Die Fondsmanager der besten Europa Aktienfonds haben exklusiv fünf Fragen zur Bewertung der Assetklasse, den Gewichtungen und Performances beantwortet. Welcher Anteil repräsentierte die Titelauswahl?

Funds

| 27.08.2012 02:00 Uhr

Archiv-Beitrag: Dieser Artikel ist älter als ein Jahr.

Click on picture to enlarge!

e-fundresearch: "Which facts & figures are currently relevant to value European equity and how do you interpret these?"

Thorsten Winkelmann

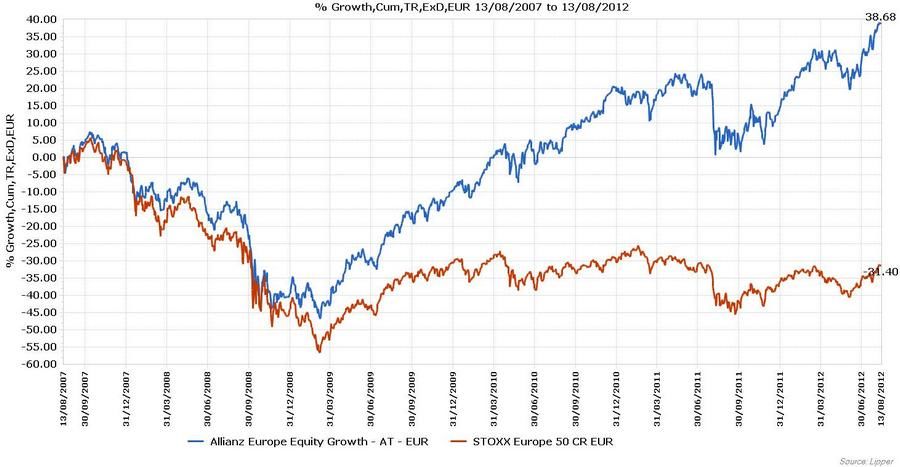

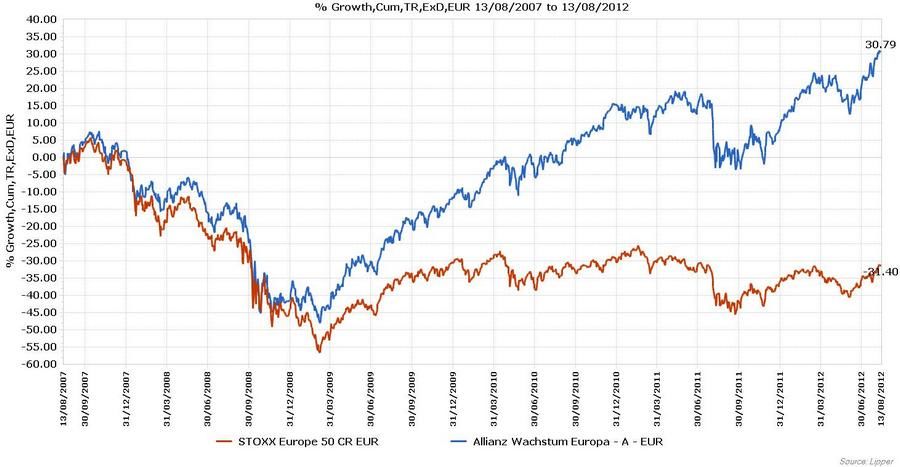

Thorsten Winkelmann, Fund Manager, "Allianz Europe Equity Growth - AT - EUR" (ISIN: LU0256839274) & "Allianz Wachstum Europa - A - EUR" (ISIN: DE0008481821) (21.08.2012): "For us the relevant facts and figures to value European equity have never really changed. The ability to generate sustainable cash flow and earnings growth remains key. As growth investors we are ready to pay a premium for a superior business model but are not willing to overpay. We believe quality companies that can compound their cash-flows through organic growth can allocate capital efficiently and have market leading positions and brands can continue to outperform the broad market. We therefore monitor carefully the development of valuation premiums - they have to be justified by higher ROEs and ROICs. So ultimately by the driver of investment returns superior profitability that persists."

Franz Weis

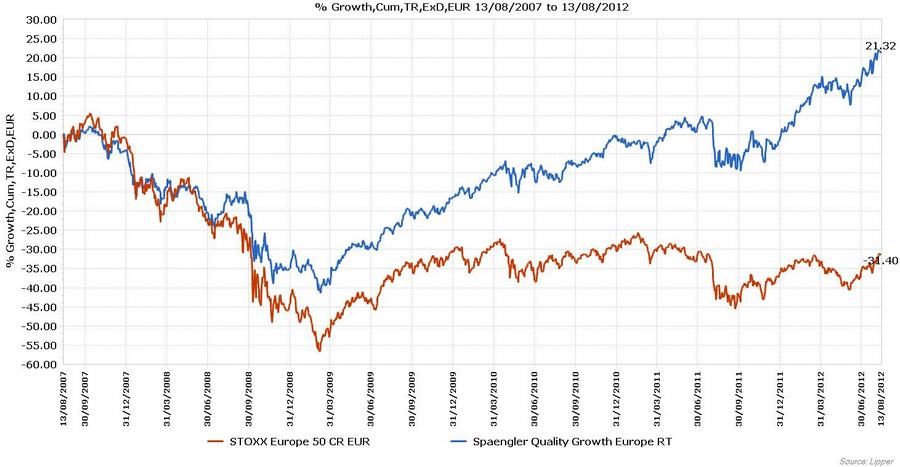

Franz Weis, Fondsmanager, "Comgest Growth Europe Euro" (ISIN: IE0004766675) & "Comgest Europe" (ISIN: LU0039989081) (17.08.2012): "Die Anlagestrategie von Comgest konzentriert sich ausschließlich auf Qualitätswachstumsunternehmen. Wir überzeugen uns zuerst davon, daß ein Unternehmen zweistelliges Gewinnwachstum generieren kann, das auch gut vorhersehbar und weitgehend unabhängig von politischen und makro-ökonomischen Faktoren ist. Erst dann sehen wir uns die Bewertung an: da langfristig die Aktienkurse von der Gewinnentwicklung eines Unternehmens getrieben werden, betrachten wir hauptsächlich das Kurs/Gewinn-Verhältnis, wobei wir gemäß der Qualität eines Geschäftsmodells und der Nachhaltigkeit des überdurchschnittlichen Wachstum differenzieren."

Mike Clements

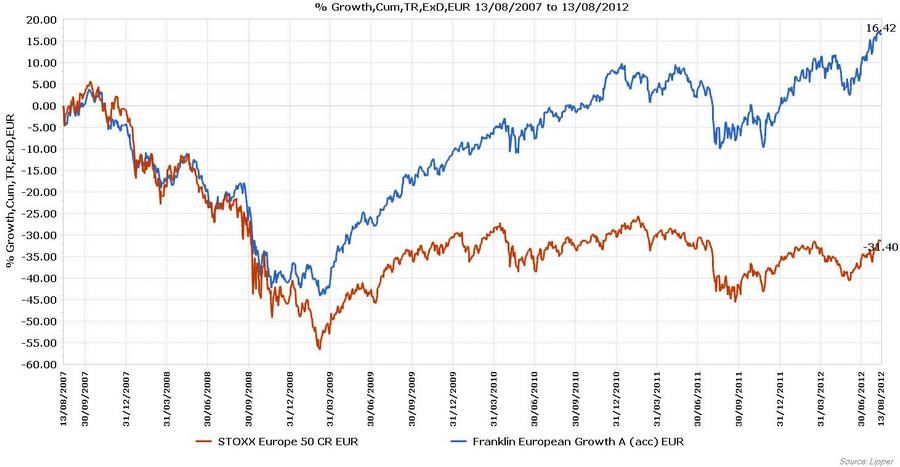

Mike Clements, Fund Manager, "Franklin European Growth A (acc) EUR" (ISIN: LU0122612848) (21.08.2012): "For much of July, global equity markets were beset by increasing fears about the impact of Spain’s debt problems on the future of the eurozone. Yet all these concerns were already present in previous months, and as July progressed, sentiment lifted somewhat on increasing expectations that policy action was on the cards to boost growth. The European Central Bank (ECB) cut deposit and lending rates to historical lows at the beginning of the month, and the People’s Bank of China also cut rates. But it was a commitment from the ECB president, Mario Draghi, that the bank stood “ready to do whatever it takes” to preserve the single currency that ensured that developed- and emerging-market equity indexes ended July in positive territory."

Alexander Darwall

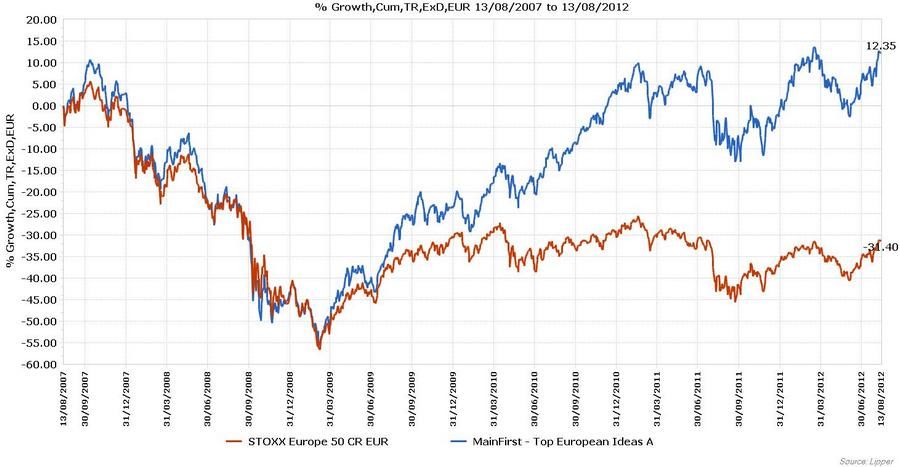

Alexander Darwall, Fund Manager, "Jupiter JGF European Growth L EUR" (ISIN: LU0260085492) (20.08.2012): "Different investors tend to favour different valuation metrics according to the whims of fashion and the position in the economic cycle. For example, in a growth phase, where cash flow is little more than a promise, metrics such as EV/EBITDA (anticipated earnings) multiples are popular whereas, in the depth of a recession, a cautious measure such as price to book (assets) may be favoured by nervous investors. In the current market, generally favoured metrics include: strong, profitable sales growth that delivers rising cash flows, strong balance sheets and attractive price/earnings multiples. In my opinion, these metrics by themselves are of limited use. I believe, more important is the discovery of businesses that have a unique product or service offering sustainability of earnings with the potential for growth whether in their local markets or internationally."

30.06.2026 10:00

30 Min.

Nataliya Taleva, Senior Client Portfolio Managerin im Hedgefonds-Team...

Paul Casson

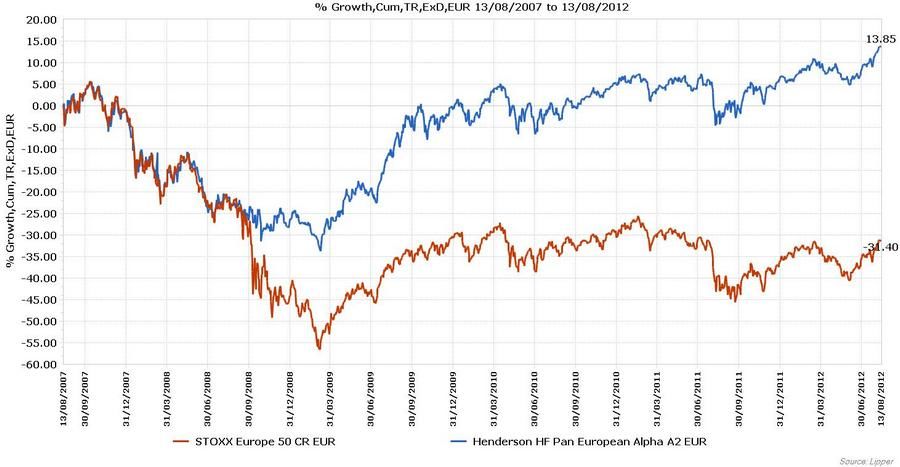

Paul Casson, Fund Manager, "Henderson HF Pan European Alpha A2 EUR " (ISIN: LU0264597617) (22.08.2012): "European Equities look extremely cheap on almost all metrics (P/E, Shiller P/E, P/B, EV/EBITDA...etc) in absolute terms and versus history. They are also cheap versus bonds that in contrast have dangerously high valuations in a number of countries with two-year government bonds being issued at negative nominal yields in some ‘safe havens’. The fact that investors are willing to pay for the privilege of loaning to certain governments is a bizarre concept and shows the level of fear in markets. These cheap valuations have been the case for some time and to a certain degree are irrelevant in the short term until we get some economic and political stability in the region. Tentative steps are being made on this front and when meaningful progress is made investors will once again focus on these cheap valuations and the attractive opportunities to invest in cheap, well managed, quality companies. Given this, it is hard to believe that equities will not produce impressive returns over the long term."

Click on picture to enlarge!

Click on picture to enlarge!

e-fundresearch: "Please describe your investment process briefly."

Thorsten Winkelmann

Thorsten Winkelmann, Fund Manager, "Allianz Europe Equity Growth - AT - EUR" (ISIN: LU0256839274) & "Allianz Wachstum Europa - A - EUR" (ISIN: DE0008481821) (21.08.2012): "The unique aspect of our European Growth strategy lies within our understanding of growth investing based on a bottom up approach. We find that equity markets tend to overvalue short-term growth while undervaluing long-term growth. This implies investing with horizons of three years or more. We focus on stock picking to identify fully or partly undiscovered structural growth rather than growth momentum. Furthermore we consider the benchmark index to be a poor representation of the investment opportunities available and do not believe that fund managers should be obliged to invest in a stock market or sector, size, regardless where they cannot find a company that meets our demanding stock selection criteria. We are typically fully invested, don’t use derivatives and have a low portfolio turnover rate. What counts is that the investment case for the structural growth path of a company is still intact and if the share price is not yet fully reflecting future growth."

Franz Weis

Franz Weis, Fondsmanager, "Comgest Growth Europe Euro" (ISIN: IE0004766675) & "Comgest Europe" (ISIN: LU0039989081) (17.08.2012): "Alle unsere Anlageentscheidungen basieren auf einer fundierten, persönlichen Überzeugung des Fondmanagers. Der Anlageprozess filtert zuerst alle Unternehmen mit zweistelligem Gewinnwachstum, soliden Bilanzen und guten Profitabilitätszahlen heraus. Diese Unternehmen werden dann von Comgests Europa-Team eingehend auf qualitative Aspekte hin analysiert, wie z.B. Markteintrittsbarrieren und Preissetzungsmacht: diese qualitativen Aspekte etablieren die Zuverlässigkeit des zukünftigen Wachstums. Nur wenn ein Unternehmen sowohl hohe Qualitäts- als auch langfristige Wachstumsanforderungen erfüllt, wird die Aktienbewertung in Betracht gezogen. Die Konstruktion des konzentrierten Portfolios mit ca. 30 Titeln erfolgt einzig und allein durch Titelauswahl und ist völlig unabhängig von jeglichen Benchmark-Erwägungen."

Mike Clements

Mike Clements, Fund Manager, "Franklin European Growth A (acc) EUR" (ISIN: LU0122612848) (21.08.2012): "As investment managers, we utilize a bottom-up, long-term strategy and therefore try to take advantage of market volatility to gain exposure to companies with what we view as strong and sustainable competitive advantages, solid balance sheets and substantial cash generation. We tend to be contrarian in our style, and our philosophy and process often lead us to segments of the market that are out of favor with other investors."

Alexander Darwall

Alexander Darwall, Fund Manager, "Jupiter JGF European Growth L EUR" (ISIN: LU0260085492) (20.08.2012): "The Jupiter European Growth Fund is very different to most European funds in that I do not run it as a way to “play” Europe. As such, I am not unduly concerned with index risk but I am very concerned about company risk. I am primarily a stock-picking analyst who looks for a very specific type of company. These will have a unique product or service which gives them strong growth prospects - not only in their local markets but internationally. The fact that they are successful on the global stage means they are less likely to be affected by domestic issues. I want growth companies.

I have a clear model for the type of businesses I consider to be long-term ‘winners’: they are providers of specialist products or services often protected by intellectual property rights; they command oligopolistic positions in areas of long-term structural growth. Thus they have little need to weaken their balance sheets by loading up on debt in order to supercharge pedestrian earnings. They have highly competent management teams, are not dependent on currency fluctuations, do not operate in regulated areas and are not part-owned by the French government.

I am out to invest, not to speculate. I avoid herd behaviour and remain disciplined in my approach. My focus is on understanding companies. I have long experience of understanding both the hard factors, such as economics, history, industries, finance as well as the soft factors like company culture and institutional trading behaviour. As a rule, I typically avoid banks because I consider it impossible to fully appreciate the balance sheet risks. If I cannot understand something then I will not invest in it, no matter how large a part of the index it is. I stick to my disciplined approach. In addition, I am not particularly interested in most cyclical companies and am generally underweight in commodities. If I have an advantage then it lies in an ability to understand the fundamentals of the businesses better than the average analyst. Of course, I cannot tell you when the stock market will recognise superior company performance, only that I believe it will do so."

Paul Casson

Paul Casson, Fund Manager, "Henderson HF Pan European Alpha A2 EUR " (ISIN: LU0264597617) (22.08.2012): "The investment approach used in the Henderson Horizon Pan European Alpha Fund is first and foremost one of bottom-up stock selection. This is based on fundamental and qualitative analysis of companies and is underpinned by a strong risk control discipline. The fund takes a long-term approach to buying shares and will tend to hold long positions in individual names for an average of two to three years. The fund manager is also able to use short positions. The ability to take short positions (through the use of derivatives) allows the fund manager to control the fund’s net exposure to the market, thus smoothing returns and reducing volatility."

Click on picture to enlarge!

e-fundresearch: "Which over- and underweights do you currently hold in the fund?"

Thorsten Winkelmann

Thorsten Winkelmann, Fund Manager, "Allianz Europe Equity Growth - AT - EUR" (ISIN: LU0256839274) & "Allianz Wachstum Europa - A - EUR" (ISIN: DE0008481821) (21.08.2012): "We see the capex spending cycle of the oil and mining industry going on for a few years. We therefore remain confident in selected investment cases among capital goods. We remain constructive on IT spending as companies are investing again. We stick to our holdings in the structural winners especially in the software space. Next to this, growing consumption in Emerging Markets remains on our agenda, where brand strength and high entry barriers to entry are of high importance. Selected trends in healthcare build another important part of our strategy, but we will focus on areas where we do not see pressure from healthcare reforms and a threat from patent expiries like for a lot of the big pharma names. In Emerging Markets automation and energy efficiency is of increasing importance, as labor costs and environmental issues are increasing. Inflationary pressures coming from Emerging markets and raw materials have to be monitored, as they are impacting input costs for a couple of companies. We struggle to identify structurally growing franchises among telecom and utility stocks. As we have been for a very long time, we have only very selective holdings in Financials."

Franz Weis

Franz Weis, Fondsmanager, "Comgest Growth Europe Euro" (ISIN: IE0004766675) & "Comgest Europe" (ISIN: LU0039989081) (17.08.2012): "Die größten Positionen im Fonds sind Inditex und SAP. Wie Inditex (die Holding-Gruppe mit den Marken Zara und Massimo Dutti) mit den jüngsten Quartalszahlen bewiesen hat, ist das spanische Unternehmen trotz der Wirtschafts- und Bankenkrise in Spanien in der Lage, dynamisches Umsatz- und Gewinnwachstum zu liefern, dank seines Geschäftsmodells und seiner fortlaufenden internationalen Expansion. SAP wächst aufgrund der starken Nachfrage in Schwellenländern, der Notwendigkeit von Unternehmen sich für den Wettbewerb zu rüsten, und durch Innovationen in den Bereichen Datenbanken und Mobilität. Comgests Europa-Fonds meiden seit über 20 Jahren Banken und stark zyklische Branchen wie Autos, Chemie und Rohstoffe."

Mike Clements

Mike Clements, Fund Manager, "Franklin European Growth A (acc) EUR" (ISIN: LU0122612848) (21.08.2012): "We continue to believe that the best time for us to consider purchasing European equities, especially in peripheral countries such as Portugal, Ireland, Greece, Italy and Spain, is likely to be over the next six to12 months. We also believe building construction and materials remain attractive industries. Overall, we still believe stock valuations, particularly in Europe, support our optimistic outlook for investment performance potential over the next few years."

Alexander Darwall

Alexander Darwall, Fund Manager, "Jupiter JGF European Growth L EUR" (ISIN: LU0260085492) (20.08.2012): "The Fund is currently overweight Industrials, Healthcare, Basic Materials and Technology compared to the Fund’s benchmark, the FTSE World Europe Index.

The Fund is underweight Financials, Consumer Goods and Oil & Gas. It has zero exposure to Telecoms and zero exposure to Utilities.

The Fund is positioned to aim to benefit from European companies that are exposed to global growth, particularly in fast-growing economies such as Brazil, India and China, and that have strong balance sheets, productivity-enhancing and cost-saving products and services that are attractive."

Paul Casson

Paul Casson, Fund Manager, "Henderson HF Pan European Alpha A2 EUR " (ISIN: LU0264597617) (22.08.2012): "Being an absolute return focused fund we do not look at over/underweights but rather absolute weights. The fund currently has its largest net long exposures in the Consumer, Energy and Healthcare sectors. This has resulted from the funds bottom-up investment process."

Click on picture to enlarge!

Click on picture to enlarge!

Alexander Darwall

Paul Casson

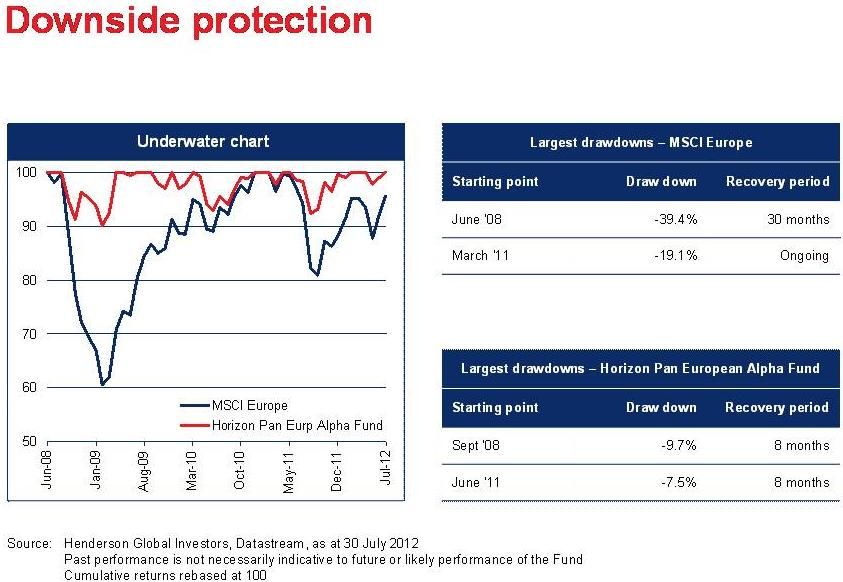

Paul Casson, Fund Manager, "Henderson HF Pan European Alpha A2 EUR " (ISIN: LU0264597617) (22.08.2012): "The fund has few rigid limits with respect to risk. This allows the fund manager the flexibility to seek alpha wherever he deems fit for his clients. However risk control plays a large part in the stock picking and portfolio construction. The ability to take short positions has enabled the PM to limit downside risk despite a difficult market environment. This is highlighted by the drawdown analysis below:

Click on picture to enlarge!

POSITIVE RETURNS IN EACH OF THE LAST THREE YEARS.

The fund continues to perform strongly making new absolute highs."

Click on picture to enlarge!

Click on picture to enlarge!

Alexander Darwall

Paul Casson

Paul Casson, Fund Manager, "Henderson HF Pan European Alpha A2 EUR " (ISIN: LU0264597617) (22.08.2012): "The fund has very strong risk adjusted returns since Paul Casson took control of the fund in June 2008. The bulk of the returns can be attributed to good stock picking and good balance sheet management (i.e. increasing the funds market exposure during strong market performance and reducing market exposure when market performance is weak)

The chart below highlights the funds strong returns versus all the major asset classes."

Click on picture to enlarge!

Click on picture to enlarge!

Click on picture to enlarge!

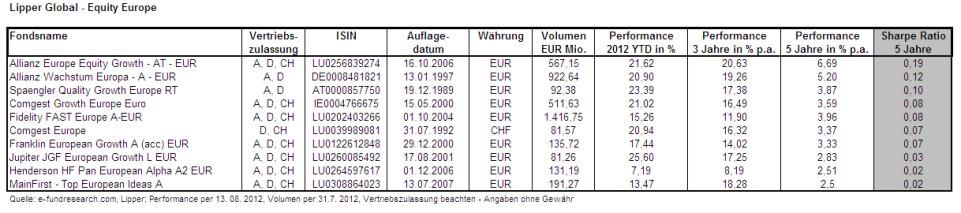

Alle Performance Daten der Top-10 Auswertung per 13.08.2012:

Performanceergebnisse der Vergangenheit lassen keine Rückschlüsse auf die zukünftige Entwicklung

eines Investmentfonds oder Wertpapiers zu. Wert und Rendite einer Anlage in Fonds oder

Wertpapieren können steigen oder fallen. Anleger können gegebenenfalls nur weniger als das

investierte Kapital ausgezahlt bekommen. Auch Währungsschwankungen können das Investment

beeinflussen. Beachten Sie die Vorschriften für Werbung und Angebot von Anteilen im InvFG 2011

§128 ff. Die Informationen auf www.e-fundresearch.com repräsentieren keine Empfehlungen für den

Kauf, Verkauf oder das Halten von Wertpapieren, Fonds oder sonstigen Vermögensgegenständen. Die

Informationen des Internetauftritts der e-fundresearch.com AG wurden sorgfältig erstellt.

Dennoch kann es zu unbeabsichtigt fehlerhaften Darstellungen kommen. Eine Haftung oder Garantie

für die Aktualität, Richtigkeit und Vollständigkeit der zur Verfügung gestellten Informationen

kann daher nicht übernommen werden. Gleiches gilt auch für alle anderen Websites, auf die

mittels Hyperlink verwiesen wird. Die e-fundresearch.com AG lehnt jegliche Haftung für

unmittelbare, konkrete oder sonstige Schäden ab, die im Zusammenhang mit den angebotenen oder

sonstigen verfügbaren Informationen entstehen.

Klimabewusste Website

AXA Investment Managers unterstützt e-fundresearch.com auf dem Weg zur Klimaneutralität.

Erfahren Sie mehr.