The rapid rise in the overnight repo rate on September 16 into September 17 harkened back to a John Hughes movie, with the repo trader playing the role of Judd Nelson in The Breakfast Club.

As background, the Federal Open Market Committee (FOMC) cut interest rates by 25 basis points (bps) on September 18. More interesting is the 30-bps cut in the interest rate on excess reserves (IOER), which is the rate the Federal Reserve pays banks for the deposits they hold with the Fed above those required by banking regulations.

Lowering of the IOER was likely the Fed's response to the week's tumult in the short-term (repo) borrowing markets. The tumult was so significant I received more questions about repo funding in the two days leading up to the September 18 Fed meeting than I did in any other market event since the CBOE Volatility Index (VIX) blew up in 2018.

Repo Basics

To level set, repo is short for repurchase. A repo transaction occurs when Party A borrows money on an overnight basis from Party B.

Party As of the world are big Wall Street bond dealers, and this mechanism enables them to fund their bond-market-making operations. The Party Bs of the world are short-term lenders with cash to park, such as money market funds.

So, Party A gives a bond to Party B as collateral. Party A then agrees to buy back the bond the next day at a slightly higher price. The higher price equates to one day's interest on the money that was borrowed the night before. The rate is called the repo rate.

Back to John Hughes

What does that have to do with The Breakfast Club?

When I started working on Wall Street in the early 1990s, a kind soul who had gone to my high school walked me around the trading floor and pointed out the different groups, comparing them to the high school social structure, with all the political correctness of a 1980s John Hughes movie.

He compared long bond traders to the captain of the football team, salespeople as the popular crowd who know where all the parties are, and derivatives traders to members of the computer and math club.

“How about those guys?” I asked. “They look kind of scary.”

“Those guys are the repo traders,” my guide replied. “Stay away from them. They're the trading-floor equivalent of the kids who hung out smoking after cutting gym class.”

You know, Judd Nelson's character in The Breakfast Club. And all those repo traders were like Judd Nelsons of the world when overnight Treasury general collateral repo rates surged on September 16 and the better part of September 17—living in the moment, doing what they do.

A Perfect Storm

This happened as the combination of corporate tax day and a large Treasury coupon settlement prompted significant funding pressures in the repo market.

As a result of the corporate tax deadline—which drains liquidity as corporates sell their money market funds—coupled with the need for primary dealers to fund the many new Treasury bonds being issued by the government, the cost of money got more expensive. The secured overnight funding rate (SOFR) increased 23 bps on September 16—the largest one-day move outside of a quarter-end.

Historically, corporate tax days in September add about $100 billion to the Treasury’s general account and drain a commensurate amount of reserves from the banking system. At the same time, institutional money market funds also tend to experience $30 billion of outflows as corporations draw down their balances to fund their tax payments.

While a swing of this magnitude in reserves is not uncommon, its impact on repo was magnified when $54 billion of Treasury coupons also settled on September 16. More importantly, some of those coupons needed to be financed on dealer balance sheets that were already elevated with Treasury positions.

In response, on September 17 the Federal Reserve Bank of New York announced that it would conduct a system open market operation of up to $75 billion. The operation lends cash to primary dealers, effectively injecting cash in the markets on a short-term basis. When the operation ends, the cash comes out of the market, so the monetary effects of such an operation are strictly temporary.

This was the first such large-scale operation since the financial crisis era, and that may partly explain why the Fed had to temporarily delay the operation.

Ultimately, the operation was undersubscribed, probably because most of the day's overnight borrowing was completed well before the Fed executed. The vast majority of repo transactions occur before 9 a.m. and the Fed operation concluded at 10:10 a.m.

It's interesting that there were varied reactions in other short-term funding markets.

For example, in the market for equity futures rolls, which is basically a market three-month term funding, we didn't see any real movement in implied funding levels.

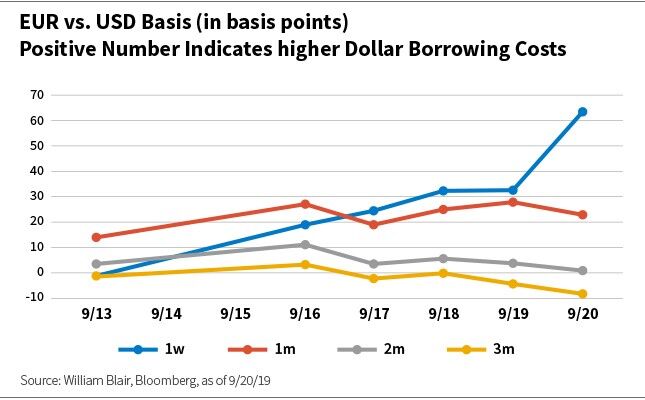

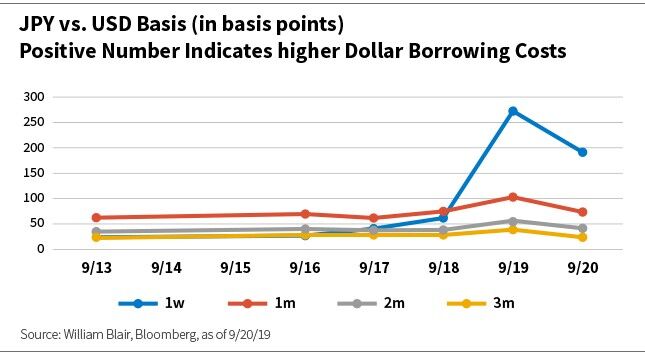

In the foreign exchange market, the short-term demand for dollars drove the one-week basis between U.S. dollars and euros up over 40 bps in two days (consistent with the move in repo), but on a longer-term basis markets did not move materially.

On September 18, the Fed continued its repo facility, with $20 billion additional funding provided on top of $50 billion on September 17.

Observations

A few observations and opinions:

First, I don't think this is a precursor to a repeat of 2008, when the repo market effectively shut down and kicked off the financial crisis.

Second, the market feels like it is calming down, with repo and money-market rates looking a lot closer to where they were on September 13 than where they were on September 18.

But this is still something to watch. The federal funds rate printed above the 2.25% upper level of the target range. Subsequently, it printed back inside the target range, coming in at 1.90%.

At the same time, when you look at other markets, you can get an interesting perspective. For example, check out (see charts below) the spread over LIBOR discounting curves for U.S. dollars vs. euros and the Japanese yen.

Last week, the 1-week spread increased significantly. So, that is alarming and supports the argument that trouble is brewing. But 1-month, 2-month, and 3-month spreads are pretty well behaved. Thus, I believe this seems more like a short-term issue instead of real problems in short-term funding markets.

Steve Karasick is the Head of Derivatives Trading for William Blair Investment Management.

The London Interbank Offered Rate (LIBOR) is the average interest rate estimated by leading banks in London that the average leading bank would be charged if borrowing from other banks. The Secured Overnight Financing Rate (SOFR) is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.

Tipp: Dieser Beitrag ist auch im "Investment Insights"-Blog von William Blair verfügbar.

Weitere beliebte Meldungen: