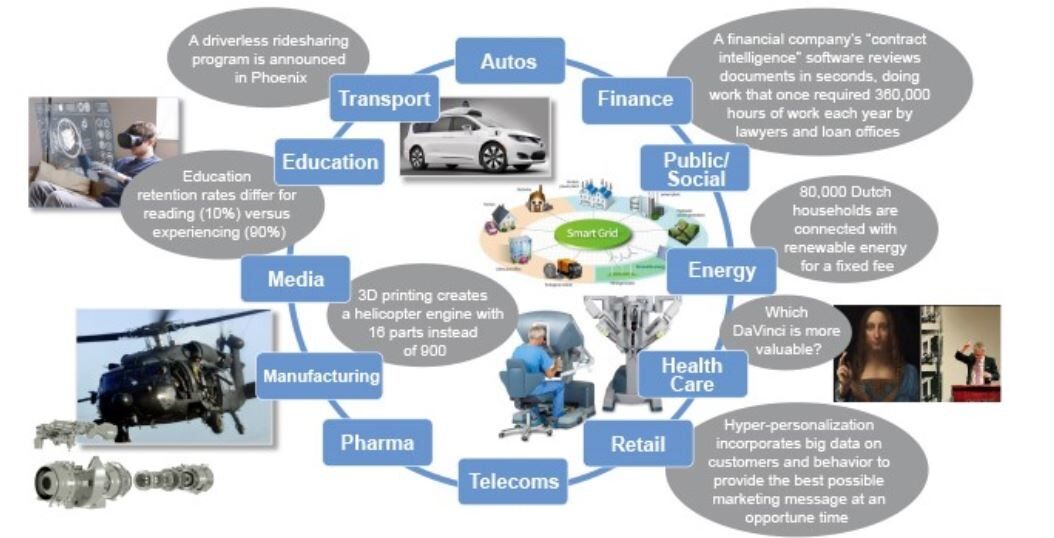

The biggest force to be reckoned with as investors in technology is the technology of everything—increased computing power; artificial intelligence and machine learning; distributed computing through the cloud; ubiquitous data; richer analytics and visualization; and the power of mobility.

These influences have profoundly changed the corporate world. In manufacturing, healthcare, retail, media, and transportation, the level of disruption has never been higher, and it's creating both stresses to incumbents and opportunities for newcomers.

Looking Beyond Technology Stocks

Investing in technology companies to gain technology seems obvious, but is actually less fruitful than you might think and comes with more risk than might be expected.

Based on the Russell 3000 Index returns since 1998, the best-performing technology industry group, software and services, ranks only eighth among all industry groups, behind consumer, healthcare, and industrials.

Other limits to investing in technology include expectations and valuations, which tend to be far too optimistic, leading to challenging stock returns. A shrinking opportunity set—fewer initial public offerings, robust private markets, slowing growth (thanks to regulation, lower capex needs, and abundant capital), and more mergers and acquisitions—are also a challenge.

When we look beyond the technology sector, however, we see better examples of companies that have built lasting, durable, sustainable competitive advantages by being early and/or intentional adopters of technology. Once entrenched, these companies are less likely to be disrupted. Ongoing innovation also becomes a self-fulfilling mindset.

Domino's Pizza illustrates this concept well. Early in its development, the company used technology as a differentiator in all aspects of its business: supply chain, food preparation, delivery, and customer engagement. Now it's a clear leader in an industry that is rapidly accelerating the pace of technology-led innovation. Compare Domino's to another well-known company, Google parent Alphabet. Both went public in 2004, but Google stock is up 2,500%, while Domino's stock is up 4,000%.

In a world of disruption, we find companies like these an appealing place to seek long-term value creation. So we're bullish on technology, especially outside of the technology sector.

Laissez-Faire Governance Creates Risks

Of course, no discussion of technological disruption would be complete without an analysis of the risks, and I'll start in an unusual place: the government.

Historically, the government (including the military) and academia have worked alongside corporations to develop new technologies. The Defense Advanced Research Projects Agency (DARPA) and NASA are good examples.

This has changed. We've seen an erosion of government influence in early-stage research and development as well as a more laissez-faire approach to intervention.

Thus, the private technology industry has amassed considerable power—power perhaps not seen since the turn of the last century, when robber barons in steel, rail, and banking were left to their own devices.

This is particularly clear as it relates to data ownership, privacy, and security. There has been a concentration of power in large platforms, leading to concerns about competition: How exactly can we “undo” Google? Public pressure on this topic will be unrelenting.

“What the government gives, the government takes away.” It's a commonly cited quote, and history tells us it's accurate; we just don't know when it will happen and to what magnitude.

Consider this as a thought experiment, however. If Facebook shut down at midnight tonight, what would actually happen? Ask the same about any company you depend on. What are the odds that seemingly must-have products and services would be replaced very quickly and life would go on?

Societal Disruption Precedes Policy Change

Possibly, however, the biggest risks related to technology are at the existential level—that is, they have little to do with technology itself.

Looking at the role technology plays in society, there are plenty of positives.

Technology enables new solutions, which lead to better and faster offerings for consumers and more efficiency and profits for manufacturers. Virtual reality (VR), for example, could prove to be a powerful force in retraining workers faster than ever. According to the Society for Human Resources Management, programs in which workers use VR headsets for training show productivity gains of 20% to 35%.

Technology also brings jobs. We searched Glassdoor for job openings that didn't exist 10 years ago, and the results included titles such as cloud architect, mobile app manager, and AI engineer.

That said, we have started to see technology take an unexpected toll within the past 10 to 15 years: labor displacement, income inequality, and other social pains.

While much of the movement toward nationalism, protectionism, and tariffs has been blamed on globalization, we believe it results more from disruptions caused by technology.

We are likely seeing the consequences of rapid technological advancements occurring faster than labor skills, regulation, and government policy.

This has occurred before, as technological disruption outpaced society's ability to catch up during the first three industrial revolutions: mechanization and the steam engine, mass production and electricity, and the rise of digital technology and automation.

While government and society have successfully transitioned before, the impacts of our current industrial revolution are being felt more quickly than in the past because change occurs much more rapidly. Angst is high while we wait for policy to catch up to disruption with changes to societal safety nets, including education and training/retraining.

Investment Implications

That sets the backdrop; but what comes next? In my next post in this series, I discuss the implications of technology disruption for active equity asset managers, and by extension their clients as asset allocators.

Ken McAtamney

partner & portfolio manager Global Equity team

William Blair Investment Management

Tipp: Dieser Beitrag ist auch im "Investment Insights"-Blog von William Blair verfügbar.

Weitere beliebte Meldungen: