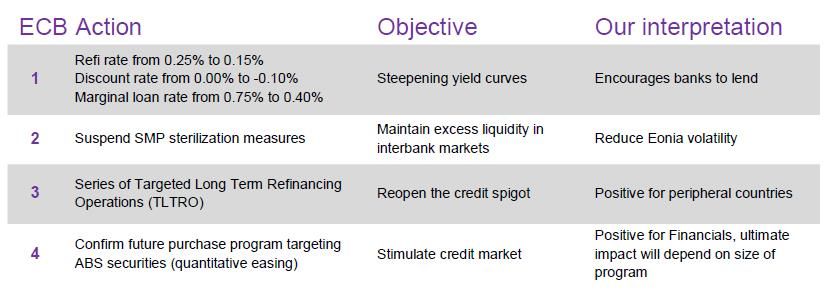

In a historic move, the European Central Bank on June 5, 2014 cut interest rates and confirmed it would embark on a broad range of measures aimed at stimulating the Euro-zone economy via four principal actions:

What does the recent ECB announcement imply for interest rate strategies?

Over the past few months, Natixis AM’s interest rate forecasts have pointed to lower rates and lower spreads, despite the fact that consensus data and market sentiment maintained persistent expectations for higher rates, linked more to higher US rate expectations. Lower rates and spreads have been built into our central scenario, and our in-house model recently pointed to 1.32% as fair value for the 10 year German Bund, a level which the market subsequently reached in recent weeks. Throughout this period, our interest rate strategies have privileged neutral to long durations, a view that has been rewarded since the start of the year but which has only recently gained traction in the market place. Indeed, leading up to the ECB announcement, we have observed a decisive shift in investor positioning to long duration; the last time this kind of market reversal happened was in 2012.

However, contrary to broader market positioning, we remain more defensive than the consensus and prefer a neutral duration posture, because our reading of the BCE announcement implies bearish risk for bonds as well. Our interpretation is that the ECB has sent a strong statement to investors that they will do “whatever it takes” to extract the Euro-zone from anemic inflation or deflation in certain countries. The effect on ten-year yields should send them back into the lower end of our 2014 target range of 1.50%-2.25% for the 10-year German Bund. As such, this combination of an extremely bullish market on the back of ECB messages represents an opportunity to reduce duration exposure in our portfolios as rates should drift higher into the above range. Toward the end of 2014, we could touch the higher end of this range as US yields should reflect anticipations for 2015 FOMC tightening.

Perhaps the most beneficial measure is the four-year, EUR 400 billion Targeted Long Term Refinancing Operation (TLTRO) to be implemented in September and December 2014. This move targets in particular the real economy but should benefit peripheral European countries such as Spain and Italy, where we already hold strong overweights. We thus maintain these positions in both countries.

For strategies invested in credit sectors, the Quantitative Easing program, announced to purchase ABS, should benefit the entire sector. Natixis AM’s aggregate and credit strategies are already overweight Financials, and confirmation of the “QE” program could lead to an increased risk budget allocation to diversifying credits such as convertibles and high yield.

Inflation

Finally, the implications for inflation-linked strategies are positive as well. The ECB has in effect revised inflation expectations downward to 0.7% for 2014 and 1.1% for 2015, and suspended the sterilization program which it had been unable to implement fully. The TLTRO program will provide support for inflation-linked bonds. Given these factors, current market inflation expectations of 0.8% for three years and 1.45% for ten years are attractive in our view and justify a continued overweight or off-benchmark allocation to inflation-linked bonds in our government and aggregate portfolios.

What does this mean for money market yields?

In the wake of ever-lower anticipations for Eonia rates, the question remains “how low will we go?” However, negative money market yields are not necessarily the logical next step.

Credit spreads should remain stable for funds with the ability to invest across short-term credit sectors and extend weighted average maturity, although we expect some compression as yields decline. As such, the shortest-maturity overnight money market funds, whose yields are close to or flat with Eonia, could indeed see significant compression.

Natixis AM’s money market funds have already been positioned defensively in anticipation of yesterday’s moves. In short term money market funds, two strategies are already in place in order to maintain

a defensive positioning: first, extending maturities several weeks out the money market curve, and second, continuously managing the allocation between fixed and floating rates. For example, short term money market funds currently hold 50/50 allocations to fixed vs. floating rate securities, and the team expects to increase the allocation to fixed rates over the coming weeks.

In the near term, money market yields should move in line with Eonia expectations, which center around 0.07% for the next three months, and drift lower to 0.05% thereafter. Natixis AM’s view is that, consistent with recent experience, given the ECB’s difficulty implementing sterilization measures, the effect on liquidity and downward pressure on yields will be limited, and should in fact push Eonia to around 0.10%. Current reimbursements should continue through year end, which could create a zero sum gain in terms of excess liquidity, as it would limit downward pressure on Eonia. A surprise to the upside in Eonia levels (i.e., above 0.10%) is not to be excluded either: as observed in recent months during the first LTRO operations, Eonia rates found support around 0.10%. We could see higher levels in coming months as the excess liquidity actually provided by the first two LTROs was weaker than expected.

Where’s the silver lining?

The upside for banks is a new round of very cheap term funding which should suppress spreads further at the short end, as there will be less need for market financing (net supply further negative). The ECB’s readiness to take on private non-bank credit risk is a novelty and, we believe, the best way to muddle through as banks adjust balance sheets to the new regulation framework.

The question of whether policy will lead to materially stronger investment and borrowing demand could be answered once the effect of policy on inflation expectations is clear. If inflation expectations do bottom out, this might spur current spending and bring growth back to the Euro Area. However, if persistent low inflation or deflation should settle in, then the ECB will just be pushing on a string and the loads of money in the financial sector may never hit Main Street.

Olivier de Larouziere Alain Richier

Head of Interest Rates Head of Money Markets

Axel Botte Elizabeth Breaden

Strategist Head of Product Specialists

Weitere beliebte Meldungen: