Kernaussagen

- Die aktive Auswahl von Krediten ist weiterhin von entscheidender Bedeutung, da das Thema der Streuung (Dispersion) uns voraussichtlich über das Jahr 2019 hinaus begleiten wird. Auch die Frage des idiosynkratischen Risikos bleibt wahrscheinlich bestehen.

- Das technische Bild erscheint akzeptabel, mit keiner signifikanten Maturity Wall und Aussichten auf ein vernünftiges Potenzial an Kreditemissionen.

- 2020 könnten die Märkte beginnen, Kreditpreise auf der Grundlage von ESG-Faktoren zu differenzieren. Da Janus Henderson ESG-Kriterien seit jeher in seinen Anlageprozess integriert hat, besteht die Möglichkeit, auf diese Weisen eine Outperformance gegenüber dem breiteren Markt zu erzielen

Den vollständigen englischsprachigen Kommentar von Elissa Johnson, Co-Managerin des Secured Loans Fund, und Oliver Bardot, Associate Portfolio Manager innerhalb des Secured Loans Teams bei Janus Henderson Investors, finden Sie nachfolgend eingefügt:

Credit selection remains crucial

As we have said many times in the past, credit selection remains crucial to successful investing in the European secured loans market. We see the main risks in 2020 as similar to those at the start of 2019; namely a turn in the credit cycle, a meaningful economic slowdown, escalating trade wars and, Brexit‑related noise. We therefore continue to position the portfolio towards credits that can weather the uncertainties.

While default rates should remain low, we think a continuation of the dispersion theme evident in 2019 is likely, hence idiosyncratic risk looks set to remain. From a technical perspective, we expect a reasonable balance. Slightly lower collateralised loan obligation (CLO) issuance is forecast due to the tight arbitrage (versus the €29bn seen in 2019) and, with gross loan issuance unlikely to rise aggressively as many refinancings and repricings have already occurred, no significant maturity wall until 2024 and US elections occurring, we see a benign technical backdrop.

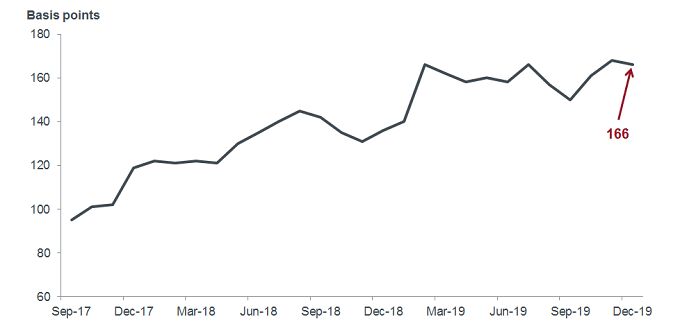

One area that may provide opportunities is the single B rated segment of the market. As macroeconomic uncertainty has picked up in the second half of 2019, the differential between BB and B rated loans has increased. We believe an improving economic backdrop and a pickup in corporate earnings would lead to spread compression between these two rating buckets (chart 1).

Chart 1: spreads on single B versus BB loans at multi‑year wides

Source: Credit Suisse, Janus Henderson Investors, as at 31 December 2019

Encouragingly, we are also seeing issuers provide more information on environmental, social and governance (ESG) factors such as sustainability, climate impact and safety metrics. We believe that in the long run companies that score well on these metrics will deliver better outcomes for credit investors and this is why ESG has always been integrated into our fundamental-based investment process. We think 2020 could be the year that markets start to have the information to really differentiate loan pricing based on ESG factors and this could provide opportunities to outperform the wider market.

A decent year ahead?

Our portfolios have been overweight sterling‑denominated loans versus the broader market for some time now. The loans are typically issued by global and regional businesses and not just by those that rely on the UK economy. These pari passu tranches tend to pay a higher margin versus the euro‑denominated tranches, reflecting lower levels of demand in sterling as CLOs typically purchase euro‑denominated loans.

While sterling loans underperformed their euro and dollar counterparts in 2019 given the uncertainties related to Brexit and UK politics, we see scope in 2020, in the aftermath of the election, for them to recover some of the underperformance seen in 2019.

On the supply side, there is potential for a decent year of loan issuance. Private equity firms have significant dry powder to deploy and publicly‑listed European corporates look cheap relative to their US counterparts. The pipeline for early 2020 looks reasonably healthy, with several large merger and acquisition deals set to approach the market. However, issuance beyond that will depend on a multitude of factors, not least the macroeconomic environment. There will also be competition with the high yield and direct lending markets and issuance will depend on the conditions in each of these markets.

Dispersion to remain

2019 saw a rise in dispersion rates in the European loan market. While not as pronounced as for other sub‑investment grade credit markets in Europe and the US, issuers whose earnings underperformed investor expectations were punished by the market.

According to research from Credit Suisse, as at 31 December 2019, 4.9% of the European loan market traded with a price below 90, the highest level since March 2017, despite the value of CCC rated loans being unchanged over the year. Macro and idiosyncratic risks have both played a part, but more of the latter, in our view. We have also seen examples of significant price rises in loans when a borrower reports an unexpectedly improved outlook.

At this point in the macroeconomic and credit cycle, we believe selectivity remains key to delivering medium-term returns. Our participation rate in new deals fell in 2019 to an average of 38%, mirroring 2018, but far below the average of 50% in the prior three years. However, we now see the opportunity to find selective loans that could offer capital appreciation to the fund, as dispersion rates are likely to continue to rise given the macro outlook and geopolitical uncertainties, despite default rates remaining low. Thus, we expect turnover rates in the fund to move slightly above the 14% seen on average over the last year.

What to watch for

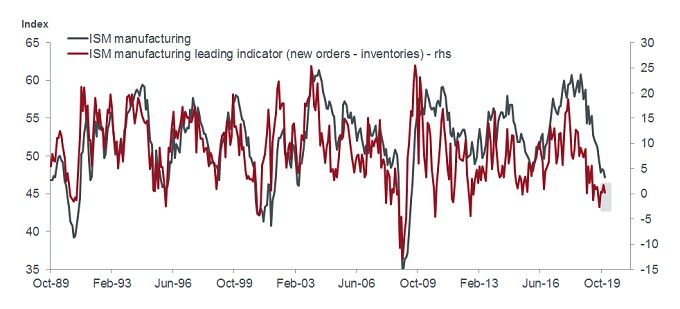

Although our base case is for a ‘slow growth’ environment, we will be keeping a close eye on macroeconomic data releases such as purchasing managers’ indices (PMIs) in 2020. While the share of economies with manufacturing PMIs below 50 has been increasing throughout 2019 — a traditional indicator of a weakening economy — services PMI data has generally remained in positive territory. Chart 2 is an interesting one — seemingly indicating that the manufacturing cycle may be bottoming and supporting our low growth, benign macro base case.

Chart 2: ISM manufacturing lead indicator bottoming?

Source: Bloomberg, Janus Henderson Investors, monthly data, as at 31 December 2019

Coupon‑returns expected

Assuming no major market shocks, we believe European loans could offer potential returns of 3.75-4.25% and 4.50-5.00% (in euro and sterling terms respectively) in 2020; largely in line with coupons after the rally in markets towards the end of 2019.

Technical factors should remain largely balanced, with forecasts of lower CLO supply likely to be matched by slightly lower loan issuance. The macroeconomic picture remains uncertain but our base case is for a continuation of the ‘slow growth’ environment where selective credit investing can earn reasonable risk‑adjusted returns and default rates remain benign.

Weitere beliebte Meldungen: