Reflecting on 2019

We had expected a substantial slowdown in economic growth for the year and consequently positioned for lower rates and wider spreads. While the slowing growth environment and lower rates outlook came to pass, it was notable how resilient risk markets were (albeit coming off the back of a very weak period in the fourth quarter of 2018).

Instead of slowing growth and concerns about recession driving credit spreads wider over the year, we found that dovish central banks, lower rates and the reapplication of quantitative easing (QE) in the US and Europe helped to sustain risk markets and deliver stellar returns across asset classes as investors climbed a wall of worry over Brexit and trade.

In spite of the concerns raised by investors on a perennial basis that central banks are out of ammunition and pushing on a string, it seems that once again it has been the central bankers that have triumphed over economic fundamentals. The question now is where to from here?

We see two major themes likely to shape the financial markets and the global economy in 2020, both of which will contribute to answering the key questions: will there be a recession in the US (or elsewhere) or has the worst passed and, will the longest economic cycle (in US history) continue?

2020: the first key theme is trade…

Can the optimism on a trade détente currently percolating through markets be matched by action from the politicians? We have seen the announcement of a “phase one” deal; will it be signed, can it last and will it lead to a “phase two” or “phase three”? Just as importantly, even with the recent de‑escalation, tariffs remain at extreme levels with only marginal roll back. Will it be enough to prevent any longer lasting damage to global supply chains and investment?

…the second is policy action

We shifted from rate hikes in 2018 to rate cuts and the tentative return of QE in 2019. Have central banks done enough to offset the risks to growth caused by trade disputes and geopolitical concerns and do they have the ammunition to make a difference if the recent optimism is misplaced? The other key policy decision lies with politicians and their choice as to whether to step up the role of fiscal policy in managing the economic cycle.

Rosier outlook ahead

As things currently stand, we see a year of two halves. The first half of 2020 may well be characterised by a continued sluggish growth outlook globally, for the US in particular, as the lagged effects of the trade war and tighter fiscal impulse continue to feed through to the economic data. However, assuming no sudden economic shocks, the second half of 2020 looks rosier, with leading indicators from industry surveys such as the purchasing managers indices (PMIs) (chart 1) and money supply growth suggesting better data to come.

Chart 1: ISM manufacturing lead indicator bottoming?

Source: Janus Henderson Investors, monthly data, as at 31 December 2019

Note: Institute for Supply Management (ISM) manufacturing index versus a lead indicator (new orders minus inventories).

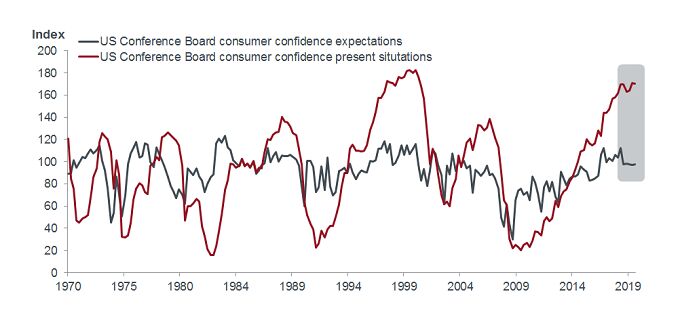

The risks remain to the downside; with a re‑escalation in the trade war a real concern and uncertainties around the US election likely to weigh increasingly heavily on market sentiment as we progress through the year. As an illustration, chart 2 depicts the status of consumer confidence in the US. US consumers’ opinion of the future outlook has rarely diverged so much from their assessment of the present situation. When the two have converged from these levels in the last 40 years, there has always been a recession in the US.

Chart 2: US consumer’s opinion on future outlook at odds with its present assessment

Source: Bloomberg, Janus Henderson Investors, quarterly data, as at 31 December 2019

Equally, while some leading indicators are looking up, it is by no means a clean sweep; much uncertainty remains regarding the strength and durability of the economic cycle in places like the US. However, the risk factors weighing on investors have abated somewhat, with fears of a chaotic hard Brexit reduced following the UK election in December and the “phase one” deal between the US and China a positive development.

Scanning the horizon in search of opportunities

Turning to the financial markets, the biggest challenge facing investors is perhaps not how do I protect capital if the risk case does materialise, but actually where do I invest capital should the benign outcome evolve (as is very possible)? Credit spreads are close to the cycle tights and bond yields remain low, while equity markets make new record highs and already assume a good rebound in corporate profitability in the coming year. Attractive investment opportunities are not the easiest to come by.

We do, however, see interesting opportunities in parts of the emerging markets where inflation‑adjusted interest rates (real yields) remain very attractive in a low growth, low inflation world. We also remain of the view that secured loans and asset‑backed securities (ABS) remain of value to investors but as always a robust and discerning investment process is key to avoiding the inevitable bad apples.

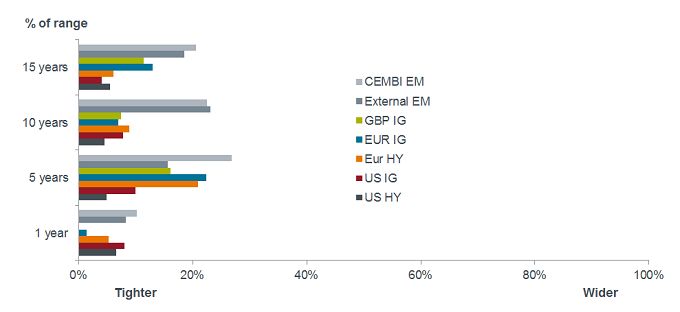

Within developed corporate credit markets we remain generally cautious, with spreads offering little upside from further tightening and the risks still to the downside, while lower quality parts of the credit market continue to signal some distress. Should we see a revision to more attractive levels, possibly on the back of some of the first half economic weakness we anticipate, we would look for opportunities here too. Chart 3 is a good illustration; at the margin, it looks like emerging markets potentially offer value.

Chart 3: spreads as a percentage of their range

Source: Bloomberg, ICE BoA Merrill Lynch indices for high yield and investment grade corporate bonds, JP Morgan emerging market corporate and external debt indices, Janus Henderson Investors, as at 7 January 2020

Note: Spreads as a percentage of their range shows how current credit spreads are situated within their historical range, with a low percentage showing spreads close to their tightest within the given time period and vice versa; HY = high yield, IG = investment grade, CEMBI = Corporate Emerging Markets Bond Index and, External EM = EMBI Global Diversified

Thus, 2020 looks set to be a year of two halves but ultimately our base case is increasingly focusing on a benign outcome. However, we are very wary of downside risks and see markets as increasingly priced to perfection with regards to the base case. Consequently, we retain a cautious approach and will remain selective in our asset class and security selection.

Andrew Mulliner, Portfolio Manager im Global Bonds Team, Janus Henderson Investors

Weitere beliebte Meldungen: