Equity markets have reached extreme levels of market concentration. This is largely the result of a few mega-cap companies with stellar stock performance. When markets are concentrated, active managers tend to struggle. But it is especially important in these types of markets to continue to seek diversification strategies. Not losing sight of the less dominant sectors, regions, and lower market capitalizations, has proven to pay off in the long run.

The big get bigger

The U.S. equity market has reached its highest level of market concentration since 1970. A few mega-caps, known as the Magnificent 7*, dominate the S&P 500. While concentration is highest in the U.S. market, it is not merely visible in the S&P 500. There is a similar pattern in other major indices such as Europe’s Stoxx 600 and Japan’s TOPIX.

Weight of the top 10 stocks by Market Cap from 1995 to July 2024 in the US (S&P 500) & Europe (STOXX 600), and top-30 in Japan (TOPIX)

Source: Goldman Sachs Global Investment Research, 11 March 2024

Source: Goldman Sachs Global Investment Research, 11 March 2024

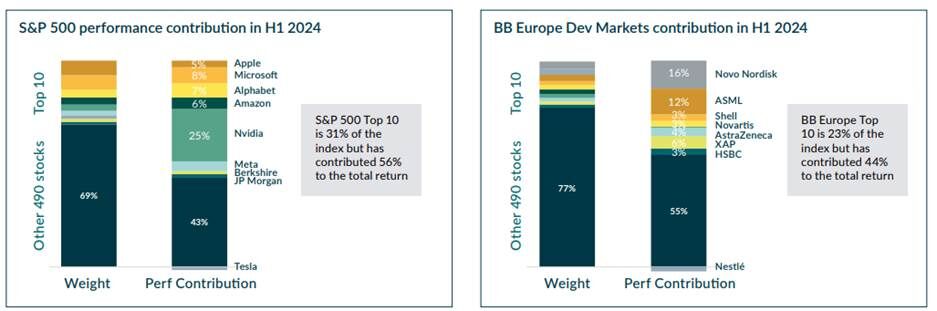

The largest names in the index have generated above-average returns. This has led to ever increasing concentration levels. In the first half of 2024, the top 10 names in the S&P500 represented 31% of the index but contributed 56% to the total return. In Europe the performance was also dominated by the top 10 names.

Source: Bloomberg / Kempen Dividend & Value Team, H1 2024

Past performance is no guarantee to future returns, your capital is at risk

For active managers, it has been a tough period. Concentrated benchmarks are much harder to beat, especially when the heavyweights record stellar returns. As a result of building diversified portfolios, active managers are typically underweighting these mega-caps versus the benchmark. That leads to relative underperformance versus the benchmark and increasing tracking errors.

Time to get active

Although the recent period reflects poorly on active managers, the picture might not continue to be so bleak. Trends in concentration tend to change direction. The track record of mega-caps when they are trading at lofty valuations is poor. Think about the Nifty Fifty or Tech Bubble. History shows that in the long run, the largest stocks underperform versus the rest of the market.

Obviously, it is hard to pinpoint if and when a lasting rotation will happen. That makes it even more important to seek diversification strategies when markets are extremely concentrated.

Source: GMO. Data from 1957-2023. Source: Compustat, Standard & Poors.

Source: GMO. Data from 1957-2023. Source: Compustat, Standard & Poors.

Get to know the less renowned

As dividend and value investors, we are clearly invested in a different kind of company. In short, no or low dividend yields and high valuations, refrain us from investing in many of the biggest companies. Instead, we look for attractively valued companies with strong free cash flows and capital allocation policies.

We have written about our investment philosophy to seek off the beaten path investment opportunities. Our idea generation is flexible, and we look beyond common sectors and regions. Additionally, we also look at mid-sized companies. Due to the increasingly large valuation differential with mega-caps, we find more opportunities with an attractive risk-reward ratio among mid-caps.

Our portfolio construction is based on standard-weight position sizing. These standard weights are not linked to market capitalization. As a result, our funds are well diversified across companies with a range of market capitalizations.

Mega-caps are not invincible

History has shown that investing in mega-cap stocks alone makes your portfolio vulnerable. Given currently extraordinary concentration levels, the same holds for investing in market capitalization weighted indices. Even the largest stocks turn out to be sensitive to gravity eventually.

Recent turbulent summer months clearly showed that investing in mega-caps is not without risk. Growth expectations and valuations have increased significantly over the last 10 years. This is visible when you compare the valuation of the MSCI World, dominated by mega-caps, with the MSCI World Equal Weight.

Source: Bloomberg / Kempen Dividend Team. Period June 2014 - July 2024.

Source: Bloomberg / Kempen Dividend Team. Period June 2014 - July 2024.

We briefly experienced how violent a rotation from a few mega-cap to all those lagging companies can be and how quickly this can happen. With that in mind, it is worth it to keep looking for attractive diversification opportunities.

Do you want to know more? Please visit our website to read more about our dividend strategy.

* Magnificent 7 include Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla

Disclaimers

Van Lanschot Kempen Investment Management NV (VLK Investment Management) is licensed as a manager of various UCITS and AIFs and authorised to provide investment services and as such is subject to supervision by the Netherlands Authority for the Financial Markets. This document is for information purposes only and provides insufficient information for an investment decision. No part of this document may be used without prior permission from VLK Investment Management. This document does not contain investment advice, no investment recommendation, no research, or an invitation to buy or sell any financial instruments, and should not be interpreted as such. The opinions expressed in this document are our opinions and views as of such date only. These may be subject to change at any given time, without prior notice.

Capital at risk. The value of investments and the income from them can fall as well as rise, and investors may not get back the amount originally invested. Past performance provides no guarantee for the future.

General risks to take into account when investing in Dividend equity strategies

Please note that all investments are subject to market fluctuations. Investing in a Dividend Equity strategy may be subject to country risk and equity market risks, which could negatively affect the performance. Under unusual market conditions the specific risks can increase significantly. Potential Investors should be aware that changes in the actual and perceived fundamentals of a company may result in changes for the market value of the shares of such company.

Weitere beliebte Meldungen: