Published in French on October the 26th – Data expected this week but already published are briefly discussed.

8 points to keep in mind this week to highlight the macroeconomic momentum

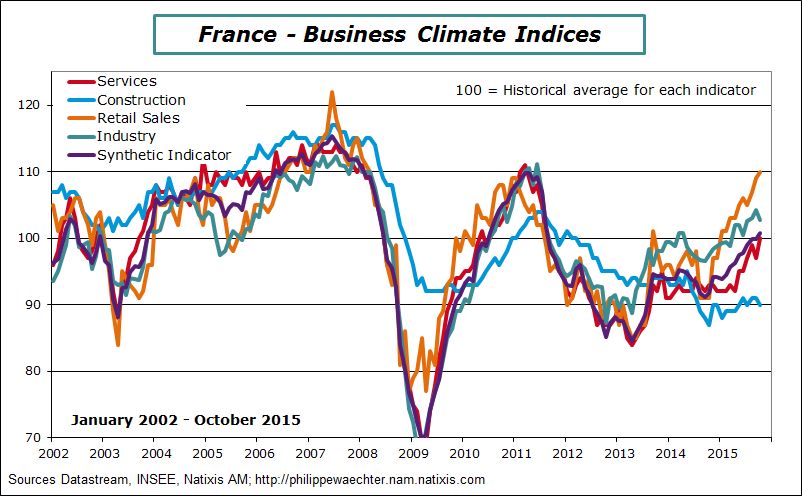

1 – The improvement of the French economy is the real good news

The business climate index, published by INSEE the French Statistical Institute, is above its historical average for the first time since August 2011.

It shows how deep and persistent was the negative shock that has hit the French economy since this period. Looking at the different sectors, building construction is the only one being still on the weak side. Services, Industry and retail trade contribute positively to growth.

The ECB strategy is consistent with the Fed’s behavior; they both prefer acting a little too late than too early

6 – In China the central bank has reduced its interest rates by 25 bp at 4.35% for the one year lending rate and to 1.5% fort the one year deposit rate. The Reserve Requirement Rate was also down by 50bp at 17%.

China is reducing the constraints on growth whereas the economic activity falters. Nevertheless, China is in a huge adjustment process from an industrial led growth economy to a service led growth economy. This will take time and GDP growth will trend downward as services productivity is lower. So the change in monetary policy can help in the very short-term, specifically on land and real estate sectors.

But a simple calculation shows that real interest rate for companies is close to 10 % (interest rate less producer price change) which is way above the GDP growth trend. There is room for lower rates in a deflationary context.

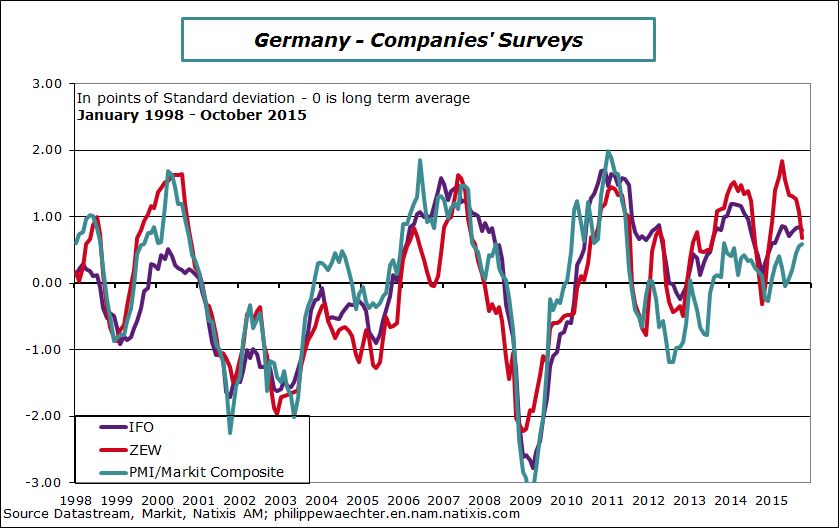

The IFO index has been published on Monday in Germany. It’s a little lower but the German economy is still doing well as it is shown on the graph. The 3 indices are still way above their average. Adjustment on the ZEW reflects correction after an excess.

Have a good week everybody!

Philippe Waechter, Natixis Global Asset Management

Weitere beliebte Meldungen: