Investment Universe, Process, Strategy and Benchmark – How does the Fund Manager invest?

The fund´s investment objective is to offer pure, adaptable and optimised exposure to fluctuations in the 1-year implied volatility of the Euro-zone’s equity markets. Volatility, traditionally considered as a risk indicator, is used here as a source of performance: the investment team exploits its medium-term cyclical trends and short term fluctuations.

The investment goals of the fund (ISIN: LU0272941971) are:

- Absolute performance

The investment goal of the fund is to provide absolute performance by offering exposure to equity market volatility of the Euro zone on a 3-year investment horizon and within a controlled and budgeted risk.

This investment solution aims to achieve, over the medium term, a performance objective of 7% gross per annum before fees, whatever the main market trends (equity markets, bond markets, etc.). - Maximum VaR of 35%

The volatility measures the dispersion of the returns around its average. Therefore, a precise risk control of the portfolio is carried out through Value at Risk. The risk budget defined by the team consists of a maximum ex-ante annual VaR of 35%. This means the portfolio is constructed in such a way that statistically, under normal market conditions, i.e. with a probability of 95%, the net asset value of the portfolio should not drop of more than 35% over a year.

Philosophy

The philosophy behind the fund is that:

- Equity volatility eventually reverts towards its long-term average, around 25%. The approach is one of active management around a mean reverting strategy: the fund takes advantage of low volatility regime to be long volatility, but also benefits from a high volatility environment by selling volatility.

- Performance of this long-term trend is supplemented by a mechanism to exploit short-term fluctuations in volatility.

So, fluctuations in volatility of the Euro zone equity markets represent an original source of performance.

Amundi Funds Absolute Volatility Euro Equities invests in pure volatility. Traditionally considered as a risk indicator, volatility combines all the characteristics of an asset class of its own:

- Accessibility: it is possible to invest in the equity volatility of the Euro zone and of other zones via listed options and derivatives. The price of the different options varies according to implied volatility, which reflects the risk expected by investors.

- Uncorrelated behaviour compared with trends in returns of the equity asset class and credit spreads. This can also become a reverse correlation in times of crises. As a rule, a rise in equity volatility is related to a correction of the equity markets or a widening of credit spreads.

- Performance: introducing this asset class to an equity or balanced portfolio makes possible to reduce its overall risk while increasing its expected return, notably at times of low volatility.

Our investment universe consists of the following instruments:

- Listed derivative instruments, mainly on Eurostoxx 50 and equity indices of the Euro zone:

- futures

- options

- futures on interest rates for hedging purposes - Money market instruments: Certificates of Deposit, commercial paper, repos, short term government treasury bills.

- Interest rate swaps: EONIA OIS (Overnight index swaps) in order to hedge the interest rate exposure on money market instruments.(from fixed to variable rate)

- Money-market funds: for cash management purposes, we may also invest in Amundi internal money-market open-ended funds.

As the strategy is based on a balance between a quantitative approach (the grid) and discretionary judgement (leeway), changes in the exposure to volatility are driven by movements in implied volatility across the grid. However, the fund is not purely systematic and the fund manager has flexibility thanks to the leeway of +/- 1: a good level of discretion to vary exposure around the grid, but also in the range [25-30], based on his qualitative assessment of the market. The grid is the “core” position of the fund, while the leeway represents the flexibility to express short term views. The judgment of the fund manager is a key factor in the creation and the adjustment of the fund’s exposure to volatility.

As an absolute return fund, Amundi Funds Absolute Volatility Euro Equities has no benchmark.

Performance Review 2006

Gilbert Keskin & Eric Hermitte: "The fund was incepted on 15th November 2006. From this date until the end of 2006 the fund was up +2.61% (C(C) share class). This was a period where the fund was positioned long volatility with an average vega of around +2. 1-year implied volatility of the DJ Eurostoxx50 increased from 15.30% to 16.65% allowing the fund to record gains due to its long volatility positioning. Additionally, the fund was managed to benefit from the small fluctuations in volatility of volatility over this period. In terms of gross performance contribution: the directional engine contributed 2.63% while the volatility of volatility contributed 0.15%."

Performance Review 2007

Gilbert Keskin & Eric Hermitte: "In 2007 the fund recorded a performance of +5.64% (C(C) share class). The beginning of the year from January to May 2007 was a difficult period as the fund was positioned long volatility with an average vega of around +2 while 1-year implied volatility of the DJ Eurostoxx50 remained low and stable around 16%. During the second half of the year, the fund benefitted from two spikes in volatility from 16% to 22% (June-August) and again from 19% to 22% (September-November) while the fund was positioned long volatility with an average vega of around +1.4. Vega of the fund was reduced from +2% at the beginning of the year to +1.1 by year end when volatility rose to levels of 20%. In terms of gross performance contribution: the directional engine contributed 6.91% while the volatility of volatility was negative -0.14%."

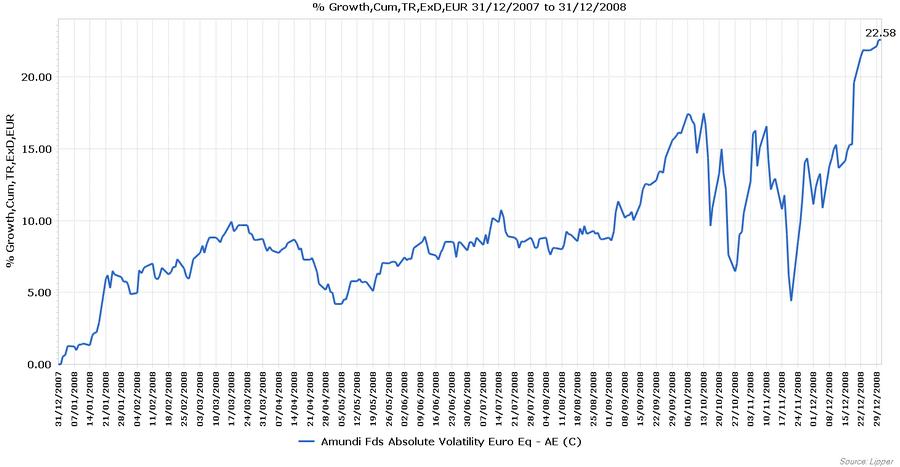

Performance Review 2008

Gilbert Keskin & Eric Hermitte: "In 2008 the fund recorded a performance of 22.58% (C(C) share class), its best year of performance since inception. This was due to the unusual circumstances that led to the eventual bankruptcy of Lehman and the global financial crisis. Since the fund was positioned long volatility with an average vega of +1 going into the crisis, the fund was able to benefit from the spike in volatility from 20% to 30% from January to September 2008. The fund reversed to a short volatility position (negative vega) once 1-year implied volatility of the DJ EuroStoxx50 spiked above 30%. The fund suffered a drawdown of approximately 11% from October 13th to November 21st as 1-year implied volatility spiked to 47%, before recovering the drawdown in just 28 days thanks to the huge fluctuations in volatility of volatility over that time. In November and December 2008 the fund recorded one of its best monthly performances due to its short volatility positioning while volatility subsided from 47% back down to 35% by year-end; and due to the volatility of volatility, which was very active towards the end of the year. In terms of gross performance contribution: the directional engine contributed +5.70% while the volatility of volatility contributed +18.54%."

Performance Review 2009

Gilbert Keskin & Eric Hermitte: "In 2009 the fund recorded a performance of 5.76% (C(C) share class). During the first 3 months, the fund recorded a slightly negative performance due to its short volatility positioning while 1-year implied volatility stayed relatively stable at around 37%. From April to July, however, 1-year implied volatility decreased from 37% to 26%, which allowed the fund to record strong gains due to its short volatility positioning. In July 2009, the fund reversed its positioning and became long volatility. From July until the end of the year the fund recorded a flat to slightly negative performance due to its long volatility positioning while 1-year implied volatility declined slightly from 26% to 24%. In terms of gross performance contribution: the directional engine contributed +1.13% while the volatility of volatility contributed +6.07%."

Performance Review 2010

Gilbert Keskin & Eric Hermitte: "In 2010 year-to-date through September 30th, the fund recorded a performance of +7.53% (C(C) share class). The first three months resulted in flat to negative performance due to a long volatility positioning with an average vega of +0.75 while 1-year implied volatility of the DJ EuroStoxx50 declined from 24% to 22%. Then in end-April and all throughout May, the fund recorded strong performance due to several spikes in volatility from 22% to above 30% due to the Greek sovereign debt crisis spreading to the peripheral Euro zone. From June to September the fund recorded smaller gains in performance thanks to opportunistic trading of volatility, as 1-year implied volatility remained range-bound. In terms of gross performance contribution: the directional engine contributed +2.11% year-to-date while the volatility of volatility contributed +6.86% year-to-date."

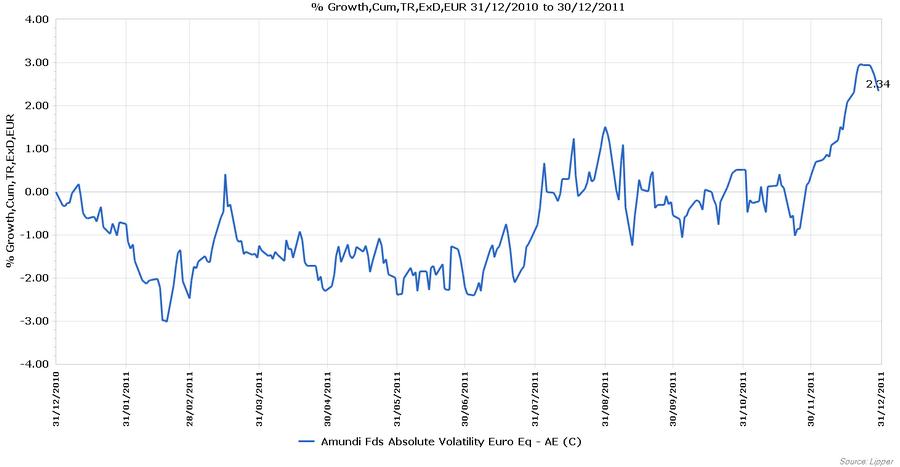

Performance Review 2011

Gilbert Keskin & Eric Hermitte: "2011 was characterized by another year of market volatility in equities. Our measure of the 1yr Implied volatility on the EuroStoxx50 started the year at 24%, reached a low at 20.6% late April, saw a peak of 34.5% in early October, to finish the year at 28%

The volatility environment in 2011 was split in two distinctive periods. From January to end of July, it was overall a declining volatility trend, with the exception being the volatility surrounding the earthquake in Japan. The AAA downgrade of the US debt and the sudden loss of confidence on Italian and Spanish debt markets caused a significant reversal of volatility, which spiked strongly in a similar fashion to 2010 and remained volatile until year end with a debut of normalization.

In this context, Amundi Funds Absolute Volatility Euro Equities was positioned long volatility in the first half. Its long exposure stood at a maximum of +1.15% in February. Volatility trended up slightly around the Middle East unrest, and spiked briefly following the Fukushima nuclear plant accident. However volatility was stable and Q1 ended with a 1.05% loss. Q2 was more challenging, as we remained long volatility and had to fight time decay. H1 overall was down less than 2%.

The long volatility position of the fund of +0.7% was not so aggressive before the very much unexpected spike late July. Although we did benefit from this spike, we unwound our long volatility a bit early late August. Q3 delivered a respectable +1.93%

As volatility started to reach expensive levels similar to 2010, the fund reversed its position in line with its investment philosophy of active management, and turned short volatility. The trading engine – volatility of volatility – was particularly effective. The last 3 months of 2011 were all positive, trading in and out of volatility from the short side. Q4 returned a strong +3.08%, showing our ability also to generate positive returns in highly volatile market, and benefiting from volatility normalization. For 2011 the fund returned +3.15%."

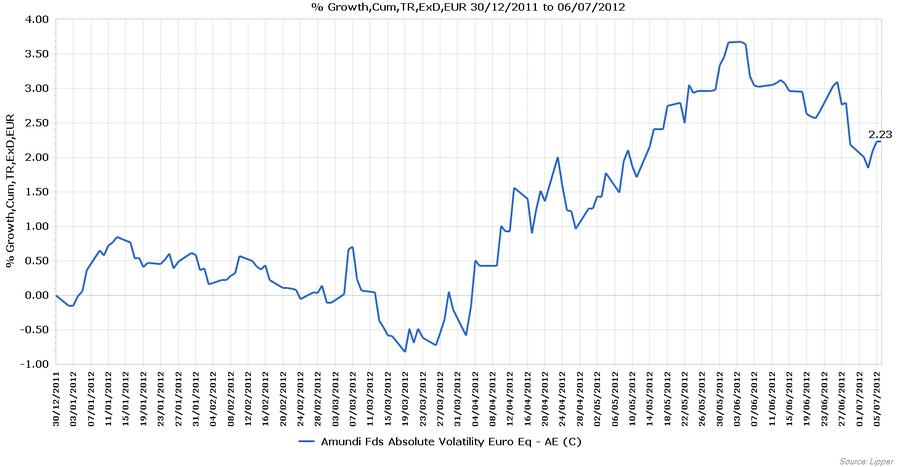

Performance Review 2012 - Year-to-Date

Gilbert Keskin & Eric Hermitte: "The year 2012 started with a level of implied 1 year volatility roughly 28% and declined to close to 22%. In the first days of the year the fund was short volatility leading to a good performance of the fund while volatility was falling. Mid January the fund turned long volatility as volatility continued to fall and got below 25%, the volatility mean we defined for this strategy. Since then the position was build up carefully with falling volatility but the management took in between the opportunity to cut the position when volatility was rising in order to capture performance from the volatility of volatility. Overall we have a slight negative contribution from the directional engine as volatility was falling while having a long vega position. This negative contribution was partly offset by capturing volatility of volatility leaving the fund with a negative performance YTD of -0.38%. Unfortunately the markets were quite stable in the first quarter with little movement in the volatility leaving only limited space for the strategy to capture performance from the volatility of volatility, which is usually the strongest source of performance."

Performance since 2007

Gilbert Keskin & Eric Hermitte: "Looking at the performance since inception of the fund you can notice a stable continuous positive performance over time. The fund proved that the concept is working out well and that the fund managers are able to capture extra performance compared to the model by implementing active management. You can also see that volatility of volatility tends to be the predominant performance contributor to the fund.

In 2007 as volatility was creeping slowly up coming from very low levels at about 15% above the 20% mark the fund performed well due to the directional engine. 2008 till 2010 the fund performed excellent with 2008 being an exceptional year. In these years the performance was driven by the volatility of volatility and the managers showed their ability to take the right decisions in terms of positioning the fund and managing the vega levels. Especially in times of growing market uncertainties and crisis the fund proved to be an excellent investment as it delivers positive performance with own volatility of roughly half the one of the Euro Stoxx 50.

2011 was so far the weakest year of the fund with a performance of 3,15% which is due to the relative stable market situation in the first half of the year. The second half the crisis came back and particularly in August the management team was surprised by the markets not having been aggressive enough with its vega position.

Since inception the fund returned till end of March 2012 58.93% while being every year positive in performance."

Weitere beliebte Meldungen:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}