e-fundresearch.com: What are the main steps in your investment process and in which area is your competitive edge to add value to investors?

Thierry Larose: There are two main parts of the investment process: the SRI screening (normative as well as best-in-class) and the portfolio management.

The investment universe of the strategy consists of the following types of instruments, taking into account that the start universe consists of 89 countries;

- Fixed-income securities (including inflation-linked, zero-coupon and floating-rate notes) and, to a lesser extent, credit-linked notes and derivatives

- Issued or guaranteed by local and national governments, semi-government, agencies from emerging countries

- Issued by supranational institutions (World Bank, EBRD, IADB, etc.) and denominated in a local currency of an emerging country are also.

- Issued by regulated financial institutions in the case of credit-linked notes

Based on the experience of the in-house sustainable screening of OECD countries, which has been used for eight years for Petercam L Bonds Government Sustainable, the retained criteria need to fulfil three requirements to be valid:

- variables that can be influenced by a country

- numeric and comparable data for all countries

- data available from reliable sources.

The approach is best-in-class i.e. focusing on the historical performance between peers within the different criteria. Each criterion gets a score between 0 and 100, (best is 100, worst is 0) based on its relative position compared to other countries (comparison to the difference between the maximum and the minimum).

For binary criteria (protocols or conventions for example) it is 0 (no) or 100 (yes). The final and overall score of a country (on 100) is equal to the weighted average of the scores on each criterion, using the weights which are decided by the Fixed Income SRI Advisory Board (FISAB).

The selection process results in an initial ranking of 89 countries.

Normative SRI screening

Based on an annual survey regarding political rights and civil liberties, Freedom House ranks worldwide countries in three main groups:

- A Free country is one where there is open political competition, a climate of respect for civil liberties, significant independent civic life, and independent media.

- A Partly Free country is one in which there is limited respect for political rights and civil liberties. Partly Free states frequently suffer from an environment of corruption, weak rule of law, ethnic and religious strife, and a political landscape in which a single party enjoys dominance despite a certain degree of pluralism.

- A Not Free country is one where basic political rights are absent, and basic civil liberties are widely and systematically denied.

The normative screening consists of excluding all countries ranked as ‘not free’ and whose status is confirmed by a second source, namely The Economist, ranking them as ‘authoritarian’ countries. Given the impact of this normative screening on the eligible universe, similar indicators have been analysed to legitimate the choice of Freedom House.

The Freedom House index is based on an annual survey of 25 questions to individuals. Political rights are based on the electoral process (1), political pluralism & participation (2), and the functioning of government. Civil liberties are based on freedom of expression and belief (1), personal autonomy & individual rights (2), associational & organisational rights (3) and rule of law.

The main comparable indicator is the democracy index provided by The Economist. The democracy index is the result of 60 indicators grouped under five themes, quite similar to those studied by Freedom House:

- electoral process and pluralism

- civil liberties

- functioning of government

- political participation

- political culture.

The ranking is divided into four categories: full democracy, flawed democracy, hybrid regime and authoritarian regimes.

24 countries are currently not allowed for investment.

Combining the normative and best-in-class SRI screening results in the eligible universe

The investable universe is defined according to the sustainability level in the ranking. Indeed, depending on the ranking, the portfolio management team is allowed to invest a certain percentage in the remaining countries. The FISAB formally approves the ranking of the countries.

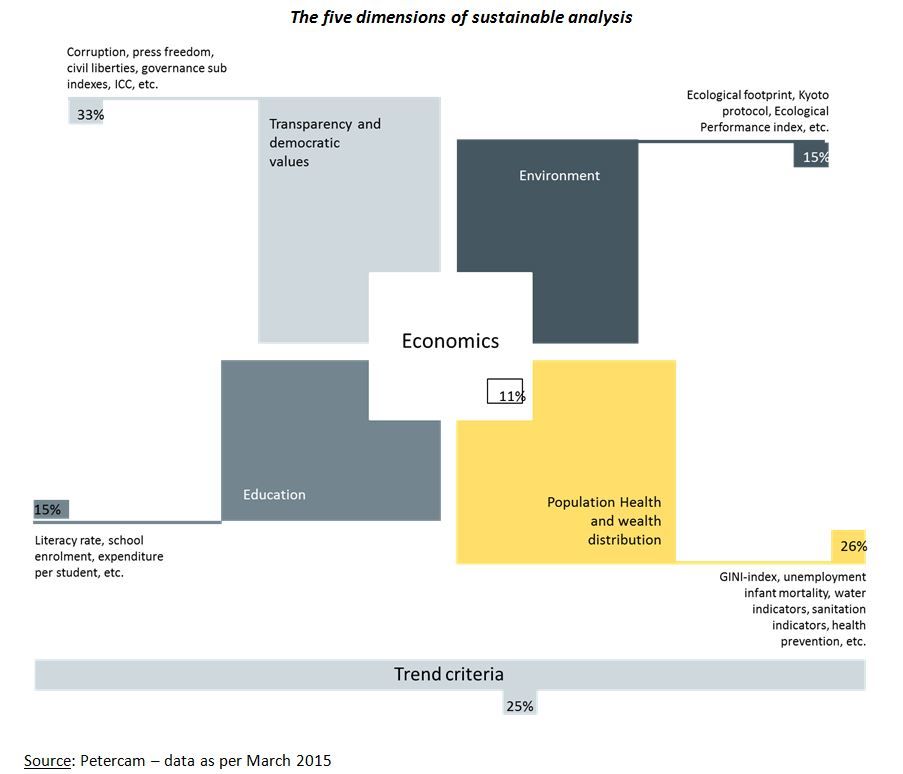

The criteria to rank the countries refer to five sustainability dimensions:

- Transparency and democratic values (weight: 33% of total score, excluding trend criteria)

- Environment (weight: 15%)

- Education (weight: 15%)

- Healthcare and wealth distribution (weight: 26%)

- Economics (weight 11%)

The trend criteria (25%) aim at assessing the dynamism of a country within each pillar.

The final and overall score of a country (on 100) is equal to the weighted average of the scores on each criterion, using the weights which are decided by the Fixed Income SRI Advisory Board.

The calculation methodology of the five dimension is visualised below.

In view of the ranking, there is a direct link between the wealth of a country and its sustainability level. Nevertheless, it is difficult to clearly distinguish the cause and the consequence. Furthermore, several agree that sustainability criteria cannot be as severe as they are in a more economically developed region (OECD for example). Finally, it makes sense to combine a best in class approach, awarding the countries which are more advanced in terms of democracy and civil liberties, with a best effort approach to encourage the not leaders but who try to improve the situation with their means at their disposal.

Therefore, with the exceptions of the not-free countries, confirmed as authoritarian regimes, the investment team is allowed to invest in the whole scope of the universe. But the investments are limited depending on the sustainable ranking:

- Min. 40% of the total portfolio in the top quartile of the ranking

- Max. 50% of the total portfolio in the 2nd & 3rd quartiles of the ranking

- Max. 10% of the total portfolio in the bottom quartile of the ranking.

The outcome is shown in the table below.

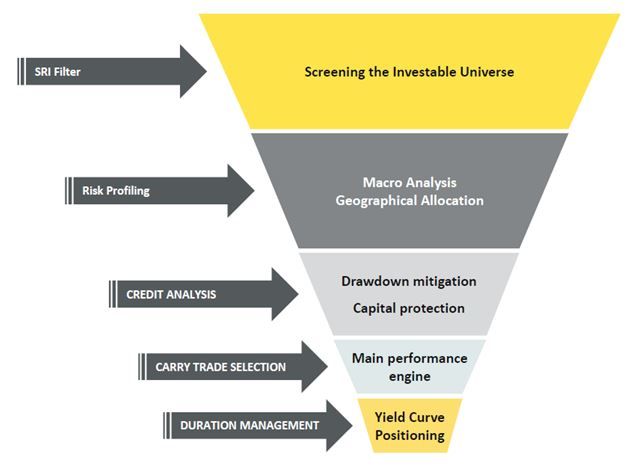

The portfolio manager aims to assess global liquidity on financial markets and positions the portfolio in function of his findings, either in a defensive or a dynamic way. Primarily, cross-asset correlations as well as volatility indicators are used to this goal. This assessment directly impacts the average credit quality of the portfolio, the allocation between advanced developing and frontier countries as well as the size of the cash buffer.

Top-down selection

Petercam top-down macro analysis serves primarily to assess the stage of the economic and credit cycles of each region (e.g. Central Asia, South-East Asia, Central & Eastern Europe, Latin America, Middle East & North Africa, Sub-Saharan Africa) and to decide on the regional allocation accordingly. In this phase of the investment process, Petercam analyses the macro-dynamics driving each region and their anecdotal and forward-looking impacts on the structure of the Balances-of-Payments aggregated at a regional level . This research is conducted both by the macro analyst team, as well as by the portfolio managers. The result of this phase of the process will be to determine which regions will be over-weight, under-weight or simply avoided.

Bottom-up security selection

The purpose of this phase is to select the most attractive issuers and currencies in each region.

Currency management is an important performance driver of the process..

Credit selection is an essential element too in this phase. Both sub-processes will be performed through a multi-angle approach including:

- Fundamental analysis of domestic economic indicators: growth, inflation, credit demand, external accounts, fiscal balance, public and private debt, etc.

- Analysis of political stability and of the willingness and the ability of the government to conduct reforms

- Analysis of monetary policy and of the track-record of the Central Bank

- Analysis of implied and realized forex volatilities, and correlations with other currencies and asset classes

- Analysis of credit spreads in order to gauge how the credit risk is rewarded versus peer countries and versus historical credit performance

- Analysis of the market in each country: stage of development of domestic and external debt markets, liquidity, foreign positioning, governing laws, etc.

Optimization

This phase of the investment process will determine the optimal stance towards duration in each country, hence the yield curve positioning.

Typically, the more advanced an emerging market is, the more correlated are its long-term rates to those of developed economies. In these countries, the managers will set the duration in accordance with their opinion on the trend of long-term yields in US and western Europe core markets.

At the other end of the development spectrum, the more frontier markets will be more immune to the situation in developed markets and will be more driven by domestic factors and/or global liquidity. In those countries, the managers will set the duration on a case-by-case basis, based on their views about domestic monetary policy and the foreign positioning developments.

Weitere beliebte Meldungen: